Motorcyclist standing beside a damaged motorcycle on the roadside holding insurance documents with traffic in the background

How Much Do Motorcycle Insurance Rates After an Accident Increase

Drop your bike in a parking lot or get sideswiped by a car? Your first worry is probably the damage to your ride. Your second worry should be what happens to your insurance bill. Here's what riders actually face: if you're at fault, expect somewhere between a 20% and 50% bump in your premium. Could be more. Could be less. The number swings based on stuff like who caused the crash, how bad it was, your previous riding history, and which state you call home.

Let's break down exactly how insurers calculate these increases—and what you can do about them.

Why Motorcycle Insurance Rates Increase After Accidents

Think of insurance pricing like a betting pool. Before your accident, you're in the "probably safe" category. After filing a claim? You've proven you're not just a theoretical risk anymore. Research from actuarial firms reveals something uncomfortable: someone who's crashed once has a statistically higher chance of crashing again within the next 36 to 60 months compared to riders who've never filed a claim.

Here's where the math gets painful. You're getting hit twice. The first punch is the accident surcharge itself—basically a markup percentage slapped onto your base premium. The second hit comes from losing your good-rider discount. Maybe you were getting 15% or 20% knocked off your bill. That evaporates after a claim. Stack these together and you're looking at increases that shock most riders.

Author: Caleb Thornton;

Source: spy-delhi.com

Your crash doesn't stay private, either. There's this database called CLUE (Comprehensive Loss Underwriting Exchange) that tracks your insurance history going back five to seven years. Every insurer checks it. You can't just hop to a new company and pretend nothing happened. They'll see your record within seconds of pulling your quote.

Now, state laws do throw you a bone sometimes. California won't let insurers penalize you for accidents where you weren't at fault. Other states? They absolutely allow it. Some states cap how much your rate can jump. Others let insurance companies go wild with surcharges. Where you live matters enormously.

Average Rate Increases by Accident Type and Fault Status

Not all crashes hit your wallet the same way. A low-speed drop in a parking lot plays out differently than a three-bike pileup on the interstate.

| Type of Crash | How Much Rates Jump | What That Costs You Annually | How Long You Pay Extra |

| Your fault, someone got hurt | 40-55% higher | Add $800-$1,500 to your bill | You're stuck for 3-5 years |

| Your fault, just bike/car damage | 20-35% higher | Add $400-$750 to your bill | Lasts 3-5 years |

| You crashed by yourself | 25-40% higher | Add $500-$900 to your bill | Continues for 3-5 years |

| Other driver's fault | 0-15% higher | Maybe $0-$300 more | Might last 1-3 years |

| Accident involving DUI | 80-150% higher | Add $2,000-$4,000 annually | Follows you 5-10 years |

These numbers assume you're currently paying around $2,000 per year for coverage on a standard bike. If you're already paying premium rates because you're young, ride a superbike, or live in a pricey area, the dollar amounts scale up accordingly even if the percentage stays similar.

Property-damage-only wrecks don't freak insurers out as much. They know they're looking at a few thousand dollars max. But add injuries to the mix? Now they're worried about medical bills that could hit six figures. That's why injury accidents trigger much steeper surcharges. Single-vehicle crashes—like when you overcook a turn and slide into a ditch—land somewhere in the middle. You messed up, but at least you didn't take anyone else with you.

The not-at-fault situation gets weird. Sure, the other guy caused it. But statistics show that riders who've been in any collision—regardless of fault—file more claims later than riders with zero accidents. Some companies ding you anyway. Others don't. Your state law often decides which approach applies.

DUI crashes? That's scorched earth for your rates. Plenty of regular insurance companies will flat-out refuse to renew your policy. You'll get shoved into high-risk insurance pools where you might pay three or four times what you used to pay.

Key Factors That Determine Your Post-Accident Premium

Beyond just the accident itself, insurers look at your entire risk profile when deciding how much to jack up your rates.

Your Riding Record and Claims History

One accident after a decade of perfect riding? That's different from someone who collects tickets and claims like baseball cards. Insurance companies give you more benefit of the doubt if you've been clean for years. They'll see it as bad luck rather than a pattern.

There's this five-year window that matters most. Something that happened four and a half years ago barely registers. Last month's crash? That's sitting front and center in their computer. As time passes without new claims, your rates creep back down naturally.

Here's the really painful part: multiple accidents don't just add up—they multiply. Two at-fault crashes within three years might triple your premium. But space those same two crashes seven years apart and the damage is way less severe. Insurers see clustered incidents as proof you're a chronically risky rider rather than someone who had an unlucky stretch.

Author: Caleb Thornton;

Source: spy-delhi.com

Accident Severity and Payout Amount

A $1,500 fender-bender plays differently than a $25,000 multi-vehicle catastrophe. Insurance companies track both how often you crash and how expensive those crashes are. A massive payout tells them you're not just likely to crash—you're likely to crash expensively.

Some insurers actually run tiered systems. Claims under two grand might bump you 20%. Claims over ten grand? That's a 45% increase. They're trying to match the punishment to the demonstrated risk.

Anything involving injuries carries extra weight beyond the immediate dollar amount. Medical costs have this nasty habit of growing over time. Someone might need surgery six months later. Or physical therapy for two years. Or maybe they develop chronic pain that leads to a disability claim. Insurers know the check they wrote on day one might not be the final bill, so they price injury accidents more aggressively.

State Regulations and Forgiveness Programs

Seventeen states have passed laws limiting how aggressively insurers can hammer you for accidents. Massachusetts and Hawaii cap surcharge percentages. California blocks rate increases entirely for not-at-fault crashes regardless of circumstances.

Then there's accident forgiveness—basically insurance for your insurance. If you've been riding clean for five years without major violations, many companies will waive the surcharge on your first at-fault crash. Some include this automatically. Others make you pay $50 to $150 per year extra for the privilege.

One catch: forgiveness doesn't follow you to a new company. If you switch carriers, you start from scratch. That means riders who've just had an accident and have forgiveness should think really carefully before jumping ship.

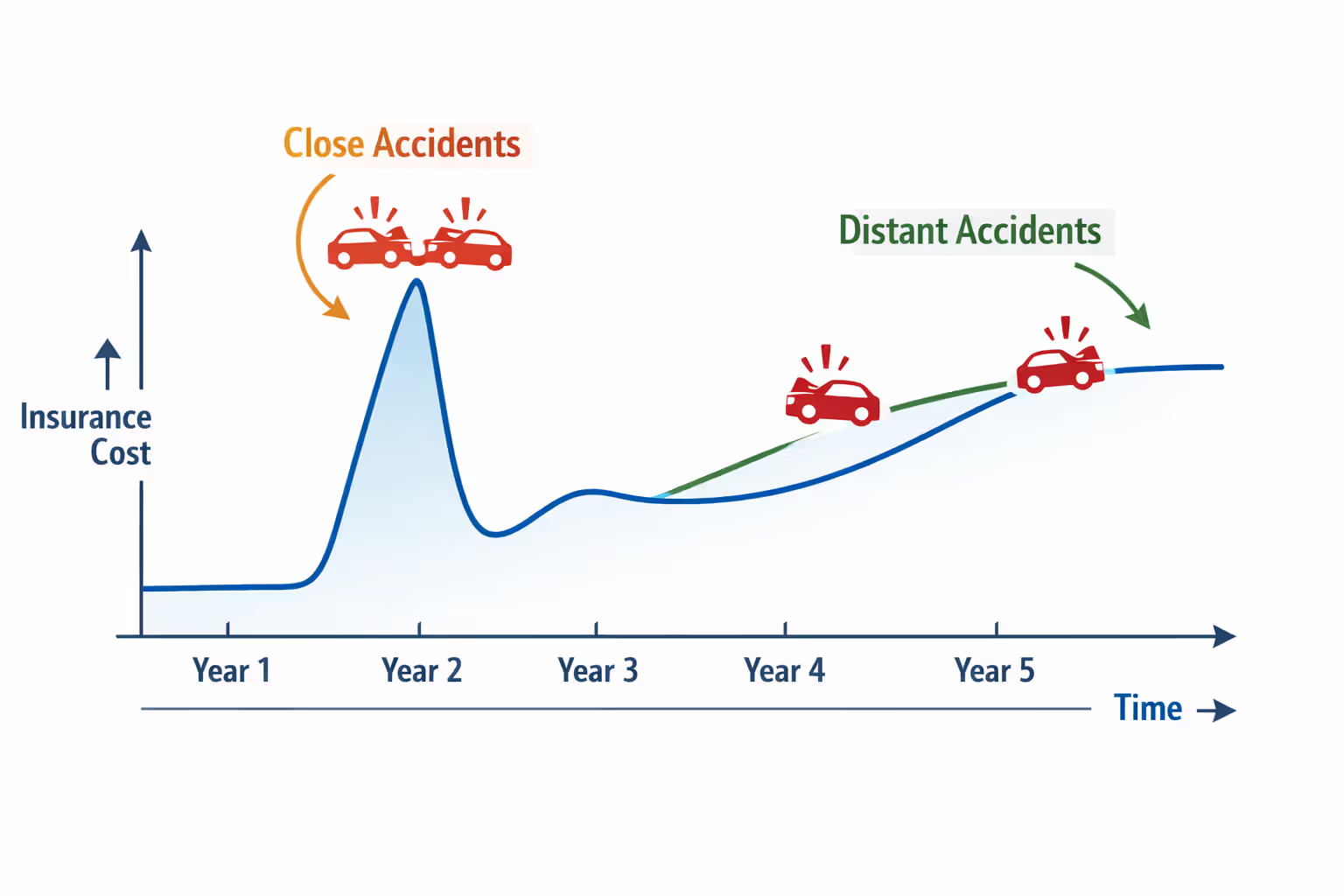

How Long Accidents Affect Your Motorcycle Insurance Rates

Most states give insurers a three to five-year window to hold accidents against you when setting rates. The surcharge usually stays at full strength for three years, then starts dropping in years four and five before finally disappearing completely.

Different companies handle the decline differently. Some use a step-down schedule: maybe 40% extra in year one, then 30%, then 20%, then 10%, then gone. Others hold you at a flat surcharge for three full years and then remove it entirely.

Major screw-ups like DUI stretch that window to ten years in many places. Even after the surcharge finally drops, the incident stays visible in your record. Some carriers will refuse to cover you at any price if they see a DUI, regardless of how ancient it is.

The CLUE database keeps accident records for seven years, but state law determines how long insurers can actually use that information to set your price. Your bill won't automatically drop when an accident hits the three or five-year mark. You might need to shop around or specifically ask your agent to review your rate to capture that improvement.

Your policy renewal date is when these adjustments typically happen. As crashes age past the three or five-year threshold, your renewal price should reflect the cleaner slate. If it doesn't, call your agent. Sometimes the system doesn't automatically update and you need to push for the correction.

Author: Caleb Thornton;

Source: spy-delhi.com

Strategies to Reduce Insurance Costs After a Motorcycle Accident

These rate increases aren't set in stone, and they don't last forever. Here's how to minimize the financial beating.

Buy accident forgiveness before you need it. Spend $100 a year now, potentially save $800 a year later after a crash. If you're planning to keep riding for the next five-plus years, the math strongly favors buying forgiveness in advance.

Take a defensive riding course. Most insurers knock 5% to 15% off your premium if you complete approved training. After an accident, signing up for an advanced safety class shows you're serious about improving. A few companies will actually waive the accident surcharge entirely if you finish the course within 90 days of the crash.

Bump up your deductible from $500 to $1,000 or even $2,000. This typically cuts your premium by 10% to 25%. Since you're already dealing with elevated rates post-accident, the savings on monthly bills can outweigh the risk of paying more out-of-pocket if something else happens.

Shop around aggressively. One company might hit you with a 45% surcharge while another applies only 25%. Get quotes from at least five different insurers to find who's most forgiving of your new risk profile.

Bundle your motorcycle insurance with your car or home policy. Multi-policy discounts run 15% to 25% at most companies. These discounts often exceed accident surcharges, meaning you might actually pay less overall despite the crash on your record.

Drop comprehensive and collision coverage on older bikes. If your motorcycle's only worth $4,000, paying for full coverage year after year costs more than the bike's value over time. Switching to liability-only after an accident prevents rate increases on coverage you don't really need anyway.

Common Mistakes Riders Make After an Accident That Increase Rates

Some moves make everything worse. Avoid these blunders and you'll save yourself grief and money.

Don't file tiny claims below your deductible. Paying $400 out-of-pocket for a small repair keeps it off your record. That $800-per-year surcharge you'd get stuck with for five years costs way more than fixing it yourself.

Don't just accept your renewal quote without shopping. Your current company will probably apply their maximum allowed surcharge. Competitors, though? They're hungry for new customers and might offer way better rates. Loyalty doesn't pay after accidents—switching can save 20% to 30%.

Don't let your coverage lapse. Creating a gap in your insurance history brands you as ultra-high-risk. When you finally get coverage again, insurers pile a 30% to 50% lapse penalty on top of your accident surcharges. Even if money's tight, keep at least state minimum liability going.

Don't ignore available discounts. Tons of riders don't realize they qualify for low-mileage discounts, motorcycle club memberships, anti-theft device credits, or safety equipment discounts. These can offset accident surcharges partially. Review your discount eligibility every single year.

Don't assume you're not eligible for accident forgiveness. Some policies automatically include it after you've maintained a clean record for a certain period. Ask your agent directly. You might be able to remove surcharges you thought were mandatory.

Author: Caleb Thornton;

Source: spy-delhi.com

When to Consider Switching Insurance Companies After an Accident

Timing matters when shopping for new coverage. Strategic planning maximizes your odds of finding decent rates despite your crash history.

Wait for your policy renewal date. Canceling mid-term usually triggers short-rate penalties where you lose part of what you've already paid. Start shopping 45 to 60 days before renewal so you have time to compare properly without rushing.

Get quotes from at least five companies covering different market segments. Standard carriers like State Farm and Progressive compete against motorcycle specialists like Dairyland and Foremost, plus regional companies you've never heard of. Rate differences of 40% to 60% between carriers are totally normal for post-accident riders.

Make sure you're comparing identical coverage. Same liability limits, same deductibles, same optional coverages. Subtle differences in what's covered can make rate comparisons meaningless.

Shop every single renewal after an accident, even if you like your current company. The competitive landscape shifts constantly. Whoever offered the best rate right after your crash might not be competitive two years later. I've watched clients cut their annual costs by $600 to $1,200 just by shopping consistently instead of assuming they already have the best deal

— Laura Adams

Look at non-standard or high-risk motorcycle insurance specialists if regular companies are quoting insane prices or refusing you outright. These companies expect riders with accidents and price accordingly. They often beat standard carriers' high-risk rates by 20% to 35%.

Ask about long-term rate projections when comparing quotes. Some insurers drop surcharges faster than others. A company with slightly higher first-year rates but faster surcharge reduction might cost less over the full five-year period than a competitor with lower rates today but extended penalties.

Frequently Asked Questions About Motorcycle Insurance After Accidents

Moving Forward After a Motorcycle Accident

Rate increases after crashes definitely sting, but understanding how the pricing works helps you fight back and plan smarter. That surcharge hammering you today isn't permanent. Keep your record clean for three to five years and your rates return to normal.

Focus on what you can control: finish safety courses, keep your coverage continuous, shop multiple companies at every renewal, and grab every discount you qualify for. These actions combined can cut your premium by 20% to 40% compared to just accepting whatever your insurer quotes you post-accident.

Think about the long-term value of accident forgiveness if you're planning to ride for years. Spending $100 annually for protection against a potential $800-per-year surcharge delivers strong returns over a typical riding lifetime.

Most importantly, don't let one crash end your riding. Millions of motorcyclists keep riding affordably after accidents by making informed insurance choices and proving they've improved their risk profile through safer riding. Your rates recover as the accident ages out of the lookback period. Keep your eyes on the road ahead instead of dwelling on what's already happened.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer insights and guidance on motorcycle accident insurance claims, settlement processes, liability issues, coverage limits, medical compensation, and related insurance matters, and should not be considered legal or financial advice.

All information, articles, and materials presented on this website are for general informational purposes only. Insurance policies, liability standards, settlement practices, and state regulations may vary by jurisdiction and insurer. The outcome of a motorcycle accident claim depends on the specific facts of the accident, available evidence, policy language, and applicable law.

This website is not responsible for any errors or omissions in the content, or for actions taken based on the information provided. Users are strongly encouraged to consult with a qualified attorney or licensed insurance professional regarding their specific motorcycle accident claim before making decisions about settlements, negotiations, or coverage disputes.