Damaged motorcycle on roadside with rider holding insurance policy document

How Your Motorcycle Accident Insurance Deductible Works After a Crash

Your bike is damaged, you're dealing with injuries, and now your insurance company mentions a deductible. For many riders, this is the moment they realize they don't fully understand what they signed up for. The deductible isn't just a number on your policy—it's the amount you'll pay out of pocket before your insurance kicks in, and it can range from a manageable $250 to a wallet-draining $2,500 or more.

Understanding how deductibles work after a motorcycle accident means the difference between financial preparedness and scrambling to cover unexpected costs while your bike sits in a repair shop.

How Insurance Deductibles Work in Motorcycle Accidents

A deductible is your share of the repair or replacement costs when you file a claim. If your bike sustains $5,000 in damage and you carry a $1,000 deductible, you pay the first $1,000, and your insurer covers the remaining $4,000. Simple enough—until you factor in which coverage applies and who caused the accident.

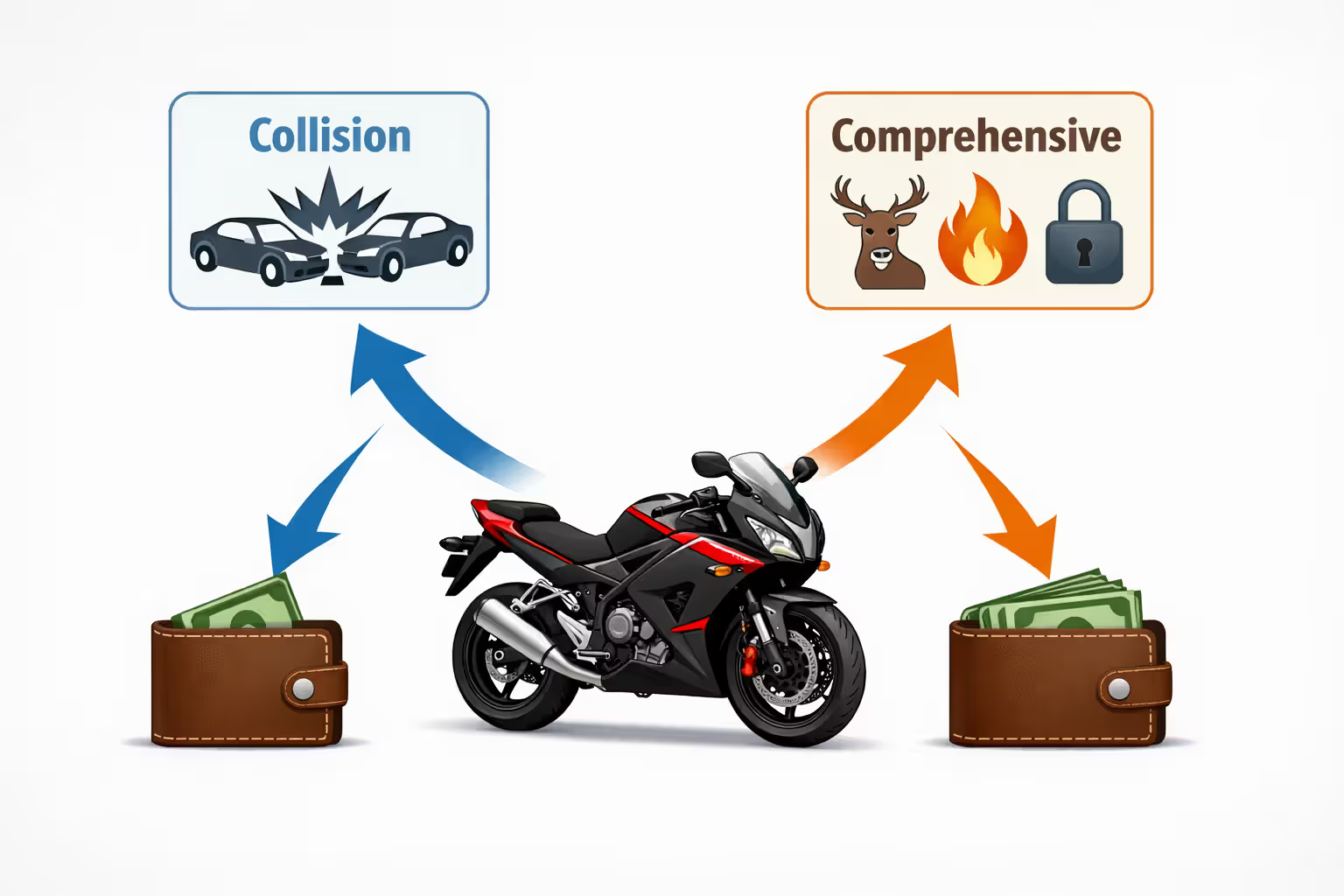

Not all motorcycle insurance coverage types require deductibles. Liability coverage, which pays for damage you cause to others, never involves a deductible on your end. The other driver's property damage and medical bills get paid directly by your insurer up to your policy limits. Collision and comprehensive coverage, however, almost always come with deductibles.

Collision coverage handles damage from crashes with vehicles or objects, regardless of fault. If you slide out on gravel or get sideswiped by a car, collision coverage applies—and so does your deductible. Comprehensive coverage addresses non-collision events: theft, vandalism, fire, falling objects, or animal strikes. Hit a deer on a rural highway? That's comprehensive, and you'll pay your comprehensive deductible, which is often lower than your collision deductible.

Author: Olivia Bennett;

Source: spy-delhi.com

At-Fault vs. Not-At-Fault: Does It Change Your Deductible?

When you're at fault for an accident, you'll definitely pay your collision deductible to repair your own bike. Your liability coverage handles the other party's damages without a deductible, but your bike repairs come out of your collision coverage—deductible required.

When another driver causes the accident, the situation gets more nuanced. Ideally, you'd file a claim against their liability insurance and avoid paying any deductible. Their insurer would cover your bike repairs, medical expenses, and other losses. Reality rarely moves this smoothly. The other driver might dispute fault, carry insufficient coverage, or their insurer might drag out the claims process for weeks or months.

Many riders choose to file under their own collision coverage to get repairs started quickly, paying their deductible upfront. Once fault is established, your insurance company pursues subrogation—recovering costs from the at-fault driver's insurer, including your deductible. This process can take 30 to 90 days, sometimes longer. Some insurers offer deductible waivers for verified not-at-fault accidents, but this varies by company and state.

Which Coverage Types Require Deductible Payment

Collision coverage: Always requires a deductible, typically $500 to $1,000 for most riders.

Comprehensive coverage: Requires a deductible, often set lower than collision ($250 to $500 is common).

Liability coverage: Never requires a deductible. You're paying for others' damages, not your own.

Medical payments coverage (MedPay): Usually no deductible. This coverage pays medical bills up to your limit regardless of fault.

Uninsured/underinsured motorist coverage: Depends on your state and policy. Some states require no deductible for UM/UIM property damage; others apply your collision deductible.

Personal injury protection (PIP): Typically no deductible in no-fault states, though some policies offer deductible options to lower premiums.

Common Deductible Amounts and What Influences Your Rate

Most motorcycle insurance policies offer deductible choices between $250 and $2,500. The amount you select directly impacts your premium—the annual cost of your insurance. Higher deductibles mean lower premiums because you're assuming more financial risk. Lower deductibles cost more upfront but reduce your out-of-pocket expense after an accident.

A rider choosing a $250 deductible might pay $200 to $400 more annually compared to selecting a $1,000 deductible. Over five claim-free years, that's $1,000 to $2,000 in extra premiums—enough to cover the higher deductible if an accident finally occurs. The math shifts based on your riding habits, storage situation, and local theft rates.

Several factors beyond your choice influence deductible costs. Riders with sport bikes or high-value cruisers often face minimum deductible requirements—insurers might not offer anything below $500 or $1,000 for bikes worth over $20,000. Your location matters too. Urban areas with high theft rates might see comprehensive deductible minimums of $500, while rural riders can sometimes select $100 comprehensive deductibles.

Your age and riding experience play a role. Newer riders under 25 might find lower deductible options significantly more expensive, while experienced riders over 40 with clean records get better pricing across all deductible levels.

| Deductible Amount | Typical Annual Premium Savings vs. $250 | Out-of-Pocket Cost Per Claim | Best Fit For |

| $250 | Baseline (highest premium) | $250 | Riders in high-risk areas, new riders, those financing expensive bikes |

| $500 | $150–$250 saved annually | $500 | Average riders balancing affordability and protection |

| $1,000 | $300–$450 saved annually | $1,000 | Experienced riders with emergency savings, low annual mileage |

| $2,000 | $500–$700 saved annually | $2,000 | High-income riders, track bikes, riders who self-insure minor damage |

The break-even point matters. If you save $400 annually by jumping from a $250 to $1,000 deductible, you'd break even after roughly two years without a claim. File a claim in year one, and you've paid $400 in premium savings but owe an extra $750 out of pocket—a net loss of $350. Wait five years between claims, and you've saved $2,000 in premiums while only paying $750 more in deductibles—a $1,250 gain.

When You Must Pay Your Deductible (And When You Don't)

Understanding exactly when your deductible applies prevents surprises during an already stressful time.

Single-vehicle crashes always trigger your collision deductible. You low-side on a wet corner, clip a curb, or misjudge a turn—these scenarios mean you're filing under your own collision coverage and paying your deductible before repairs begin.

Multi-vehicle accidents where you're clearly not at fault offer two paths. You can file through the other driver's liability insurance and pay nothing, but expect delays while insurers investigate and negotiate. Alternatively, file under your collision coverage, pay your deductible, and get repairs started immediately. Your insurer handles subrogation to recover costs, including your deductible, from the at-fault party's insurance.

Author: Olivia Bennett;

Source: spy-delhi.com

Hit-and-run situations depend on your coverage. If the fleeing driver is never identified, you'll use collision coverage and pay your deductible. Some states offer uninsured motorist property damage coverage with lower or no deductibles for hit-and-runs, but you must have purchased this coverage beforehand.

Uninsured motorist claims vary by state law. In some states, uninsured motorist property damage has no deductible. In others, your collision deductible applies. Check your declarations page—it should specify whether your UM/UIM coverage includes a deductible.

Theft falls under comprehensive coverage. Your bike disappears from your driveway, and you'll pay your comprehensive deductible before receiving the actual cash value payout. If you carry a $500 comprehensive deductible and your bike is valued at $8,000, you'll receive $7,500.

Vandalism and weather damage also trigger comprehensive deductibles. Someone keys your tank, or hail dents your fairings—you're paying that comprehensive deductible for repairs.

Animal strikes are comprehensive claims. The deer that totaled your bike on a backroad means paying your comprehensive deductible, not collision, even though you technically collided with something.

You won't pay a deductible when another driver's liability insurance accepts responsibility and pays your claim directly. You also skip the deductible if you're only claiming medical payments coverage or personal injury protection for your injuries—these coverages typically have no deductible.

Step-by-Step: Paying Your Deductible After a Motorcycle Crash

The deductible payment process isn't always intuitive, and timing matters more than most riders realize.

First, report the accident to your insurance company within 24 to 48 hours. Provide photos, police report numbers, and witness information. Your insurer assigns a claims adjuster who inspects the damage and estimates repair costs.

Once the adjuster approves repairs, you'll receive instructions on deductible payment. The most common method: you pay the deductible directly to the repair shop when you pick up your bike. The shop receives the full repair cost from your insurer minus your deductible amount. If repairs cost $3,200 and you carry a $500 deductible, your insurer pays the shop $2,700, and you pay the remaining $500.

Some insurers handle it differently. They might pay the shop the full amount and require you to reimburse them for the deductible. Others deduct it from their payment to you if you're receiving a cash settlement instead of using a shop.

For total loss claims—when your bike is deemed unrepairable or repair costs exceed its value—the insurer calculates the actual cash value of your motorcycle and subtracts your deductible from that amount. Own a bike valued at $9,000 with a $1,000 deductible? You'll receive an $8,000 settlement check. If you're still making loan payments and owe more than the bike's value, gap insurance covers the difference, but your deductible still applies to the primary payout.

The timeline from accident to payment typically spans one to three weeks for straightforward claims. Complex cases involving liability disputes or extensive damage can stretch to several months.

What Happens If You Can't Afford Your Deductible

Financial strain after an accident is common, especially if you're also dealing with medical bills or lost wages. Most repair shops require deductible payment before releasing your bike, creating a real problem if you don't have $500 to $1,000 available.

Some insurers offer payment plans for deductibles, allowing you to spread the cost over several months. This isn't universal—you'll need to ask your claims adjuster specifically about payment arrangements. Approval often depends on your payment history and policy standing.

Author: Olivia Bennett;

Source: spy-delhi.com

Credit cards remain the most common solution, though interest charges can make an expensive situation worse. Some riders negotiate directly with repair shops for payment plans, though shops aren't obligated to agree.

If you're pursuing subrogation because another driver was at fault, explain your financial situation to your insurer. Some companies will advance your deductible recovery or work with you on timing, knowing they'll collect from the other party's insurance.

The worst option: skipping repairs entirely because you can't afford the deductible. This leaves you without transportation and potentially violates loan agreements if you're financing the bike.

5 Costly Mistakes Riders Make With Deductibles

Choosing a deductible based solely on premium savings backfires when you can't cover the out-of-pocket cost after an accident. A rider saving $400 annually with a $2,000 deductible faces a serious problem if they don't have $2,000 in accessible savings. The general rule: don't select a deductible higher than you can comfortably pay within 30 days.

Assuming the other driver's insurance will pay immediately leads to delayed repairs and frustration. Even clear-cut cases take weeks to resolve. Fault disputes, unresponsive adjusters, and coverage investigations drag on. Riders who wait for the other party's insurer often go weeks without transportation. Filing under your own collision coverage gets you back on the road faster.

Filing small claims that barely exceed your deductible damages your claims history and can raise future premiums. A $700 repair with a $500 deductible nets you $200 from insurance but marks you as a higher-risk customer. Many insurers increase rates after just one claim, even if you weren't at fault. Save your coverage for significant losses—pay out of pocket for minor damage below $1,000 over your deductible.

Not understanding that different coverage types carry different deductibles creates confusion. Your policy might show a $1,000 collision deductible but only a $250 comprehensive deductible. Riders who assume both are the same get surprised when theft or vandalism costs less out of pocket than a crash.

Forgetting about multiple deductibles in severe accidents catches riders off guard. If your bike is damaged and you're injured, you might face a collision deductible for the bike and separate out-of-pocket costs for medical care (depending on your health insurance). Some policies include separate deductibles for accessories and custom parts—that $3,000 aftermarket exhaust system might carry its own deductible clause.

Deductible Waivers and Exceptions You Should Know

Vanishing deductibles reward claim-free years by reducing your deductible over time. Some insurers decrease your deductible by $50 to $100 for each year without a claim, sometimes down to zero. Five claim-free years might reduce a $500 deductible to $0. File a claim, and the deductible resets to your original amount. This feature isn't standard—you'll pay slightly higher premiums for vanishing deductible policies, but the long-term savings can be substantial for safe riders.

Author: Olivia Bennett;

Source: spy-delhi.com

Deductible waivers for verified not-at-fault accidents vary widely by insurer and state. Some companies waive your collision deductible entirely if the other driver's insurance accepts full responsibility. Others offer "disappearing deductibles" where they refund your deductible once subrogation recovers the money from the at-fault party. California, for example, requires insurers to waive deductibles in certain not-at-fault scenarios, while other states leave it to policy terms.

Broad form collision coverage, available in some states, eliminates your deductible when you're not at fault but keeps it in place for at-fault accidents. This costs more than standard collision coverage but less than a low deductible across the board.

Diminishing deductibles for specific coverage types appear in some comprehensive policies. Certain insurers offer $0 deductibles for glass damage (windshields on touring bikes) or waive deductibles for total theft if you have approved anti-theft devices installed.

Loyalty programs occasionally include deductible benefits. Long-term customers with the same insurer for 5+ years might qualify for reduced deductibles or one-time deductible waivers. These perks aren't advertised—you need to ask your agent directly.

Expert Insight:

I tell riders to think of their deductible as their emergency fund for the bike.If you can't write a check for your deductible tomorrow without financial stress, it's too high. I've seen too many riders choose $1,500 or $2,000 deductibles to save $30 a month on premiums, then panic when they actually need to file a claim. Your deductible should match your risk tolerance and your bank account, not just your desire for cheaper monthly payments

— Marcus Chen

FAQ: Motorcycle Accident Insurance Deductible Questions

Making Smart Deductible Decisions for Your Riding Future

Your deductible choice affects both your monthly budget and your financial security after an accident. Riders who balance premium savings against realistic emergency funds tend to navigate claims with less stress. Consider your riding frequency, storage security, and local accident rates when selecting a deductible—not just the immediate premium difference.

Review your deductible annually at renewal time. Your financial situation changes, your bike's value depreciates, and your risk tolerance evolves. The $1,000 deductible that made sense when you bought a new bike might be too high three years later when the bike's value has dropped by 40%. Conversely, experienced riders who've built emergency savings might increase deductibles to reduce premiums without increasing financial risk.

Document your coverage details now, before you need them. Know your collision deductible, comprehensive deductible, and whether your policy includes any waivers or special provisions. Take photos of your declarations page and store them digitally where you can access them after an accident. Understanding what you'll pay before you're dealing with a damaged bike and an insurance adjuster makes the entire process smoother and less overwhelming.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer insights and guidance on motorcycle accident insurance claims, settlement processes, liability issues, coverage limits, medical compensation, and related insurance matters, and should not be considered legal or financial advice.

All information, articles, and materials presented on this website are for general informational purposes only. Insurance policies, liability standards, settlement practices, and state regulations may vary by jurisdiction and insurer. The outcome of a motorcycle accident claim depends on the specific facts of the accident, available evidence, policy language, and applicable law.

This website is not responsible for any errors or omissions in the content, or for actions taken based on the information provided. Users are strongly encouraged to consult with a qualified attorney or licensed insurance professional regarding their specific motorcycle accident claim before making decisions about settlements, negotiations, or coverage disputes.