Damaged motorcycle lying on its side at urban intersection with ambulance lights in background after crash

Motorcycle Accident Disability Guide to Benefits, Claims, and Compensation

Your bike's lying in pieces at the impound lot. You're staring at a hospital ceiling, counting the days until discharge. Physical therapy starts next week—assuming you can figure out how to pay for it. Nobody mentioned during those first frantic hours in the ER that the real nightmare starts when you realize your job won't hold your position for six months of recovery. Or that your savings account will be empty in eight weeks.

What comes next? A confusing mess of disability programs, insurance policies, government forms, and medical documentation requirements. Let's untangle it.

What Qualifies as a Disabling Motorcycle Injury?

Breaking your wrist doesn't automatically unlock disability payments. Each program defines "disabled" differently, and those definitions matter more than your actual pain level. Social Security? They'll only consider conditions preventing any substantial work for at least twelve consecutive months—or conditions likely to cause death. Your private insurance company? They wrote a policy with their own definitions, usually starting generous ("own occupation") before switching to stricter tests ("any occupation") after two years.

Temporary vs. Permanent Disability Classifications

Temporary disability functions like financial life support while you heal. Your surgeon expects you back at work eventually, even if "eventually" stretches to nine months. Short-term policies typically cover you for three to six months, though some extend to a year. You're hurt badly, but medical science says you'll recover enough to work again.

Permanent disability splits into two categories that couldn't be more different. Permanent partial describes what happens when you've healed as much as you're going to, but you're left with specific limitations. Your knee won't bend past ninety degrees anymore—fine if you work a desk job, catastrophic if you install carpet for a living. You've lost grip strength in your right hand—manageable for most people, career-ending for a dental hygienist. Permanent total applies when medical evidence shows no realistic chance you'll handle substantial employment in any field, given your physical or mental condition.

Author: Caleb Thornton;

Source: spy-delhi.com

Why does this distinction matter so much? The category determines which doors open. Temporary claims get handled through workers' compensation (if applicable) and employer short-term plans. Permanent status unlocks Social Security programs, activates long-term private policies, and dramatically increases the settlement value personal injury attorneys can demand during negotiations with insurance companies.

Common Injuries That Lead to Long-Term Disability

Motorcycles wrap riders in precisely zero protective metal, creating predictable damage patterns when collisions occur. Here's what most commonly leads to long-term disability motorcycle accident injuries:

| Injury Category | Disability Level | Recovery Period | Permanent Damage Likelihood |

| Total spinal cord injury | Complete disability (100%) | No recovery expected | Nearly certain (95%+) |

| Partial spinal cord injury | Ranges 40-90% impairment | One to two years minimum | More likely than not (60-80%) |

| Serious traumatic brain injury | Typically 70-100% impairment | Eighteen months to three years | Highly probable (70-90%) |

| Moderate head trauma | Usually 30-60% impairment | Six months to a year and a half | Roughly even odds (40-60%) |

| Below-knee amputation | Generally 40-70% impairment | Six months to one year of rehab | Depends heavily on occupation (65-85%) |

| Third-degree burns covering one-third of body | Ranges 30-80% impairment | One to two years minimum | Moderate to high chance (50-70%) |

| Several complex fractures | Often 20-50% impairment | Six to eighteen months | Less than half (30-50%) |

| Nerve bundle damage in shoulder | Typically 30-60% impairment | One to two years or more | Moderate likelihood (40-65%) |

Severe road rash, even cases requiring skin grafts, rarely qualifies for long-term disability on its own. Add complications—persistent infections, damaged nerves underneath, five separate reconstructive procedures—and the picture changes. Claims adjusters generally view standard road rash as a temporary condition. Simple broken bones healing on schedule? Same treatment.

Brain injuries create particularly cruel situations. Six months after your crash, you look completely normal. No wheelchair, no visible scars, speaking clearly, walking fine. But you can't follow conversations in rooms with background noise anymore because your brain lost its ability to filter competing sounds. Your boss's instructions evaporate from your memory within minutes, forcing you to record every meeting and take obsessive notes just to function at half your previous capacity. Proving these invisible limitations requires expensive neuropsychological testing and physicians willing to write exhaustively detailed reports about your cognitive deficits.

Author: Caleb Thornton;

Source: spy-delhi.com

Types of Disability Benefits Available After a Motorcycle Crash

Multiple programs exist simultaneously, each with distinct eligibility requirements, benefit calculations, and processing timeframes. Most injured riders have no clue how many potential benefits they could claim.

Social Security Disability Insurance (SSDI)

SSDI provides income to workers who paid Social Security taxes through their paychecks and now meet the program's rigid disability standard. The Social Security Administration maintains an extensive manual (informally called the Blue Book) cataloging conditions that automatically qualify—specific spinal disorders at documented severity levels, traumatic brain injuries with particular measured deficits, amputations meeting defined criteria.

Your employment history determines eligibility before medical issues even enter the conversation. The general rule: forty total credits (roughly ten years of employment), including twenty credits earned during the ten years immediately before your disability began. Workers under thirty-one need fewer credits—the formulas get messy, but younger riders qualify with shorter work histories. Monthly payments averaged $1,537 nationwide in 2024, though your specific amount depends on lifetime earnings. Maximum benefits reach approximately $3,627 for high earners.

The waiting period creates genuine financial crisis. You must remain disabled for five complete months before benefits commence. Approved in month eight? Your first payment covers month six. Families who've already drained savings accounts and maxed credit cards covering bills while paychecks stopped find this gap devastating.

Supplemental Security Income (SSI)

SSI provides benefits to disabled individuals with almost no income and minimal assets, whether or not they worked enough to qualify for SSDI. Crashed your motorcycle at twenty-three before establishing substantial work history? SSI might represent your sole government option.

Asset limits are punishingly strict: no more than $2,000 in countable resources as a single person ($3,000 for married couples). Your primary residence and one vehicle don't count toward the limit, but most everything else does. Monthly payments max out at $943 for individuals in 2024, with the actual amount decreasing based on any other income you receive.

SSI offers one major advantage compared to SSDI: zero waiting period. Benefits begin the first full month following approval. However, deposit a $75,000 personal injury settlement into your checking account? You've instantly made yourself ineligible for SSI by exceeding resource limits—unless an attorney structured that money into a special needs trust beforehand.

Private Long-Term Disability Insurance

These policies—purchased independently or provided through employers—generally replace fifty to seventy percent of pre-injury earnings. They're usually more generous than Social Security, at least initially.

Most policies divide coverage into two distinct phases. The first phase (commonly the initial twenty-four months): you're deemed disabled if your specific job has become impossible. Software developer whose concentration problems prevent coding? Approved. Construction worker who can't lift more than ten pounds? Approved. The second phase (after twenty-four months): the definition narrows to "any occupation," meaning any job remotely suitable given your education, skills, and experience. Suddenly the insurer argues you could answer phones for eight hours daily, regardless of whether such positions actually exist at anything approaching your previous income.

Benefits start after an elimination period—typically ninety or one hundred eighty days. Purchased the policy yourself? You selected this waiting period. Employer-provided plans usually default to one hundred eighty days. Unlike Social Security's five-month wait that happens AFTER the elimination period ends, this represents the only waiting period.

The hidden problem? Private insurers battle claims aggressively. They'll deploy investigators to film you carrying groceries from your car, then claim that sixty-second activity proves full work capacity. They'll scan your social media hunting for photos—you're standing and smiling at your daughter's graduation, so clearly you can stand for an eight-hour retail shift (ignoring that you needed two days in bed recovering from that one outing). They'll schedule examinations with doctors on their payroll who somehow conclude you're work-ready in the vast majority of cases.

Veterans Disability Benefits for Service Members

Veterans hurt in motorcycle crashes can access VA disability compensation when a service connection exists. The crash doesn't need to occur during active duty—the relevant question is whether a service-connected condition contributed to the crash or worsened as a result.

Consider this scenario: Your PTSD from combat is service-connected at fifty percent. While riding, a truck backfires nearby, triggering a severe flashback that causes you to lose control and crash into a guardrail. That crash could qualify as service-connected. Or imagine you've got a service-connected thirty percent knee injury that was annoying but manageable before the crash—now that same knee needs complete replacement surgery due to crash trauma. You'd file for an increased rating.

VA compensation spans from $165.92 monthly at ten percent up to $3,737.85 monthly at one hundred percent, with supplemental amounts for dependents. Unlike Social Security, employment doesn't affect eligibility. A veteran with a one hundred percent rating can work full-time earning $120,000 annually while still collecting the entire $3,737.85 monthly benefit. The rating measures impairment severity, not employability.

Comparing four major benefit programs side-by-side:

| Benefit Type | Who Qualifies | Monthly Payment Amount | How Long Before Benefits Start | How Long Benefits Continue |

| Social Security Disability Insurance | Must have sufficient work credits plus medical condition expected to last a year or prove fatal | Average payment around $1,537 (formula uses your historical earnings) | Five full months of disability plus three to five months for application processing | Until you reach retirement age or medical improvement occurs |

| Supplemental Security Income | Must have under $2,000 in assets plus qualifying medical impairment | Maximum $943 (reduced dollar-for-dollar by other income sources) | First full month after approval with no mandatory waiting period | Continues as long as you remain disabled and financially eligible |

| Private long-term disability insurance | Must have active insurance coverage plus inability to perform specified job functions | Fifty to seventy percent of your previous salary | Ninety to one hundred eighty days after your disability starts | Until age sixty-five typically, or earlier based on specific policy caps |

| VA disability compensation | Must establish connection between military service and current condition | Ranges from $165.92 to $3,737.85 depending on your impairment rating | Retroactive to either your claim date or when the disability actually began | Usually permanent unless your condition improves substantially |

How to File a Disability Claim Following Your Motorcycle Accident

Simply declaring "I got hurt and can't work anymore" produces zero results. Programs demand specific evidence, assembled in specific ways.

Medical Documentation You'll Need

Your medical records form the entire foundation of your case. Social Security wants treatment documentation showing diagnosis, expected prognosis, attempted treatments, and—critically—functional limitations. A physician's note stating "this patient is disabled" carries absolutely no weight with claims examiners who've reviewed thousands of applications.

What actually moves cases forward:

Detailed functional assessments from treating physicians: How long can you sit before needing to change positions? Twenty minutes? An hour? Can you remain standing for fifteen consecutive minutes? Can you lift ten pounds occasionally, frequently, or never? Physicians must document these specific restrictions using clinical findings and examination results, not just repeat your subjective pain complaints.

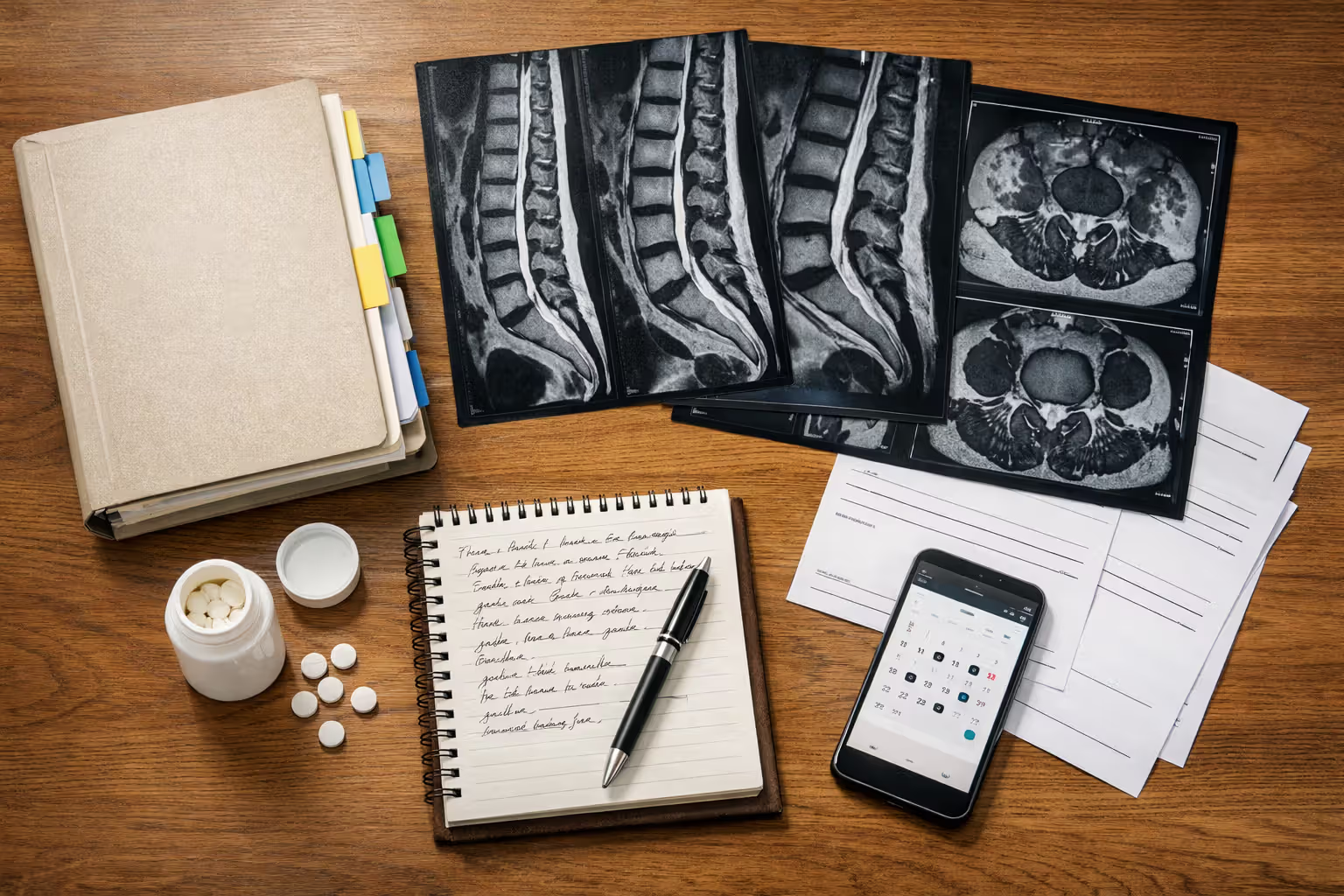

Objective medical testing: MRI images revealing which vertebrae are compressed and the compression degree. CT scans pinpointing brain injury location and extent. X-rays demonstrating that fractured bones aren't healing properly (non-union fractures). Pain remains subjective—examiners heavily discount complaints unsupported by imaging, laboratory results, and documented clinical observations.

Consistent treatment records: A four-month gap in medical visits raises massive red flags. If the pain truly prevents working, why haven't you seen your doctor in one hundred twenty days? Maintain treatment plans. Attend scheduled physical therapy sessions. Keep specialist appointments even when progress feels nonexistent.

Mental health documentation: Depression and anxiety commonly follow serious crashes, particularly those leaving permanent disfigurement or mobility restrictions. Don't skip mental health treatment thinking it's irrelevant—this documentation strengthens disability applications and provides crucial coping tools during massive life disruptions.

Frequent mistake: Riders wait until month eight to request a functional capacity evaluation from their physician when filing disability claims. If that evaluation happens at month eight post-crash, the doctor notes improvement since month three and expects further improvement ahead. That projection—"anticipate continued improvement"—destroys claims requiring proof of twelve-plus-month disability duration.

Author: Caleb Thornton;

Source: spy-delhi.com

Timeline Expectations for Different Benefit Types

SSDI initial applications require three to five months for decisions, longer for medically complex cases. Denied at initial level? Reconsideration adds another three to four months. Denied again and now requesting a hearing before an Administrative Law Judge (where eventual approvals most commonly occur)? Expect twelve to eighteen months from hearing request to actual hearing date. Many riders wait two full years or longer for final approval.

Private disability insurers operate faster in most situations. Short-term decisions: thirty to ninety days. Long-term approvals: sixty to one hundred twenty days. Some insurers issue provisional approvals, sending payments for six months while continuing evaluation.

VA disability claims average one hundred thirty to one hundred fifty days from submission to decision. Submit a "fully developed claim" including all supporting evidence upfront and you might get decisions in thirty to sixty days. Rating increases for existing service-connected conditions often process faster than brand-new claims.

Common Mistakes That Delay or Deny Claims

Inconsistent statements across different providers: Tell your orthopedic surgeon you can't sit longer than twenty minutes, then tell the Social Security consulting examiner you can manage an hour. That contradiction obliterates credibility. Remain consistent and honest.

Declining recommended treatments without valid medical reasons: Your orthopedic surgeon recommends spinal fusion surgery that could potentially restore significant function, and you refuse without legitimate medical justification? Expect denial. Programs require pursuing reasonable treatment options. Declining high-risk experimental procedures or treatments with documented poor success rates generally won't damage your case. Refusing standard medical interventions definitely will.

Earning above the substantial gainful activity threshold during application: For SSDI in 2024, monthly earnings exceeding $1,550 (or $2,590 if blind) typically trigger automatic denial for engaging in substantial gainful activity. Even part-time employment crossing that earnings threshold can destroy your claim.

Missing critical notification deadlines: Private policies commonly require disability notification within thirty to ninety days after disability begins. Blow that deadline? You might forfeit every dollar regardless of how legitimate your impairment is.

Incomplete application submission: Social Security returns incomplete applications, which resets your filing date and delays when retroactive benefits can begin. Gather everything first—complete work history spanning fifteen years, all treating physician names and complete addresses, comprehensive medication lists, pharmacy contact information—before starting the application process.

The single most critical factor in successful motorcycle accident disability claims is detailed, consistent medical documentation that explains not just what injuries you have, but specifically how those injuries prevent you from working. I've seen clients with severe injuries denied because their doctors wrote vague notes, and clients with moderate injuries approved because their physicians thoroughly documented every functional limitation

— Michael Richardson

Calculating Your Disability Compensation: What to Expect

Understanding how programs calculate payments helps you create realistic budgets during what might become years without regular employment income.

Factors That Determine Your Benefit Amount

SSDI calculates benefits using your Average Indexed Monthly Earnings calculated across your thirty-five highest-earning years. The formula applies different replacement percentages to different AIME portions, producing your Primary Insurance Amount. A worker who averaged $50,000 annually throughout their career might receive approximately $1,600 monthly. Someone averaging $100,000 might receive around $2,400. It's not a straightforward percentage of pre-disability income.

Private policies spell out exact calculation formulas in your specific contract. Most replace sixty percent of base salary (excluding bonuses, overtime, and commissions). A $75,000 annual salary generates $3,750 monthly in disability benefits. But here's the catch: most policies include offset provisions for other disability income. If you're collecting $1,500 from SSDI, the insurer reduces its payment to $2,250—you're still getting sixty percent total income replacement, just from combined sources instead of the insurer alone.

VA compensation depends purely on your disability rating. Your rating percentage (assessed in ten percent increments from zero to one hundred percent) determines the precise monthly amount from published compensation tables. Multiple service-connected conditions combine using VA's unusual math—a fifty percent rating combined with a thirty percent rating doesn't equal eighty percent; it equals sixty-five percent using their specific calculation methodology.

How Accident Settlements Affect Disability Payments

Personal injury settlements from at-fault drivers don't affect your SSDI benefits whatsoever. Social Security doesn't care whether you received $500,000 from the other driver's liability insurance—your monthly SSDI payment continues at the same amount. But simultaneous workers' compensation (because the crash occurred while making deliveries for your employer)? Social Security might reduce SSDI when combined benefits exceed eighty percent of your average current earnings before disability.

SSI treats settlements as both income and countable resources. A $100,000 settlement deposited directly into checking instantly disqualifies you from SSI—you've exceeded the $2,000 resource limit. Advance planning using properly drafted special needs trusts preserves SSI eligibility while still allowing access to settlement money for expenses SSI doesn't cover.

Private disability insurers frequently include settlement offset language. If your policy covers injuries "from any cause," insurers might claim your settlement should reimburse them for benefits they've already paid. Or they'll argue the settlement proves you received compensation for wage loss, reducing what they owe going forward. Policy language varies dramatically—carefully review your actual contract before accepting any settlement offer.

Workers' compensation settlements sometimes trigger Social Security offsets. Social Security calculates your average current earnings before disability, then reduces SSDI if workers' comp combined with SSDI exceeds eighty percent of that figure. Strategic workers' comp settlement structuring—using Medicare set-asides or specific allocation language—can sometimes minimize this offset.

When Your Disability Claim Gets Denied: Next Steps

Roughly sixty-five percent of initial SSDI applications receive denials. Private insurers deny twenty to thirty percent of long-term disability claims. Denial doesn't end the process.

Understanding Why Motorcycle Injury Claims Are Rejected

Insufficient medical evidence supporting claimed limitations: The overwhelmingly most common reason. Examiners couldn't locate objective proof of your alleged restrictions, or physician documentation lacked specificity about functional capabilities.

Disability duration too short: Social Security denied because evidence suggests recovery within twelve months. A complicated femur fracture might disable you for ten months, falling two months short of minimum duration requirements.

Excessive earnings: Your earnings during the alleged disability period exceeded substantial gainful activity levels, or evidence suggests capacity to perform some work despite limitations.

Failure to comply with treatment: You didn't take prescribed medications consistently, missed numerous physical therapy appointments, or refused recommended medical procedures without legitimate medical justification for refusal.

Insufficient clinical findings: You report disabling pain levels but imaging studies appear essentially normal and physical examination doesn't reveal corresponding clinical abnormalities. This particularly impacts soft tissue injuries and mild traumatic brain injuries with normal CT/MRI results.

Private insurers add additional reasons: surveillance footage capturing you performing activities contradicting claimed limitations, social media posts (photographs from your niece's wedding reception showing you standing and socializing), or their hired independent medical examiners disagreeing with your own treating physicians' conclusions.

The Appeals Process Explained

For SSDI, you get sixty days from the denial notice date to request reconsideration. A different claims examiner reviews your complete file—you can submit additional medical evidence. Approval rates at reconsideration hover around thirteen percent nationally, which sounds discouraging, but the appeal preserves your protective filing date while preparing for subsequent levels.

Denied at reconsideration? You've got another sixty days to request an ALJ hearing. This stage produces the majority of eventual approvals. You'll testify personally about your limitations. Vocational experts may testify. Your attorney will cross-examine witnesses and present medical evidence. Approval rates at the hearing level reach forty-five to fifty percent. Current hearing wait times run twelve to eighteen months in most regions.

Beyond hearings lie the Appeals Council and federal district court, but these levels review legal errors and procedural mistakes rather than re-examining medical evidence.

Private insurers typically offer one or two internal administrative appeal levels before litigation becomes necessary. ERISA governs most employer-sponsored plans, significantly limiting available remedies and eliminating jury trial rights. Individually purchased policies may allow broader legal challenges and remedies.

Appeal timing carries enormous consequences. You could file a brand-new SSDI application instead of appealing, but you'd lose your protective filing date. If eventually approved through appeals, benefits retroact to your original application date. File new applications and you only receive retroactive benefits to the new filing date—potentially losing years of back payments. For private insurance, missing appeal deadlines may permanently terminate your rights to benefits under the policy terms.

During appeals, continue treating with your physicians and documenting limitations. If your condition deteriorates, that strengthens your case significantly. If you attempt returning to work and fail due to your limitations, carefully document that failed work attempt—it can actually help prove you cannot sustain employment despite genuine desire to work.

Author: Caleb Thornton;

Source: spy-delhi.com

Maximizing Your Total Compensation: Combining Multiple Benefits

Severely injured riders may simultaneously qualify for multiple benefit sources. Understanding interaction between programs prevents costly mistakes.

SSDI and VA compensation stack completely—both programs pay full benefits without any offsets. A veteran receiving $3,000 monthly in VA disability compensation and $1,800 in SSDI receives the full $4,800 combined.

SSDI and private long-term disability interact through your specific LTD policy's offset provisions. If your policy pays sixty percent of income and offsets SSDI dollar-for-dollar, the insurer pays sixty percent minus your SSDI amount. You still receive the full sixty percent income replacement rate—just split between two funding sources.

Personal injury settlements typically stack on top of disability benefits completely. You might collect $2,000 monthly in SSDI, $1,500 from private disability insurance, and a $500,000 settlement from the at-fault driver's liability carrier. The settlement doesn't reduce your monthly benefits (except in workers' comp situations or for SSI recipients subject to resource limits).

Workers' compensation creates complications and potential offsets. If your motorcycle accident occurred while performing employment duties—delivering food for a restaurant, traveling between job sites as a service technician—workers' comp covers medical treatment and provides wage replacement benefits. But Social Security offsets SSDI when combined workers' comp and SSDI payments exceed eighty percent of pre-disability earnings. Several states flip this arrangement, offsetting workers' comp when you receive SSDI instead.

Strategic settlement structuring becomes crucial. Allocating more settlement dollars specifically to future medical expenses versus wage loss can reduce offsets in particular situations. Spreading lump-sum payments across multiple years through structured settlements might preserve SSI eligibility by keeping annual income below program thresholds.

Often overlooked benefit: Medicare eligibility. SSDI recipients automatically qualify for Medicare after collecting disability benefits for twenty-four months, regardless of age. This provides essential coverage for ongoing treatment of motorcycle injuries. Medicare becomes the secondary payer if you maintain other insurance coverage, filling coverage gaps.

Tax treatment varies significantly by benefit source. SSDI becomes partially taxable if total household income exceeds certain thresholds. If your employer paid disability insurance premiums pre-tax, those benefits face taxation. If you paid premiums using after-tax dollars, benefits arrive tax-free. VA disability compensation never faces federal or state taxation under any circumstances. Personal injury settlements for physical injuries generally arrive tax-free, though portions specifically allocated to punitive damages or pure emotional distress might face taxation.

Frequently Asked Questions About Motorcycle Accident Disability

Moving Forward After a Disabling Motorcycle Accident

Navigating disability benefits after serious crashes demands patience, meticulous organization, and relentless persistence. Managing chronic pain while attending multiple weekly medical appointments and watching unpaid bills accumulate creates overwhelming stress.

Start by collecting complete medical records and identifying which programs match your specific situation based on work history, military service, and insurance coverage. Don't assume one denial means permanent rejection—the majority of approvals occur only after initial denials, during later appeals stages.

Consider carefully how different benefit sources interact with each other. Accepting a lump-sum workers' comp settlement might trigger Social Security offsets. Failing to properly structure a personal injury settlement could eliminate SSI eligibility entirely. These decisions carry long-term financial consequences worth professional guidance.

Most importantly, prioritize your actual medical treatment and recovery above everything else. Your disability claim's strength rests entirely on documented medical evidence of specific functional limitations. Attend every scheduled appointment, follow treatment recommendations carefully, and communicate clearly with physicians about exactly how injuries limit your daily activities and work capacity. Administrative and legal processes will consume months or years, but thorough medical documentation builds the essential foundation supporting every benefit you pursue.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer insights and guidance on motorcycle accident insurance claims, settlement processes, liability issues, coverage limits, medical compensation, and related insurance matters, and should not be considered legal or financial advice.

All information, articles, and materials presented on this website are for general informational purposes only. Insurance policies, liability standards, settlement practices, and state regulations may vary by jurisdiction and insurer. The outcome of a motorcycle accident claim depends on the specific facts of the accident, available evidence, policy language, and applicable law.

This website is not responsible for any errors or omissions in the content, or for actions taken based on the information provided. Users are strongly encouraged to consult with a qualified attorney or licensed insurance professional regarding their specific motorcycle accident claim before making decisions about settlements, negotiations, or coverage disputes.