Injured motorcycle rider sitting at kitchen table reviewing medical bills and financial documents with a bandaged arm and a motorcycle visible through the window

How to File a Motorcycle Accident Lost Wages Claim Successfully

A motorcycle wreck doesn't just leave you with injuries—it empties your bank account while you're stuck at home healing. You've got medical bills showing up in the mail daily, but here's the problem: your paychecks have stopped coming. Most riders I've talked to had no clue they could recover this lost income, and even fewer knew how to actually file for it.

Here's what insurance companies won't tell you upfront: saying "I missed three weeks of work" won't get you paid. Claims adjusters want paperwork—lots of it. They want calculations showing exact dollar amounts. They need your doctor to write specific statements about why you physically couldn't do your job. Skip any of these pieces and you'll get a denial letter or a lowball offer that covers maybe half what you actually lost.

I'm going to show you exactly how to document everything, calculate what you're owed, and submit a claim that actually gets approved. We'll cover what income counts (it's more than just your hourcheck), which documents matter most, and which mistakes cause riders to leave thousands of dollars on the table.

What Qualifies as Lost Wages After a Motorcycle Accident

Most riders think lost wages means their regular paycheck and nothing else. That's leaving money behind. You can recover nearly any income that would've hit your account if someone hadn't knocked you off your bike.

Types of Income Loss You Can Claim

Your base pay—whether hourly or salary—represents the obvious starting point. But what about that overtime you pull every week?

If you've consistently worked extra hours, that counts. Let's say you're in construction and you've logged 8-10 overtime hours weekly for the past five months. That's not "extra" income anymore—it's predictable money you count on for rent and groceries. Adjusters can't wave that away as speculative when your pay stubs prove the pattern.

Performance bonuses create arguments. Did you earn a $3,000 quarterly bonus every quarter for two years straight? That's compensable. Was there maybe possibly a bonus coming that you might have qualified for? That's tougher to prove. Get something in writing from your HR department or supervisor stating you were on track to receive it.

Commissions work similarly for sales jobs. An insurance adjuster won't accept your best month's commission (say, $12,000) and multiply that out. They'll average your last three to six months instead. Pulled in $8,000, $6,500, $9,200, $7,800, $10,100, and $8,900 over six months? That's roughly $8,400 monthly—use that figure.

Benefits have actual dollar values attached. When your employer kept paying their share of your health insurance premiums while you were out, that's real money. Same goes for 401(k) matches you missed, profit-sharing contributions that would've landed in your account, or stock options you couldn't exercise.

Did you burn through two weeks of PTO covering your injury? Those days have monetary worth. You earned that time off—it's compensation you received and then had to spend because someone ran a red light. Calculate what those hours pay out at your normal rate.

Author: Hannah Pierce;

Source: spy-delhi.com

Self-Employed vs. W-2 Employee Claims

Employees with W-2s have it easier. Your employer exists as a neutral third party who'll confirm dates, pay rates, and schedules. Grab a couple recent pay stubs, get a letter on company letterhead, pull your tax return if needed, and you've got a complete picture.

Self-employed riders face skepticism from the jump. There's no boss to vouch for you. Insurance adjusters assume you're inflating numbers because, honestly, some people do.

You'll need tax returns—specifically the last two years showing Schedule C. That schedule breaks down profit from your business operations. Adjusters typically average both years to smooth out the ups and downs that come with running your own operation.

Client contracts become your lifeline. If you're a freelance photographer and you had five weddings booked during your recovery period at $3,500 each, those signed contracts prove you would've earned $17,500. No contracts? You're asking the adjuster to trust your word about what "probably" would've happened, and they won't.

Bank deposits help fill gaps. Pull six months of statements showing regular income deposits. Rideshare and delivery drivers should download their platform reports—Uber, DoorDash, Instacart all provide weekly earnings summaries you can print.

One critical detail: separate your gross revenue from actual income. If you're a contractor who typically spends 35% on materials and subs, you can't claim the full contract value. Net profit matters here, not the top-line number.

Documentation Required to Prove Your Lost Income

Insurance companies reject more claims for missing paperwork than for actual policy disputes. Build your documentation package correctly the first time and you'll avoid months of back-and-forth requests.

Essential Records from Your Employer

Call HR or your supervisor and request a letter printed on company letterhead. That letter needs these specifics: your job title, when you started, your normal schedule (including which days and how many hours), and exactly how you're paid.

For hourly workers, the letter should state your rate—"$32.50/hour working 40 hours weekly." Salaried employees need their annual figure—"$67,000 annual salary paid biweekly." If overtime, bonuses, or commissions are part of your regular compensation, those need to be spelled out too.

Make sure your supervisor's direct contact information appears on the letter. Some adjusters will call to verify details, and having a live person confirm everything speeds up the process dramatically.

You also need attendance records showing exactly which dates you were out and why. Some employers use specific injury leave codes different from vacation or personal days. That distinction matters—it proves your absence resulted from the accident, not a planned trip to the beach.

Were you scheduled for anything special during your recovery? A promotion that got delayed? A temporary supervisor role that paid an extra $5/hour? Major project overtime everyone in your department was pulling? Get those lost opportunities documented in writing while people still remember them.

Tax Returns and Pay Stubs You'll Need

Pull your last two or three months of pay stubs before the crash. These show your actual take-home pattern, not what you're "supposed" to make according to your offer letter from three years ago.

Tax returns verify that you actually earned what you claim. If you say you make $85,000 but your W-2 shows $62,000, guess which number the adjuster will use? For longer claims extending beyond a month, expect to provide last year's complete return.

Self-employed folks, you need two years minimum. Include every schedule—especially Schedule C where business income lives and Schedule SE showing self-employment tax. If your income jumped around significantly (maybe $45,000 one year and $78,000 the next), write a brief explanation for why and which figure better represents your current earning power.

Here's something that trips people up: if you paid quarterly estimated taxes, save those receipts. They corroborate your income level. Someone paying estimated taxes on $70,000 income but claiming they make $95,000 creates questions you don't want to answer.

Author: Hannah Pierce;

Source: spy-delhi.com

Medical Documentation Linking Injury to Missed Work

A doctor's note saying "patient injured" accomplishes nothing for your claim. You need explicit statements from your physician explaining why your injuries physically prevented you from performing your specific job duties during specific dates.

Work restrictions carry more weight than diagnosis names. A broken finger might not stop an accountant from working but completely prevents a massage therapist from doing their job. Your doctor should write restrictions like "no gripping or fine motor work with right hand," "limited to 20 minutes standing per hour," or "no overhead reaching"—then explain how these limitations make your particular job impossible.

When your doctor clears you to return, get that in writing even if it's just for light duty. This document creates a clear endpoint showing exactly when your earning capacity was impaired and when it came back.

Keep every physical therapy note, specialist report, and surgical record. An adjuster might push back on six weeks off work for what looks like a "moderate" injury on paper, but surgery records and twice-weekly PT notes showing ongoing mobility work make that timeline completely reasonable.

Step-by-Step Process for Filing Your Wage Loss Claim

How you file depends on which insurance you're claiming against—your own policy's PIP coverage, the at-fault driver's liability policy, or your uninsured motorist protection—but the basic steps stay consistent.

Notifying Your Insurance Company Within Required Timeframes

Nearly every policy requires "prompt" notice of accidents. In practice, that usually means 24 to 72 hours maximum. Even if you're in the hospital, have a family member or friend call your insurer to report the crash. Waiting too long can blow up your entire claim before you even get to lost wages.

Lost wage claims often have separate deadlines beyond the initial accident report. Many policies say you've got 30 days from when the loss occurs—not 30 days from the accident date. If you were off work during weeks two through four after the crash, that 30-day clock started ticking from your first missed shift.

Dig out your policy and read the notice section word-for-word. Some companies accept phone calls; others want written notification. Document absolutely everything—if you call, send an email right after summarizing the conversation and confirming what the rep told you.

Submitting Your Claim Package

Don't just dump a folder of random papers on the adjuster's desk (literally or figuratively). Organize everything logically with a cover letter up front that summarizes the key facts: accident date, injury type, total days you couldn't work, and the total dollar amount you're claiming.

Attach supporting documents in order: medical records first, then employer letter, pay stubs, tax returns if needed.

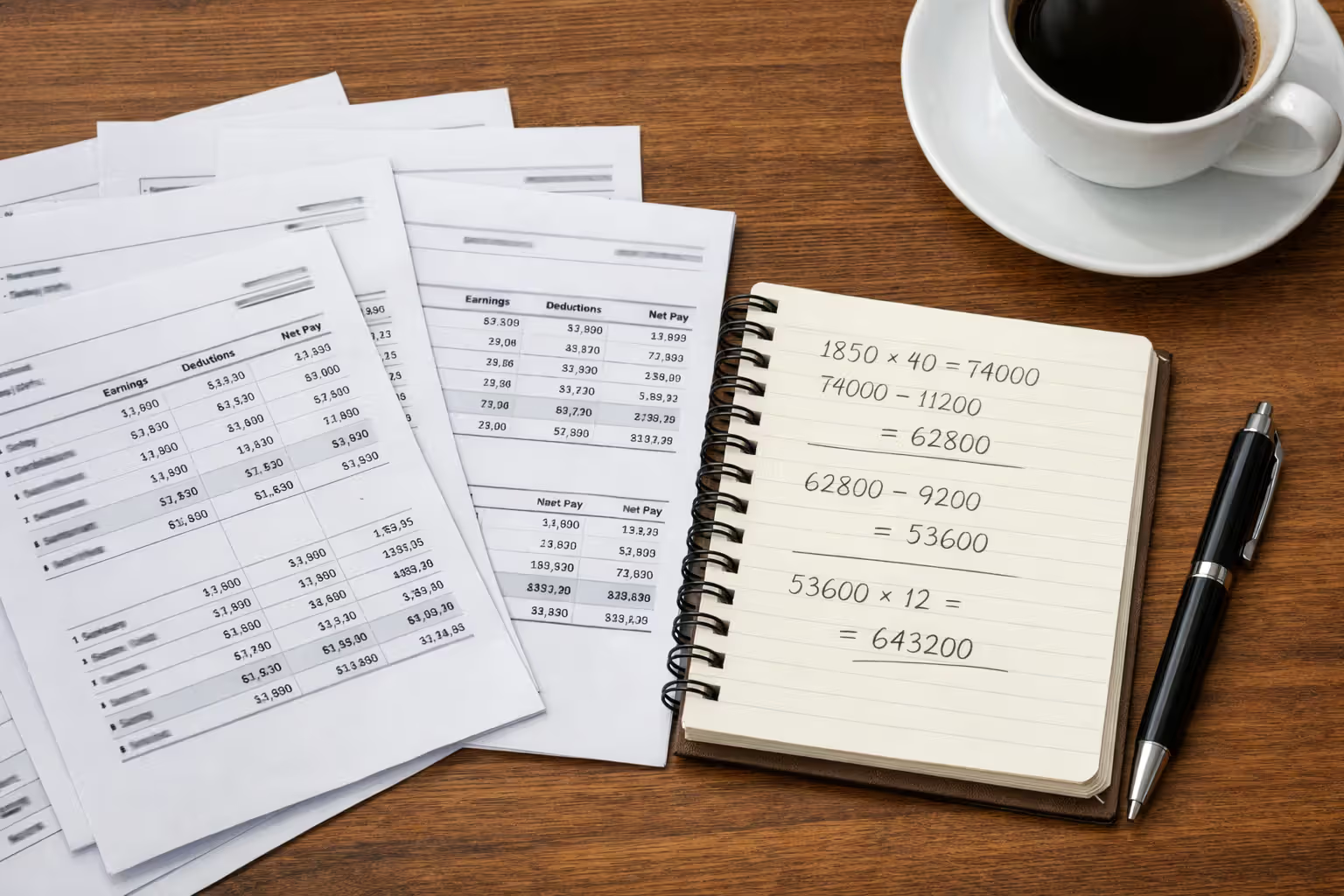

Calculate your lost wages yourself and show your math clearly. Don't make the adjuster guess at your methodology or do arithmetic. Write it out: "Standard hourly rate $28.50 × 40 hours per week × 4 weeks missed = $4,560 in base wages. Typical overtime of 8 hours weekly × $42.75 per hour × 4 weeks = $1,368 in overtime wages. Combined total: $5,928 in lost income."

For self-employed claims, break down your typical monthly income, list the specific contracts or projects you couldn't fulfill, and note any extra costs you took on (like paying someone to cover essential business tasks) to prevent even bigger losses.

Submit everything the insurer wants in one complete package whenever possible. Sending stuff piecemeal drags out processing and increases the chances documents get lost in the file.

Author: Hannah Pierce;

Source: spy-delhi.com

What Happens During the Review Period

Plan on 30 to 45 days for initial review on straightforward claims, longer if anything's complicated. The adjuster checks your documentation, might call your employer directly to verify details, and applies your policy terms to figure out what's covered.

Some adjusters prefer phone calls over written requests when they have questions. Take detailed notes during these conversations—who called, what date and time, specific questions they asked. Follow up with an email confirming what you understood they needed and when you'll provide it.

Partial approvals happen all the time. An insurer might approve two weeks of lost wages but balk at the third week because medical notes from a follow-up appointment mentioned "increased range of motion." Be ready to provide additional documentation explaining why improvement doesn't equal ability to work yet.

Denials should include specific reasoning. "Insufficient documentation" tells you exactly what to fix—provide more paperwork. "Injury not severe enough to prevent work" means they're disputing medical necessity, which is when you should probably talk to a lawyer.

How Insurance Companies Calculate Motorcycle Accident Wage Reimbursement

Understanding how adjusters run the numbers helps you spot errors in settlement offers before you accept payment and close your claim forever.

Standard Calculation Methods for Hourly and Salaried Workers

Hourly employees see simple math: hourly rate times missed hours. Things get messier when your schedule varies. If you work anywhere from 35 to 45 hours depending on business needs, the adjuster will probably average your hours over the previous 8 to 12 weeks instead of using your busiest weeks.

Overtime calculations multiply your overtime rate (usually 1.5x your regular rate) by your average overtime hours. You've got to demonstrate a pattern—one random week of heavy overtime doesn't establish that income as expected. Most adjusters want at least two or three months of steady overtime before they'll include it.

Salaried workers see their annual salary divided by 52 weeks, then divided by 5 days to get a daily rate. If you're paid biweekly or monthly, adjusters calculate weekly income by multiplying your per-period amount by how many pay periods you get yearly (26 for biweekly, 12 for monthly) then dividing by 52 weeks.

Part-timers get more scrutiny. When your schedule bounces around—maybe 25 hours one week and 12 the next—expect the insurer to use conservative averages. A college student working inconsistent hours shouldn't build their claim around their busiest weeks.

Commission-based pay gets averaged across three to six months typically. That real estate agent who closed three big deals the month before the accident but averaged one deal monthly over the past year? Calculation will probably use the longer average, not the recent hot streak.

Proving Lost Future Earning Capacity

Permanent or long-lasting injuries that damage your ability to earn income in the future require completely different analysis than temporary lost wages. These claims need vocational expert testimony and detailed medical prognosis about permanent limitations.

Reduced earning capacity applies when you return to work but can't perform at your previous level. Think about a motorcycle mechanic with permanent hand mobility problems—they might get back to the shop but can't handle certain repairs anymore, which cuts their efficiency and income. Calculating this loss means comparing what you could earn before versus what you can earn now.

Career impact matters enormously for serious injuries. A 35-year-old commercial driver whose injuries cost them their CDL hasn't just lost current wages—they've lost decades of earning potential in the profession they trained for. These claims regularly hit six or seven figures and almost always need attorney involvement.

Vocational rehabilitation experts assess what work you can still do post-injury and what retraining you might need. If you earned $75,000 yearly as a roofer but your injuries limit you to desk work paying $40,000, that $35,000 annual gap multiplied across your remaining work years represents lost earning capacity.

Author: Hannah Pierce;

Source: spy-delhi.com

Common Mistakes That Reduce Your Lost Wage Recovery

Waiting weeks or months to file. People forget details, you'll misplace documents, witnesses become unreachable. File your claim as soon as you've gathered the necessary paperwork, even if you're still recovering. You can file supplemental claims if your recovery drags on longer than expected.

Forgetting to document side income. That weekend landscaping gig or occasional freelance consulting? That's lost income too—but only if you reported it to the IRS. Cash income you never claimed creates tax headaches and won't be compensated by insurance.

Going back to work before medical clearance. Financial pressure pushes many riders back to work before doctors clear them. This risks reinjury and hands insurance companies evidence that you weren't really unable to work. If you returned after one week but claim you needed two weeks, expect hard questions.

Accepting the first settlement number without checking it yourself. Run your own calculation before reviewing what the insurer offers. Adjusters make mistakes—sometimes in your favor but usually not. One rider I know caught an adjuster who calculated their claim using 40-hour weeks when pay stubs clearly showed 50-hour weeks. That's a 25% error.

Confusing workers' comp with regular accident claims. If your crash happened during work-related travel, workers' compensation might be your remedy, not the auto insurance claim. Filing through the wrong system causes massive delays and can cost you rights in the correct system.

Forgetting about benefits you used up. That week of PTO you burned covering your absence? It has dollar value—typically your daily rate times days used. The health insurance premiums your employer kept paying while you were on unpaid leave? Those represent additional losses.

Lousy record-keeping after you file. Save copies of everything you submit and take detailed notes about every single conversation with adjusters. When disputes pop up months later, your contemporaneous records become your best evidence.

When to Hire a Lawyer for Your Motorcycle Injury Wage Claim

Most simple lost wage claims don't justify hiring an attorney—legal fees would eat up more than you'd gain for a straightforward two-week claim with solid documentation. Certain situations flip that calculation completely.

Red Flags That Your Claim Needs Legal Representation

Disputed fault complicates everything immediately. When the insurance company argues you caused or contributed to the accident, they'll slash or deny your entire claim including lost wages. Comparative negligence rules change by state, but even 20% fault can cut your recovery by one-fifth. Attorneys know how to investigate crashes, collect evidence, and build cases proving the other driver's responsibility.

Serious injuries with long-term consequences need legal expertise you don't have. Calculating lost earning capacity across decades, accounting for promotion potential you'll never reach, and projecting wage growth require economic experts that attorneys work with regularly but individuals can't efficiently hire on their own.

When your claim gets denied, legal review becomes valuable. Insurance companies deny claims for all kinds of reasons—some legitimate, plenty pretextual. An attorney can tell you whether the denial holds water or represents the insurer trying to dodge a valid claim. Lots of denials get reversed on appeal with proper legal pressure.

Bad faith practices—unreasonable delays, ridiculous lowball offers despite clear documentation, refusal to properly investigate—justify legal action beyond just recovering your lost wages. Lawyers can pursue additional damages when insurers violate their duty to deal fairly with you.

Multiple potentially liable parties create complexity requiring legal coordination. If your crash involved several vehicles, or maybe a road defect contributed, identifying every potential source of compensation and filing appropriate claims against each requires legal knowledge most riders don't possess.

Self-employed individuals with substantial income often benefit from legal help even on relatively straightforward cases. Proving business income to a skeptical adjuster's satisfaction requires presentation skills and documentation strategies attorneys have refined through hundreds of claims.

How Attorney Fees Work in Lost Income Cases

Personal injury lawyers typically work on contingency—they take a percentage of your recovery, usually somewhere between 33% and 40%, and collect nothing if they don't win compensation. This setup lets injured riders access legal help without paying anything upfront.

Contingency percentages often bump up if the case moves to litigation. An attorney might charge 33% for a negotiated settlement before filing suit but 40% if they have to file a lawsuit and go through discovery. Some attorneys use a flat 40% regardless of case stage.

Costs are separate from fees. Even contingency attorneys usually deduct case expenses—filing fees, expert witness bills, medical record retrieval costs—from your settlement before calculating their percentage. A $50,000 settlement with $3,000 in costs and a 33% contingency fee nets you: $50,000 minus $3,000 equals $47,000, times 67% equals $31,490 in your pocket.

Ask potential attorneys whether costs come "off the top" (subtracted before calculating fee percentage) or "off the bottom" (subtracted after). This significantly impacts your net recovery.

Some attorneys front all costs during the case and recoup them from the settlement. Others require clients to pay costs as they're incurred even though the attorney's fee remains contingent. Nail down this arrangement before signing anything.

The biggest mistake I see riders make? Incomplete documentation of their earning patterns. Insurance adjusters aren't sitting there trying to figure out what you probably earned—they're hunting for reasons to pay the absolute minimum they can defend. When riders bring me three months of pay stubs instead of one, document their regular overtime, and secure detailed employer letters, their settlements jump by 30-40% on average compared to bare-bones claims

— Michael Chen

Comparison of Lost Wage Documentation by Employment Type

| Employment Type | Required Documents | Processing Difficulty | Average Claim Time |

| W-2 Employee | Employer verification letter, 2-3 recent pay stubs, tax return if claim exceeds one month | Low | 3-5 weeks |

| Self-Employed/1099 | Two years' tax returns including Schedule C, bank statements, client contracts, profit/loss statements | High | 6-10 weeks |

| Commission-Based | Employer letter explaining commission structure, 6 months' pay stubs, tax return, sales records | Medium-High | 5-8 weeks |

| Part-Time Worker | Employer letter showing typical schedule, 3 months' pay stubs, work schedule for period missed | Medium | 4-6 weeks |

| Gig Economy Worker | Platform earnings reports covering 3-6 months, tax return including Schedule C, bank deposit records | Medium-High | 5-9 weeks |

Frequently Asked Questions About Motorcycle Accident Lost Wages

Moving Forward with Your Claim

Recovering lost wages after a motorcycle crash requires detailed attention that feels overwhelming when you're already dealing with injuries and medical appointments. The effort pays off substantially—riders who thoroughly document their losses and understand the claims process recover significantly more than those who submit minimal claims hoping the insurance company will give them the benefit of the doubt.

Start gathering documentation immediately, even if you're still recovering and unsure how much work you'll ultimately miss. Requesting employer letters and pulling pay stubs now prevents panicked scrambling later when the insurance company sets a documentation deadline. Calculate your losses explicitly rather than leaving the math to the adjuster, and maintain detailed records of every submission and conversation throughout the entire process.

Recognize when your claim crosses from straightforward to complex. A two-week absence with clear documentation rarely justifies attorney fees, but serious injuries, disputed fault, or substantial self-employment income often do. Most personal injury attorneys offer free consultations, so getting a professional assessment costs nothing and might reveal complications or recovery opportunities you hadn't considered.

Your lost wage claim represents actual money you would have earned if someone else hadn't been negligent. Approach the process with the same seriousness you'd apply to any other significant financial matter, and don't settle for less than full compensation for income you've lost through absolutely no fault of your own.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer insights and guidance on motorcycle accident insurance claims, settlement processes, liability issues, coverage limits, medical compensation, and related insurance matters, and should not be considered legal or financial advice.

All information, articles, and materials presented on this website are for general informational purposes only. Insurance policies, liability standards, settlement practices, and state regulations may vary by jurisdiction and insurer. The outcome of a motorcycle accident claim depends on the specific facts of the accident, available evidence, policy language, and applicable law.

This website is not responsible for any errors or omissions in the content, or for actions taken based on the information provided. Users are strongly encouraged to consult with a qualified attorney or licensed insurance professional regarding their specific motorcycle accident claim before making decisions about settlements, negotiations, or coverage disputes.