Motorcyclist in full gear standing beside a damaged motorcycle on road shoulder while holding a smartphone camera

How to File a Motorcycle Accident Insurance Claim Successfully

Getting hit while riding changes everything in an instant. You're dealing with injuries, a damaged bike, and now you've got to figure out how insurance companies work. Here's the thing: most riders leave thousands on the table because they don't know what actually matters during the claims process. Let me walk you through what really works, based on what separates successful claims from disappointing ones.

What to Do at the Accident Scene Before Filing Your Claim

Those first minutes after impact? They make or break your entire case. Insurance adjusters will pick apart every detail later, so what you capture now directly determines whether they believe your version of events.

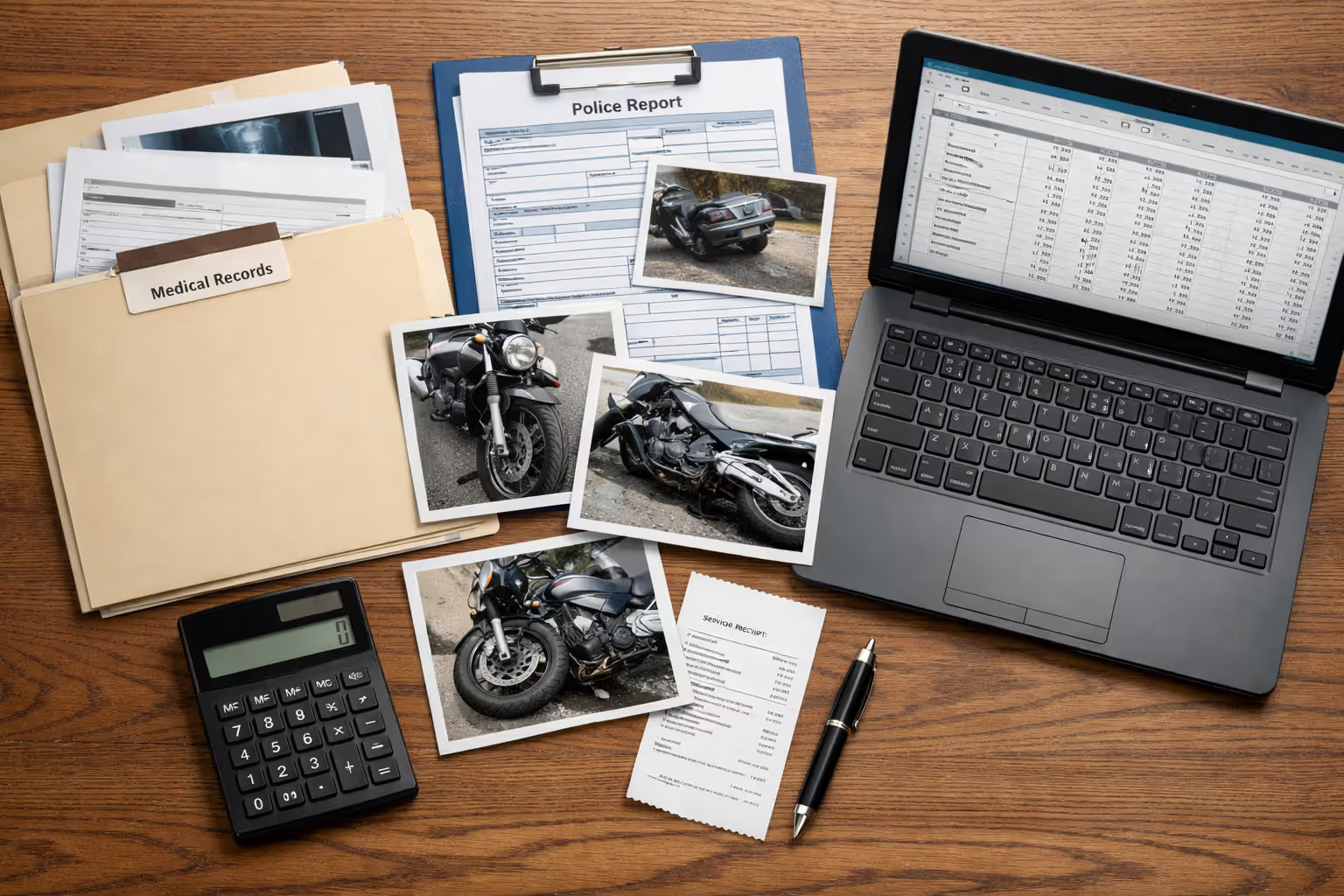

Document Everything: Photos, Videos, and Witness Information

Pull out your phone and start shooting from every angle you can manage. Show where each vehicle ended up, any skid marks on the pavement, the position of traffic signals, what the weather looks like. Get close-ups of every dent, scrape, and broken part on your motorcycle. Don't forget the other vehicle's damage and any visible cuts or road rash.

Here's what most people miss: take a video while walking around the entire scene. Narrate what you're seeing. That 30-second clip shows spatial relationships that individual photos never capture—where that blind corner is, how close that stop sign sits to the intersection, whether sun glare could have been a factor.

Now for witnesses. Record their contact details in your phone: full names, phone numbers, email if they'll give it. Here's how I phrase it: "Would you mind writing down what you saw, just a few sentences?" Most people will, especially if you make it easy by handing them your phone to type into. Witnesses who aren't related to either driver carry massive weight when the other party tries claiming you ran a red light.

Don't count on the responding officer to track down witnesses. At minor accidents, they frequently write up the report and leave without interviewing bystanders who saw everything.

Trade insurance details with other involved drivers—company names, policy ID numbers, vehicle registration info—but keep your mouth shut beyond that. Even saying "my bad" or "I should've seen you sooner" gets weaponized against you. Stick to swapping information, nothing more.

When to Call Police vs. Handle It Privately

Always dial 911 if anybody's hurt, if vehicles can't be moved safely, or if the other driver seems drunk or high. Any accident involving injuries or major property damage legally requires police documentation in nearly every state.

Some riders think about skipping the police call for fender-benders to avoid insurance rate hikes. This backfires spectacularly. Without an official report, the other driver can—and often does—completely change their story two days later. They'll claim you sideswiped them, that the accident never even happened, or that you fled the scene. I've seen it dozens of times.

Even minor-looking damage can hide thousands in repairs. Motorcycles have sensitive components and frame issues that don't show up until a mechanic gets underneath.

Before you leave, write down the report number the officer gives you. You'll reference this number repeatedly while filing your claim.

Author: Caleb Thornton;

Source: spy-delhi.com

Medical Attention: Why Immediate Treatment Strengthens Your Claim

Adrenaline is a liar. You feel fine right now, but whiplash, soft tissue injuries, and concussions often don't announce themselves until hours or even days later. Getting examined within 24 hours creates medical documentation that directly connects your injuries to the crash.

Here's what claims adjusters hunt for: treatment gaps. Wait five days to see a doctor? They'll argue your injuries can't be that serious, or that you got hurt doing something else between the accident and your doctor visit. Emergency rooms create the strongest paper trail, though urgent care facilities or your regular doctor work too.

One critical boundary: never sign medical authorization forms that the other driver's insurance company sends you. These releases grant them access to your complete medical history going back years. They'll dig up that knee surgery from 2015 or your chronic back pain and blame your current injuries on pre-existing conditions.

Step-by-Step Process to File Your Motorcycle Accident Claim

Filing correctly the first time saves you months of delays and prevents denials. Here's the exact sequence that works.

Notifying Your Insurance Company (Timing and What to Say)

Your policy probably requires notification within 24 to 72 hours after an accident—exact deadlines live in your policy's declarations page. Missing this window can void coverage completely, even when you did nothing wrong.

When you make that first call, share the bare minimum: what day and time it happened, where it occurred, who else was involved, and that you're planning to file a claim. Tell them you're still collecting information and will provide detailed statements later. This approach satisfies your reporting requirement without locking you into a version of events before you've gathered all the facts.

Skip the detailed play-by-play during this initial call. Adjusters record these conversations. When you're stressed, confused, and working from incomplete information, you'll say things that contradict your later statements or accidentally admit fault.

Gathering Required Documentation and Evidence

Your claim needs serious supporting documentation beyond accident scene photos. Build a file containing:

- The official police report (request it from the department within 7-10 business days)

- Every medical record and bill from all treatment providers

- At least two repair estimates for your motorcycle

- Documentation of missed work and lost income (recent pay stubs, a letter from your employer on company letterhead)

- Every receipt related to the accident—towing fees, rental vehicle costs, damaged riding gear that needed replacing

- Your motorcycle's service history proving its pre-accident condition

Create a detailed timeline that tracks every medical appointment, every phone conversation with insurance adjusters, and every dollar you've spent. This becomes absolutely invaluable when your claim drags on for months.

Completing the Claim Forms Without Hurting Your Case

Insurance claim forms feature open-ended questions specifically designed to get you to limit their liability. When describing how the accident happened, report only what you directly observed. Write "The other vehicle turned left directly into my path" instead of "I think they didn't see me because they were distracted by their phone."

Never guess about injuries. If a form asks you to list all injuries but you're still undergoing diagnostic testing, write "currently under medical evaluation" rather than listing specific conditions you're uncertain about. Adding new injuries later makes you look dishonest; leaving out known injuries means you can't claim compensation for them.

Photocopy everything before mailing it. Write the submission date and the assigned adjuster's name on your copies.

Author: Caleb Thornton;

Source: spy-delhi.com

What Happens After You Submit Your Claim

The insurance company assigns a claims adjuster who investigates by reviewing your documentation, talking to everyone involved, and evaluating the damage. They might send an appraiser to physically inspect your motorcycle or request additional medical records.

Expect your first contact from them within 5-7 business days. The adjuster will almost certainly ask for a recorded statement. Here's what they won't tell you: you're not legally obligated to give one to the other driver's insurance company. For your own insurer, your policy might require it, but you can ask for time to prepare or request that your attorney be present.

Eventually the adjuster makes a settlement offer. This first number is practically always lower than what they'll actually pay. They're counting on you to negotiate.

Types of Coverage That Apply to Motorcycle Accident Claims

Knowing which coverage applies tells you where to file and what you can actually recover.

| Coverage Type | What It Pays For | Situations Where It Applies | Typical Monthly Premium |

| Liability | Other people's injuries and property damage you cause | When you're found at fault | State-required; usually $25-75/month for minimum limits |

| Collision | Repairs to your own motorcycle no matter who caused the crash | Any collision with another vehicle or stationary object | Runs $15-40/month based on your bike's value |

| Comprehensive | Non-crash damage like theft, vandalism, hail, hitting a deer | When covered perils damage or destroy your bike | Generally $10-25/month |

| Uninsured/Underinsured Motorist | Your medical costs when the at-fault driver lacks sufficient coverage | Other driver has no insurance or inadequate policy limits | Typically $5-15/month |

| Medical Payments (MedPay) | Your medical expenses regardless of who caused the accident | Any covered accident | Usually $3-10/month for $5,000-$10,000 in coverage |

Too many riders carry just liability coverage because state law demands it. This leaves them completely exposed for damage to their own motorcycle and their own medical bills if they cause the accident or get hit by an uninsured driver. Collision coverage and uninsured motorist protection fill these dangerous gaps.

Common Mistakes That Delay or Reduce Your Settlement

Even riders who handle the accident scene perfectly often sabotage their claims during negotiations.

Giving Recorded Statements Without Preparation

Claims adjusters receive training in asking questions that sound helpful but actually undermine your claim. "How are you feeling today?" seems like basic concern, but responding "doing pretty well" gets used as evidence you're not seriously injured. "Walk me through exactly how the accident occurred" encourages you to speculate beyond what you actually know or to contradict statements you made earlier.

Before recording any statement, review every piece of documentation, read the police report thoroughly, and consult your timeline. Stick exclusively to facts you're absolutely certain about. Saying "I don't remember that detail" or "I'd need to check my records" are perfectly acceptable responses. Guessing fills gaps in their favor, never yours.

Consider having an attorney coach you beforehand or participate in the call. You can't un-say words once they're recorded.

Accepting the First Offer

Insurance companies maximize profits by minimizing payouts. First offers typically cover only the most obvious expenses—your initial emergency room visit and clear vehicle damage. They exclude ongoing medical treatment, your motorcycle's diminished resale value, pain and suffering, and future lost wages.

The biggest mistake riders make is accepting the first settlement offer out of financial desperation. Insurance companies know many riders can't afford to be without their bike or miss work, so they make quick, low offers counting on riders to accept just to move on. In my experience, initial offers average 40-60% of what we ultimately recover after negotiation

— Marcus Chen

Respond to lowball offers with a comprehensive demand letter detailing every category of damages, backed up by documentation. Most cases settle somewhere between the second and fourth round of negotiations.

Posting on Social Media During Your Claim

Insurance companies routinely monitor claimants' social media profiles. A single photo of you standing upright at a family barbecue becomes "evidence" you're exaggerating your injuries, even if you were in agony the entire time. A post mentioning a weekend camping trip gets twisted into proof you're not suffering lost quality of life.

Switch all your social media accounts to private immediately. Decline friend requests from profiles you don't recognize—some are fake accounts created by investigators. Better yet, go completely dark on social media until your settlement check clears. Tell your friends and family not to tag you in any photos or posts.

How Insurance Companies Calculate Motorcycle Accident Payouts

Settlement amounts swing wildly based on several interconnected factors. Understanding their valuation methods helps you negotiate more effectively.

| Factor | Calculation Method | Effect on Your Settlement | Real-World Example |

| Injury Severity | Total medical costs multiplied by 1.5 to 5 depending on injury permanence | Huge impact; permanent disabilities get the highest multipliers | $20,000 in medical expenses × 3 multiplier = $60,000 for pain and suffering |

| Property Damage | Actual repair costs or fair market value if totaled | Direct dollar-for-dollar reimbursement | $8,500 in repairs; declared total loss if repair costs exceed 75% of bike's value |

| Liability Percentage | Comparative negligence reduces your payout by your percentage of fault | Major impact when fault is disputed | Being 20% at fault cuts your total settlement by 20% |

| Policy Limits | Cannot recover more than the at-fault party's coverage limits | Hard ceiling on maximum recovery | $25,000 policy cap even when your damages total $50,000 |

| Lost Wages | Documented past and projected future income loss | Moderate to significant impact | $800 per week × 6 weeks missed work = $4,800 |

The pain and suffering multiplier depends heavily on how well you've documented injuries, how long treatment lasted, and whether your injuries are "hard" (broken bones requiring surgery) versus "soft" (sprains and strains). Permanent conditions like scarring, reduced range of motion, or chronic pain justify the highest multipliers.

Adjusters also evaluate your credibility. Consistent medical treatment, following your doctor's orders exactly, and maintaining accurate records increases your settlement value. Treatment gaps, obviously exaggerated symptoms, or contradictory statements tank your credibility and your payout.

Author: Caleb Thornton;

Source: spy-delhi.com

Timeline: How Long Does a Motorcycle Insurance Claim Take?

Claim duration varies dramatically depending on complexity and how much the insurance company fights you.

Simple Claims vs. Complex Claims

Straightforward claims—minor injuries, obvious liability, property damage under $10,000—often wrap up within 30-60 days. You've completed medical treatment quickly, nobody disputes who caused the accident, and calculating the settlement value is relatively simple.

Complicated claims involving severe injuries, disputed fault, multiple vehicles, or coverage questions can drag on for 6-18 months or longer. If you need surgery, continuing treatment, or haven't reached maximum medical improvement (the point where doctors say you're as healed as you're going to get), you simply cannot settle. Settling early means you can't reopen the claim when complications emerge later.

Never accept a settlement before finishing all medical treatment. Signing that release form ends everything permanently.

What Causes Delays in Processing

Common bottlenecks include:

- Waiting for treatment to conclude: Can't calculate total damages until doctors confirm you've reached maximum medical improvement

- Liability fights: When each side blames the other, investigations drag on, sometimes requiring accident reconstruction experts

- Unresponsive parties: The other driver ignores their insurer's calls, witnesses have moved or won't return calls

- Coverage disputes: The insurer questions whether the policy was actually active or claims an exclusion applies

- Lowball negotiation tactics: Multiple back-and-forth rounds extend the timeline significantly

- Missing documentation: Incomplete records require follow-up requests that add weeks

You can accelerate the process by responding immediately to every request, maintaining organized files, and following up with your adjuster weekly. Document every single conversation with date, time, and brief summary notes.

When to Hire a Lawyer for Your Motorcycle Accident Claim

Plenty of motorcycle accident claims can be handled without hiring an attorney, but certain red flags mean you need professional representation.

Red Flags That You Need Legal Representation

Hire a lawyer when:

- Serious injuries occurred: Anything requiring hospital admission, surgical procedures, or causing permanent disability

- Liability is contested: The other driver or their insurance company claims you caused or contributed to the accident

- Multiple parties involved: Accidents with several vehicles create complicated liability and coverage issues

- Your claim gets denied: Denials require legal challenges and detailed policy interpretation

- Offers seem suspiciously low: Attorney involvement frequently doubles or triples initial settlement offers

- You're facing pressure to settle immediately: Aggressive settlement tactics usually mean they know your claim is worth substantially more

Attorneys handling motorcycle accidents typically work on contingency—they collect 33-40% of your final settlement and zero if you don't recover anything. That percentage might seem steep initially, but experienced attorneys usually recover significantly more than you'd get alone, even after deducting their fee.

How Attorney Involvement Changes the Process

Once you retain an attorney, all communication flows through them. This protects you from accidentally saying something damaging and signals to the insurance company that you're taking this seriously.

Attorneys craft demand letters that carry real weight, negotiate far more aggressively than most individuals can, and can file lawsuits if the insurance company refuses reasonable offers. Most cases still settle without ever reaching trial, but the credible threat of litigation motivates substantially better offers.

Your involvement becomes much simpler—focus on medical recovery while your attorney manages negotiations, documentation, and legal strategy.

Author: Caleb Thornton;

Source: spy-delhi.com

FAQ: Motorcycle Accident Insurance Claims

Protecting Your Rights and Maximizing Your Settlement

Successfully navigating a motorcycle accident insurance claim demands careful attention at every single stage. Riders who document thoroughly, understand exactly what their coverage includes and excludes, avoid the common pitfalls outlined here, and recognize when to bring in legal help consistently secure better outcomes than those who rush through the process or assume insurance companies will voluntarily offer fair settlements.

Start by capturing solid evidence at the accident scene and getting medical evaluation immediately, even when you feel fine. Follow the step-by-step filing process carefully, refusing to give recorded statements until you've prepared properly. Understand which specific coverage types apply to your unique situation and how adjusters actually calculate settlement values. Recognize that first offers rarely represent anywhere close to full value and that negotiation is not only expected but necessary.

Perhaps most importantly, don't let financial pressure force you into accepting inadequate compensation just to get it over with. Your motorcycle accident claim may represent your only opportunity to recover costs that could affect your finances and quality of life for years to come. Invest the time to build a comprehensive case, document every category of damages, and negotiate persistently for the settlement that actually reflects your losses.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer insights and guidance on motorcycle accident insurance claims, settlement processes, liability issues, coverage limits, medical compensation, and related insurance matters, and should not be considered legal or financial advice.

All information, articles, and materials presented on this website are for general informational purposes only. Insurance policies, liability standards, settlement practices, and state regulations may vary by jurisdiction and insurer. The outcome of a motorcycle accident claim depends on the specific facts of the accident, available evidence, policy language, and applicable law.

This website is not responsible for any errors or omissions in the content, or for actions taken based on the information provided. Users are strongly encouraged to consult with a qualified attorney or licensed insurance professional regarding their specific motorcycle accident claim before making decisions about settlements, negotiations, or coverage disputes.