Damaged sport motorcycle lying on asphalt at urban intersection after collision with car, police vehicle with flashing lights in background

How to File a Motorcycle Accident Property Damage Claim Step by Step

Crash your bike, and you're suddenly fighting on two fronts. The first battle? Getting your body healed. The second? Wrestling a fair payout from insurance adjusters who'd rather lowball your claim than cover what your damaged motorcycle actually costs to fix or replace.

Here's what most riders don't realize until it's too late: property damage claims operate under completely different rules than personal injury cases. You're working against tighter deadlines—sometimes half as long. Insurers use valuation tricks they'd never attempt with medical bills. And the negotiation tactics that work for injury settlements often backfire when you're arguing over whether your 2020 Hayabusa needs OEM fairings or cheap knockoff plastic.

Miss these distinctions, and you'll cash a settlement check that falls $3,000-5,000 short of what you actually needed. Know how to navigate this process, and you'll walk away with enough to either fix your ride properly or replace it with something comparable.

What Qualifies as Property Damage in Motorcycle Accident Claims

Look beyond your mangled bike. Insurance should cover everything that got destroyed in the collision, but adjusters will pretend the damage stops at your frame and bodywork if you let them.

Bike damage vs. total loss determinations

Your insurer totals your motorcycle when fixing it costs anywhere from 70-80% of what they calculate as actual cash value. The exact percentage depends on which state you're in and which company you're dealing with.

Here's where it gets messy. Let's say you own a 2019 Yamaha R6 showing 12,000 miles. NADA guide says it's worth $8,500. Repair estimate comes back at $6,800. Math says the bike's fixable, but your insurer declares it totaled anyway because $6,800 hits 80% of that $8,500 valuation. You wanted your baby repaired; they're cutting you a check for the depreciated value instead.

Total loss fights get really ugly when you've customized your ride. That Akrapovic exhaust system you installed for $3,000? The suspension work that ran $1,500? Insurance will maybe—maybe—add 50 cents on the dollar to your base value. And only if you kept every receipt and specifically told them about modifications when you bought your policy. Most riders discover this gap too late.

Author: Ryan Whitlock;

Source: spy-delhi.com

Sometimes insurers approve repairs initially, the shop starts tearing down your bike, and boom—they find cracked frame tubes nobody could see under the fairings. Now you're filing a supplemental claim. The adjuster has to come back out. Timeline resets. And that "repairable" motorcycle you were counting on? Suddenly it's totaled because repair costs just jumped another $4,000.

Additional property covered beyond the motorcycle

Your claim shouldn't stop at the bike—that's exactly what insurers hope you'll assume.

Riding gear takes serious damage in crashes. Your helmet absorbed a $600 hit to save your skull. That leather jacket showing road rash cost $800. Pants, gloves, boots—quality gear runs $1,000-2,000 for a complete set. None of this appears in the initial claim unless you itemize every piece with either purchase receipts or current replacement costs.

Check your pockets and storage compartments. Phone shattered when you hit the pavement? That's $800-1,200 right there. Tank bag containing your laptop? Another $200 for the bag, $800-1,500 for the computer. GPS unit, phone mount, action camera, saddlebags—all legitimate property damage.

Sometimes your crash damages stuff that isn't yours. Maybe you swerved avoiding some idiot who cut you off and took out somebody's fence. Their mailbox. Their landscaping. That becomes third-party property damage under your liability coverage, usually handled as a separate claim from your own motorcycle damage.

Step-by-Step Process for Filing Your Motorcycle Damage Claim

What you do in the first hour after impact directly determines whether you'll get paid fairly or get screwed.

Immediate actions at the accident scene

Pull out your phone and shoot 20-30 photos minimum. Multiple angles of all vehicles. Road conditions. Skid marks. Debris scattered across the pavement. Get shots of the other driver's license plate—the actual plate, not them telling you the number. Photograph their insurance card directly. Their driver's license too.

Write down witness contact information before they leave. Names, phone numbers, emails. People vanish within minutes of a crash, and their statements become critical when the other driver suddenly claims you ran a red light.

Call the other driver's insurance company right there at the scene if you can—use that 24-hour claims number on their insurance card. Verify the policy's actually active. I've seen riders waste weeks pursuing claims against expired policies.

Make a police report regardless of how minor the damage looks. Some insurers won't process claims over $1,000-2,500 without an official report. More importantly, that report creates a government record of fault before the other driver changes their story—which happens more often than you'd think.

Author: Ryan Whitlock;

Source: spy-delhi.com

Never discuss who caused the crash while standing there. Don't apologize even if you're Canadian and apologizing is basically involuntary. Statements like "my bad, didn't see you" get twisted into liability admissions that tank your claim.

Contacting insurance companies (yours vs. at-fault driver's)

You've got two paths here: file through the at-fault driver's liability coverage (third-party claim) or use your own collision coverage (first-party claim).

Third-party claims avoid your deductible and keep your insurance rates clean. But they crawl along because that other insurer owes you nothing contractually. They'll investigate fault exhaustively. If they decide their driver was only 60% responsible—or worse, not responsible at all—they'll slash or deny your claim entirely.

First-party claims through your collision coverage move faster since your own insurer has contractual obligations to process claims promptly. You'll front your deductible, but they handle everything and then chase the at-fault party through subrogation to recover costs, including your deductible eventually.

Pick based on fault clarity. When liability's obvious and the other insurer admits fault quickly, go third-party and save your deductible. When fault's murky or the other driver's uninsured, file first-party and get paid now instead of fighting for months.

Call both insurers within 24-48 hours no matter which route you choose. Policies demand "immediate" or "prompt" notice. Wait three weeks, and they might deny coverage entirely.

Required documentation and evidence

Building a solid claim requires more than just photos of bent metal.

Walk around your motorcycle immediately and create a written damage inventory. Every component. Scratched mirror? Write it down. Cracked turn signal lens? List it. Scraped engine case? Document it. Nothing's too minor to note.

Dig up maintenance records proving your bike's condition before the crash. Recent service showing proper maintenance supports higher valuation and counters insurance arguments that pre-existing neglect contributed to damage severity.

Find purchase receipts for every accessory and modification. Without that receipt for your aftermarket exhaust, the insurer might add $200 to your valuation instead of the $1,200 you actually paid.

Hunt down pre-accident photos if you've got them. Instagram posts from last month's ride, Facebook photos, marketplace listings if you bought the bike recently—anything establishing baseline condition before the collision.

Get repair estimates from at least two licensed motorcycle shops—three is better. Never depend on just the insurance company's number. Independent estimates from shops with solid reputations give you negotiating leverage, especially when they identify damage the adjuster "missed."

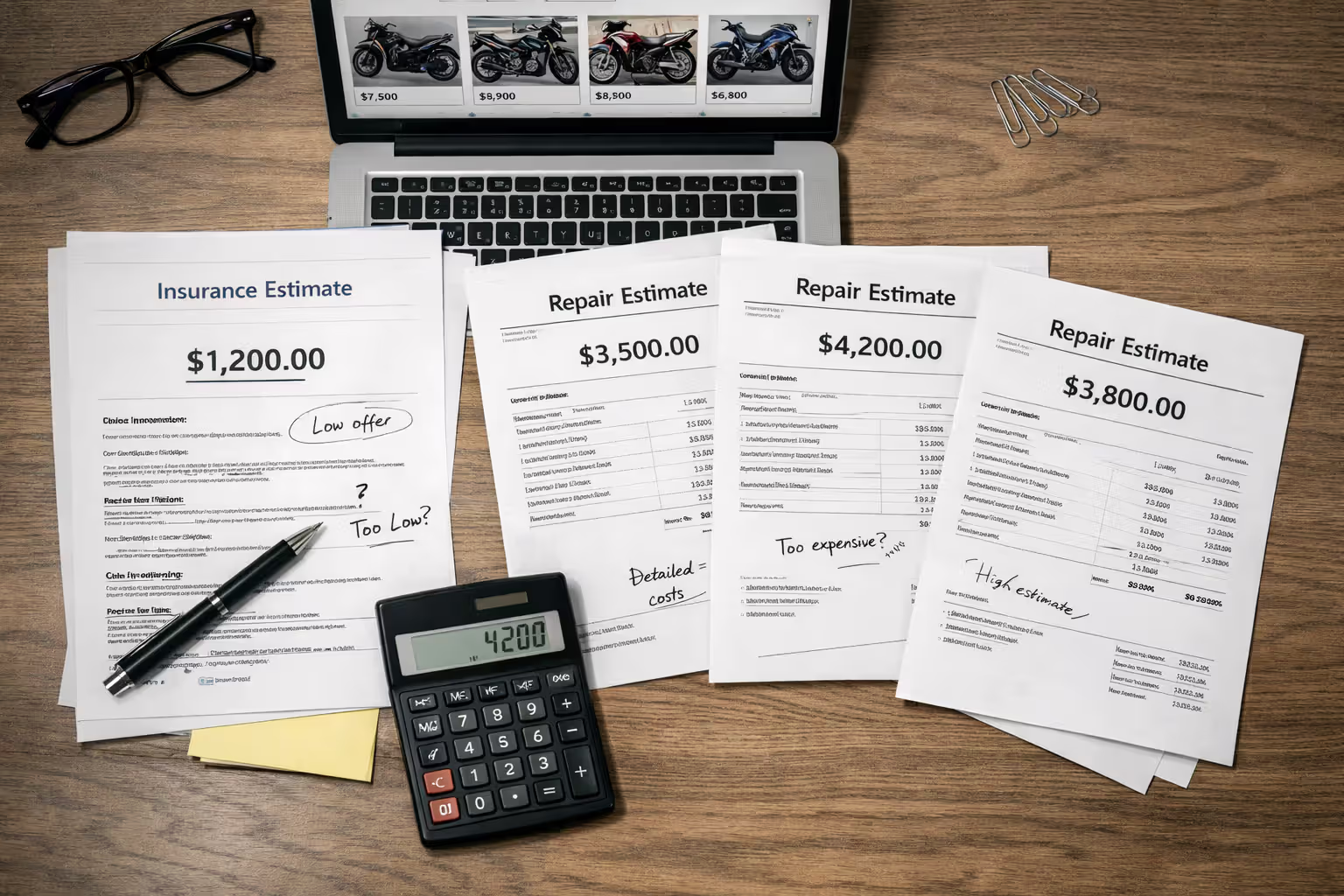

How Insurance Companies Assess Motorcycle Repair Costs

Watch how insurers strategically minimize payouts through their valuation methods, and you'll understand why that initial offer always feels low.

Independent adjuster inspections

Insurance dispatches adjusters to inspect your bike, but calling them "independent" is generous. These adjusters either work directly for the insurer or for firms that get paid by insurers. Guess whose interests they protect?

Typical inspection takes maybe 15-30 minutes. They photograph damage, tap some numbers into proprietary software like CCC ONE or Mitchell, and generate an estimate using standardized labor rates and parts prices—frequently below actual market rates in your specific area.

Many adjusters write estimates covering only visible damage. Hidden damage won't show up until teardown. This creates supplemental claims that restart the process and add weeks to your timeline.

Watch for adjusters claiming certain damage was "pre-existing." They'll point to rust, normal wear, paint oxidation—anything to attribute damage to age instead of the accident. This tactic cuts claim costs by blaming you for maintaining an older bike. Counter this with pre-accident photos and maintenance records.

Repair shop estimates vs. insurance valuations

The gap between what shops actually charge and what insurance wants to pay creates the central fight in most property damage claims.

| Cost Category | What Insurance Estimates | What Shops Actually Charge | How to Fight Back |

| Labor Rate | $85-95/hour from database averages | $110-140/hour at actual local shops | Call three shops, document their rates, demand "prevailing rate" adjustment |

| Parts Quality | Aftermarket or salvage when available | OEM matching your original equipment | Insist on OEM for bikes under 5 years; cite state laws requiring OEM |

| Paint/Refinish | Single-stage paint, basic matching | Multi-stage paint, precision color matching | Document original paint specs; custom colors require manufacturer-spec paint |

| Hidden Damage | Excluded until teardown reveals it | Pre-estimated based on impact force | Demand complete teardown inspection before finalizing anything |

| Betterment | 20-40% deduction claiming "improvement" | Zero deduction—repairs restore condition | Challenge any deduction over 15% on structural parts |

Shops write estimates reflecting their actual costs. Insurance estimates reflect their desired payment—usually 15-25% below shop reality.

This gap forces you into three choices: negotiate the difference, pay out-of-pocket for the gap, or find some shop willing to accept insurance money by cutting corners. Understanding this isn't about good estimates versus bad estimates—it's about opening offers versus fair payment.

OEM parts vs. aftermarket parts disputes

Aftermarket parts cost insurers 30-50% less than OEM components. Most states let them specify aftermarket parts for vehicles over 3-5 years old.

Motorcycles suffer more than cars here. Aftermarket car bumpers and fenders are everywhere. Aftermarket motorcycle parts? Fitment issues, inferior materials, missing warranties. Common problems across the board.

Premium bikes get hit hardest. Genuine Ducati fairing: $1,800. Aftermarket version: $600. But that cheap fairing won't fit right, won't match the paint perfectly, and might crack after six months.

Fight aftermarket parts multiple ways:

Check your policy language first. Some policies guarantee OEM regardless of age.

Raise safety concerns. Aftermarket brake parts, suspension components, or wheels might not meet manufacturer safety specifications.

Document fitment failures. Aftermarket parts that don't fit properly force insurers to pay for OEM alternatives.

Reference state laws. Several states require insurers to disclose aftermarket parts use and get your written consent first.

Common Mistakes That Reduce Your Property Damage Settlement

Most riders accidentally sabotage their own claims through errors that seem minor but cost thousands.

Jumping on the first offer without pushing back. Adjusters build negotiation room into initial offers—typically 10-20% below their authorization limit. Accept immediately, and you're leaving $1,500-3,000 on the table. They expect negotiation. Give it to them.

Author: Ryan Whitlock;

Source: spy-delhi.com

Forgetting to claim everything beyond the bike itself. Riders fixate on motorcycle damage and completely forget about $2,000 worth of riding gear, electronics, and accessories. Insurance won't include items you don't specifically claim.

Starting repairs before the estimate's finalized. Once teardown begins, your leverage evaporates. The shop's committed. You're stuck. Lock down the complete estimate—including supplements for hidden damage—before authorizing any work.

Accepting the insurer's valuation without research. Check Cycle Trader, Facebook Marketplace, local dealer asking prices. If comparable bikes sell for $2,000-3,000 above the insurance valuation, you've got ammunition for negotiation.

Signing releases prematurely. Property damage releases are separate from injury releases, but both are final. Can't reopen the claim after signing. Ever. Don't sign anything until you're absolutely certain the settlement covers all damage.

Ignoring diminished value entirely. Perfect repairs don't erase accident history. Carfax reports kill resale value by 10-25% even on bikes fixed flawlessly. Diminished value claims recover this loss, but insurers never mention them voluntarily. You have to demand them specifically.

Blowing past deadlines. Property damage claims hit shorter statutes of limitations than injury claims—often 2-3 years versus 3-4 years for bodily injury. Miss the deadline, and your claim dies completely.

Timeline: What to Expect During the Motorcycle Insurance Claim Process

Knowing realistic timeframes helps you spot when insurers are stalling versus when processes just take time.

Days 1-3: Reporting and assignment. You call in the accident. Insurer opens your file. Adjuster gets assigned. Happens fast with your own insurer—usually under 24 hours. Third-party claims take 2-3 days.

Days 4-7: Inspection and initial estimate. Adjuster schedules inspection, examines your bike, writes preliminary estimate. Should happen within a week of reporting. Third-party claims sometimes drag longer here.

Days 8-14: Review and negotiation. You get their estimate. Obtain independent shop estimates. Negotiate gaps between their numbers and reality. Duration varies wildly depending on damage severity and whether you accept their initial offer.

Days 15-21: Teardown and supplemental estimates. Authorize repairs, shop tears down your motorcycle, hidden damage emerges. Adjuster must re-inspect and approve supplements. Adds minimum 5-7 days, sometimes longer if the adjuster's juggling multiple claims.

Weeks 4-8: Actual repairs. Repair duration depends on parts availability and shop workload. Simple stuff takes 2-3 weeks. Extensive damage needing custom paint or rare parts can stretch 6-8 weeks or more.

Weeks 8-10: Final inspection and payment. Insurer inspects completed work, processes final payment, closes your file. Settlement check arrives, or the shop gets direct payment.

Total loss claims skip the repair phase entirely. Expect settlement within 2-4 weeks if you accept their valuation. Longer if you negotiate.

Delays exceeding these windows signal problems. Claim stalled three weeks with no explanation? Escalate to the adjuster's supervisor. File a state insurance department complaint. Most states require acknowledgment within 15 days and settlement decisions within 30-45 days maximum.

Author: Ryan Whitlock;

Source: spy-delhi.com

When to Dispute a Low Property Damage Offer

Not every settlement deserves your signature. Recognize when to fight back instead of accepting inadequate payment.

Red flags in settlement offers

Several warning signs scream "this offer's garbage":

Valuation falls $2,000-3,000 below recent sales of comparable bikes in your area. Pull current listings from Cycle Trader, Facebook Marketplace, local dealers. Similar bikes with comparable mileage selling significantly higher? The valuation's suspect.

Labor rates run 20-30% below what reputable shops actually charge locally. Make three quick calls to local motorcycle shops asking their hourly labor rates. Shops charging $120-140/hour while the estimate uses $85/hour? That's artificially deflated.

Excessive betterment deductions without clear justification. Reasonable betterment on high-wear items like tires or brake pads: 10-15%. Charging 40% betterment on body panels or frame components? Ridiculous. These parts restore condition; they don't improve anything.

Refusing to include documented accessories without valid reasons. You've got receipts and photos proving $5,000 in accessories? Insurer must account for them. Blanket denials signal bad faith.

Excluding sales tax, registration fees, and other mandatory replacement costs. Most states require these in total loss settlements. Omitting them shorts you several hundred dollars minimum.

Negotiation strategies and documentation needed

Winning negotiations demands preparation, not just complaints.

Build a counteroffer package with comparable sales data. Print 5-10 listings for similar motorcycles currently for sale nearby. Highlight anything priced above the insurer's offer. Include sold listings if accessible—these prove actual market value, not just asking prices.

Get written estimates from reputable shops on letterhead. Verbal quotes mean nothing. Written estimates showing higher repair costs force adjusters to justify their lower numbers specifically.

Document your bike's superior condition or desirable features comprehensively. Lower mileage, recent professional maintenance, popular color combinations, desirable model years—all support higher valuations. Service records, receipts, pre-accident photos prove these claims concretely.

Request the insurer's valuation report and challenge specific items directly. Insurers must disclose their calculation methodology. Review it for errors: wrong mileage entries, incorrect options packages, inappropriate comparable vehicles from different markets.

Cite your state's regulations requiring fair market value. Most states mandate insurers pay "fair market value" or "actual cash value" based on local conditions, not national database averages. If your state has specific valuation requirements, reference them explicitly.

Insurers bank on policyholders accepting initial offers without question. That first valuation typically represents the minimum the adjuster thinks they can pay without getting challenged, not the maximum they're authorized to spend. Policyholders who present organized, well-documented counteroffers routinely secure settlements 15-30% higher than initial offers. Proving your motorcycle's value through actual market data works infinitely better than emotional appeals about sentimental attachment

— Jennifer Martinez

Consider hiring a public adjuster or attorney for high-value disputes. If your bike was worth $20,000+ or the dispute involves complex custom modifications, professional representation pays for itself. Public adjusters typically charge 10-15% of the settlement but often boost payouts 30-50%.

Know when escalation makes sense. Negotiation stalling out? File a complaint with your state insurance department. Regulators investigate and can pressure insurers toward fair settlement. Costs you nothing and frequently produces results within weeks.

Frequently Asked Questions About Motorcycle Property Damage Claims

Conclusion

Filing a motorcycle accident property damage claim successfully requires meticulous documentation, strategic thinking, and willingness to negotiate hard. Insurance companies rarely open with fair offers, and riders who accept without challenging leave substantial money unclaimed.

Start by documenting everything at the accident scene and cataloging all damage to your motorcycle comprehensively. Understand the strategic differences between filing through your own collision coverage versus the at-fault driver's liability coverage, then choose based on fault clarity and urgency. Gather multiple repair estimates, research your motorcycle's actual market value thoroughly, and remember to claim damaged gear and accessories beyond just the bike.

When settlement offers arrive, scrutinize them carefully. Compare valuations against recent sales of comparable motorcycles in your specific area. Verify that labor rates match local shop rates and parts quality meets OEM standards. Challenge excessive betterment deductions aggressively and counter lowball offers with organized, well-documented responses.

Remember that property damage claims move faster than injury claims but carry shorter filing deadlines. Act promptly, maintain detailed records of every communication, and refuse signing releases until you're completely certain the settlement fully compensates all losses. When disputes arise, escalate strategically—from the assigned adjuster to their supervisor to state regulators when necessary.

Your motorcycle represents significant investment, and you deserve fair compensation when someone else's negligence damages it. Armed with knowledge of how claims actually work and willingness to advocate firmly for yourself, you can navigate this system successfully and secure settlements that actually cover your losses.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer insights and guidance on motorcycle accident insurance claims, settlement processes, liability issues, coverage limits, medical compensation, and related insurance matters, and should not be considered legal or financial advice.

All information, articles, and materials presented on this website are for general informational purposes only. Insurance policies, liability standards, settlement practices, and state regulations may vary by jurisdiction and insurer. The outcome of a motorcycle accident claim depends on the specific facts of the accident, available evidence, policy language, and applicable law.

This website is not responsible for any errors or omissions in the content, or for actions taken based on the information provided. Users are strongly encouraged to consult with a qualified attorney or licensed insurance professional regarding their specific motorcycle accident claim before making decisions about settlements, negotiations, or coverage disputes.