Damaged motorcycle lying on asphalt road next to scattered insurance documents and denial letter envelope at urban intersection

How to Fight a Motorcycle Accident Claim Denial From Your Insurer

Getting hit with a motorcycle accident claim denial after suffering injuries, bike damage, and mounting medical bills feels like a second collision. You paid premiums expecting protection, yet your insurer sends a letter refusing coverage. The shock quickly turns to frustration, then panic about how you'll cover expenses that can easily reach tens of thousands of dollars.

Insurance companies deny motorcycle claims at higher rates than car accident claims—sometimes citing reasons that seem arbitrary or contradictory to what your policy appears to promise. Understanding why denials happen, how to dissect the insurer's reasoning, and what steps to take next can mean the difference between absorbing devastating costs yourself and recovering the compensation you deserve.

Why Insurance Companies Deny Motorcycle Accident Claims

Insurers reject motorcycle claims for three primary categories of reasons, though the stated justification doesn't always reflect the real motivation. Recognizing these patterns helps you anticipate weak spots in your claim and address them proactively.

The insurance company is not your friend. Their job is to collect premiums and deny claims

— John Grisham

Policy Exclusions and Coverage Gaps

Most motorcycle policies contain exclusions that void coverage under specific circumstances. Racing or participating in timed speed events triggers automatic denial in virtually every policy. Using your bike for commercial purposes—food delivery, courier services, ride-sharing—without purchasing commercial coverage creates another common gap.

Some policies exclude coverage if the motorcycle has been modified beyond certain parameters. A bike with aftermarket exhaust, suspension changes, or engine modifications might fall outside your policy terms if you didn't disclose these alterations when purchasing coverage. Insurers sometimes discover modifications only after an accident, then cite the undisclosed changes as grounds for denial.

Geographic restrictions also appear in certain policies. If your policy covers your bike in your home state but you crashed during a cross-country trip, some insurers attempt to deny claims based on out-of-area exclusions. These geographic clauses vary widely and require careful policy review.

Documentation and Reporting Failures

Late reporting ranks among the most frequent denied motorcycle insurance claim reasons. Most policies require notification within a specific timeframe—often 24 to 72 hours after an accident. Miss that window, even by hours, and insurers may deny the entire claim. They argue that delayed reporting prevents proper investigation and suggests the accident might not have occurred as described.

Insufficient documentation creates another vulnerability. If you left the accident scene without calling police, didn't exchange information with other parties, or failed to photograph damage immediately, the insurer lacks third-party verification of your account. They may cite this absence of corroborating evidence as justification for motorcycle claim rejection insurance decisions.

Medical treatment gaps also trigger denials. If you waited several days before seeing a doctor, or if you missed follow-up appointments, insurers argue your injuries weren't serious or weren't caused by the accident. They scrutinize medical records for any suggestion that symptoms developed later or resulted from pre-existing conditions.

Author: Hannah Pierce;

Source: spy-delhi.com

Disputed Liability and Fault Determination

Insurers frequently deny claims by asserting you caused the accident or contributed substantially to it. Even in states with comparative negligence laws, insurers may deny claims entirely and force you to prove their liability determination was incorrect.

They'll cite witness statements that contradict your version of events, or they'll hire accident reconstruction experts who conclude you were speeding, failed to yield, or violated traffic laws. Sometimes these determinations rest on questionable evidence—skid marks that could have multiple interpretations, damage patterns that don't definitively prove fault, or witness accounts from people who didn't actually see the collision moment.

Alcohol or drug allegations represent another category. If police administered field sobriety tests or requested chemical testing, insurers scrutinize those results intensely. Even if you weren't charged or if test results were below legal limits, insurers sometimes argue that any detectable amount contributed to the accident and justifies denial.

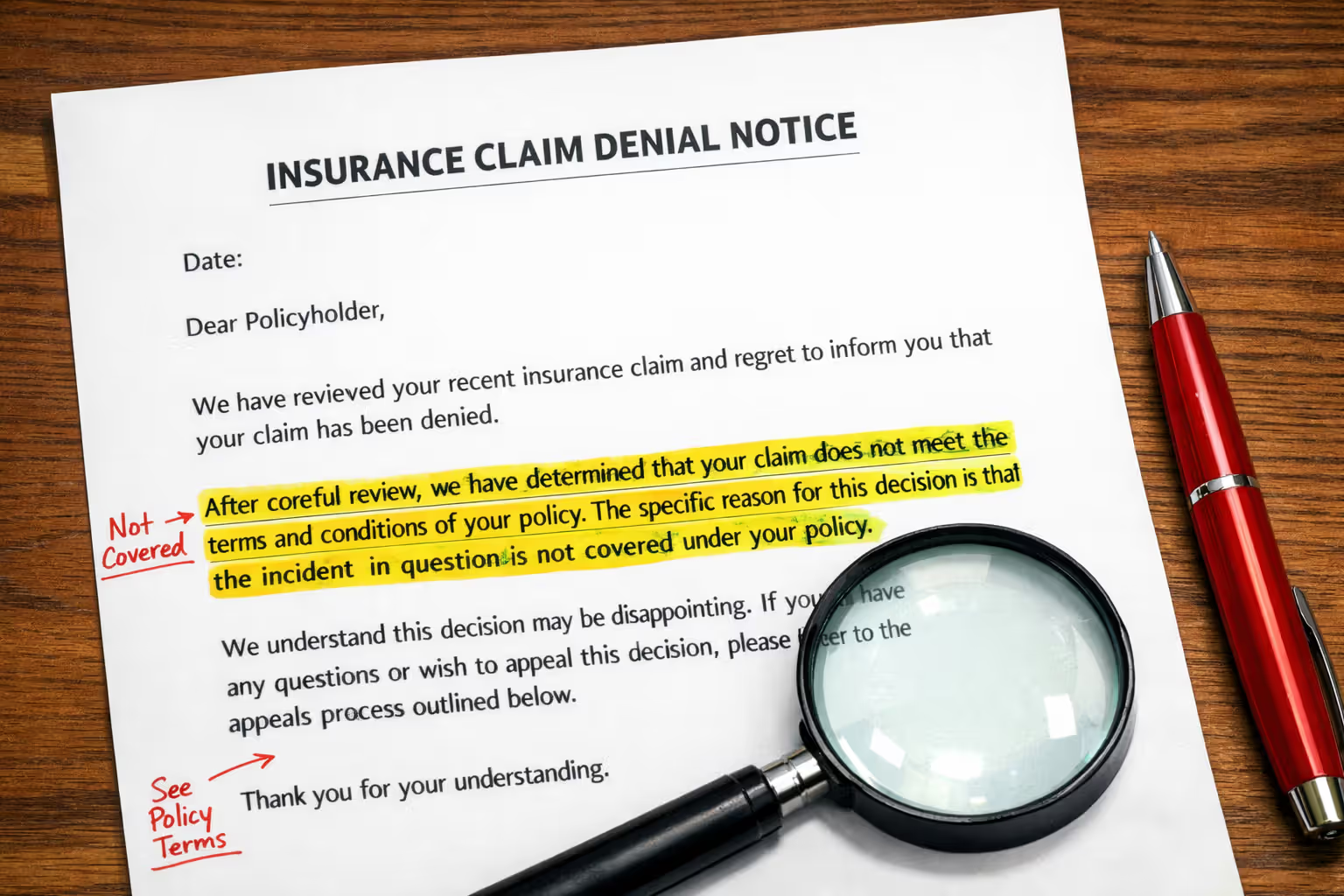

How to Read Your Denial Letter and Identify the Real Problem

Your denial letter contains crucial information buried in insurance jargon and legal citations. Learning to decode this document reveals whether the insurer has legitimate grounds or is relying on technicalities you can challenge.

Look for the specific policy section cited as grounds for denial. The letter must reference exact policy language—page numbers, section headings, and quoted provisions. Generic statements like "your claim doesn't meet policy requirements" without specific citations suggest the insurer is fishing for justification rather than applying clear policy terms.

Author: Hannah Pierce;

Source: spy-delhi.com

Compare the cited policy language to what actually happened. If the insurer claims you violated a reporting requirement, check the exact timeline. Did you report within the stated timeframe when accounting for weekends, holidays, or time zone differences? If they cite an exclusion for racing, does your accident genuinely fit that description, or were you simply riding on a public road?

Watch for conditional language that reveals weak reasoning. Phrases like "appears to," "may indicate," or "suggests that" signal the insurer doesn't have definitive evidence. Strong denials use declarative language: "You violated the policy by..." rather than "It appears you may have violated..."

Check whether the denial addresses all aspects of your claim. If you filed for both collision damage and medical payments, the letter should explain the decision on each coverage type separately. A blanket denial without distinguishing between different coverages may indicate the insurer hasn't thoroughly evaluated your claim.

Note the appeal deadline prominently stated in the letter. This date is non-negotiable. Missing it can forfeit your right to challenge the denial through the insurer's internal process, forcing you into more expensive and time-consuming litigation.

Building Your Case: Evidence You Need Before Filing an Appeal

Successful appeals rest on documentation that directly contradicts the insurer's stated denial reason. Gathering comprehensive evidence before initiating the appeal motorcycle claim denial process prevents delays and strengthens your position.

Start with the police report, which carries significant weight as a neutral third-party account. If the report assigns fault to the other driver or documents road conditions, vehicle positions, or witness statements supporting your version, it undermines insurer arguments that you caused the accident. If no police report exists, consider whether you can still obtain one—some jurisdictions allow delayed reporting for non-injury accidents.

Medical records must establish a clear causal link between the accident and your injuries. Obtain complete records from your first treatment through current care. Pay particular attention to initial intake notes where you described how injuries occurred. Consistent descriptions across multiple medical providers strengthen your case. If any provider's notes suggest injuries might have pre-existed the accident, get a clarifying letter from that provider explaining why the accident caused or aggravated the condition.

Photographic evidence of vehicle damage, road conditions, and injuries provides visual proof that often contradicts insurer claims. Take new photos if you still have access to the damaged motorcycle—different angles or close-ups of specific damage might reveal details you didn't capture initially. If the bike has been repaired or totaled, obtain photos from the repair shop or salvage yard.

Witness statements from people who saw the accident carry substantial weight, especially if they're disinterested third parties rather than friends or family. If you didn't get contact information at the scene, consider returning to the location to ask nearby businesses whether employees might have witnessed the accident. Check whether any businesses have exterior security cameras that captured footage.

Expert opinions can counter the insurer's technical arguments. An accident reconstruction expert can analyze physical evidence and provide an alternative explanation of how the collision occurred. A motorcycle mechanic can document that modifications to your bike were minor and didn't contribute to the accident. Medical experts can explain how your injury pattern is consistent with the accident forces you described.

Preserve all communications with the insurance company. Save emails, record call dates and the names of representatives you spoke with, and keep copies of every document you submitted. Insurers sometimes claim they never received documents or that you failed to respond to requests. Your records prove otherwise.

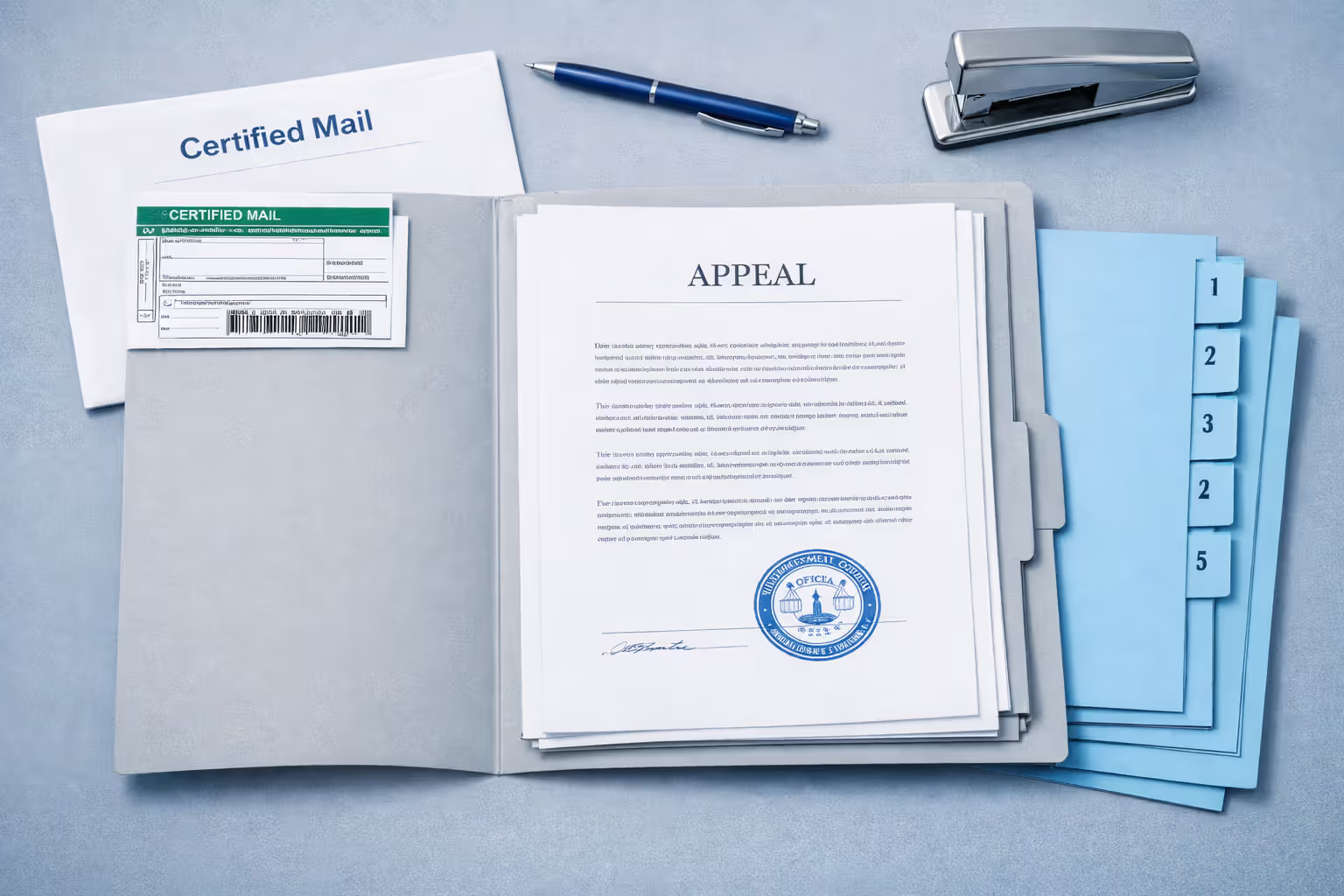

The Motorcycle Claim Appeal Process: Step-by-Step Timeline

The motorcycle claim appeal process typically follows a structured sequence with specific timeframes at each stage. Understanding this timeline helps you plan strategically and avoid missing critical deadlines.

Within days of receiving your denial, request your complete claim file from the insurer. Most states require insurers to provide this within 15 to 30 days. The file contains adjuster notes, recorded statements, expert reports, and other materials the insurer relied on when denying your claim. This information reveals the insurer's reasoning and identifies weaknesses you can exploit.

Prepare your appeal submission during the 30 to 60 days you typically have to file. Write a detailed appeal letter that addresses each stated reason for denial point by point. Attach supporting documentation organized with tabs or labels so the reviewer can easily find specific evidence. Submit via certified mail with return receipt to prove delivery and timing.

Author: Hannah Pierce;

Source: spy-delhi.com

Internal Appeals vs. External Reviews

Internal appeals go to a different claims examiner or supervisor within the same insurance company. This reviewer theoretically applies fresh eyes to your claim, though they work for the company that profits from denying it. Internal appeals usually take 30 to 60 days for a decision.

If the internal appeal fails, external review options vary by state. Some states require insurers to participate in independent review organizations that provide binding decisions. These external reviewers are theoretically neutral and can overturn the insurer's denial. The external review process typically takes 45 to 60 days.

Other states don't mandate external review but allow it as an option. If your state offers this and your claim value justifies it, external review costs typically range from $500 to $1,500—expensive, but potentially worthwhile for claims worth tens of thousands.

State Department of Insurance Complaints

Filing a complaint with your state's Department of Insurance (DOI) runs parallel to the appeal process. The DOI can't force the insurer to pay your claim, but it can investigate whether the insurer violated state regulations in how it handled your claim.

DOI complaints work best when the insurer violated procedural requirements—failed to investigate properly, missed response deadlines, or didn't cite specific policy language in the denial. If the DOI finds violations, insurers often settle claims to avoid formal sanctions.

File your DOI complaint within weeks of the denial. Include copies of all relevant documents and a clear explanation of why you believe the denial was improper. The DOI typically contacts the insurer within 10 to 15 days and requires a response within 30 days. The entire process usually concludes within 60 to 90 days.

When Hiring a Lawyer Makes Financial Sense for Your Denied Claim

Attorney involvement changes the dynamics of your motorcycle insurance claim dispute, but it comes with costs that must be weighed against potential recovery.

Most personal injury attorneys handling denied insurance claims work on contingency—they take 33% to 40% of any recovery. For a claim worth $50,000, you'd pay $16,500 to $20,000 in attorney fees if successful. That seems steep, but consider whether you're likely to recover anything without legal help. If the insurer is stonewalling and your own appeal efforts have failed, 60% of something beats 100% of nothing.

Claim value matters significantly. For claims under $10,000, attorney fees may consume so much of the recovery that hiring one doesn't make sense unless you can't handle the appeal yourself. For claims worth $25,000 or more, attorney involvement often pays for itself through increased settlement offers and higher success rates.

Time pressure from statutes of limitations makes attorney involvement more urgent. Most states impose a deadline—typically two to four years from the accident date—for filing lawsuits against insurers. If your internal appeals and DOI complaint have consumed months and you're approaching this deadline, an attorney can file suit to preserve your rights while continuing settlement negotiations.

Attorneys add value beyond just filing paperwork. They understand which arguments resonate with insurers, how to depose claims adjusters effectively, and when settlement offers are genuinely fair versus lowball attempts. They also signal to the insurer that you're serious about pursuing the claim, which often prompts better settlement offers.

Bad faith claims represent another consideration. If your insurer denied your claim unreasonably or failed to investigate properly, you might have grounds to sue for bad faith—seeking not just the policy limits but also punitive damages and attorney fees. Bad faith claims are complex and nearly impossible to pursue without an attorney, but they can dramatically increase your recovery when the insurer's conduct was egregious.

Common Mistakes That Weaken Your Motorcycle Insurance Claim Dispute

Certain missteps during the denial and appeal process undermine even strong claims. Avoiding these errors preserves your leverage and credibility.

Admitting any fault, even partial, gives insurers ammunition to deny or reduce your claim. Statements like "I might have been going a little fast" or "I didn't see him until the last second" become permanent record. Insurers interpret any ambiguity as admission of liability. Stick to factual descriptions without speculation about what you should have done differently.

Author: Hannah Pierce;

Source: spy-delhi.com

Missing deadlines kills claims that would otherwise succeed. The appeal deadline in your denial letter is absolute. The statute of limitations for filing suit is absolute. Calendar these dates immediately and set reminders weeks in advance. If you're approaching a deadline and haven't completed your appeal preparation, submit what you have and supplement it later rather than missing the deadline entirely.

Accepting lowball settlement offers out of desperation is common when medical bills pile up. Insurers count on financial pressure to force quick settlements for far less than claims are worth. Once you accept a settlement and sign a release, you can't reopen the claim later when you discover the settlement didn't cover your expenses. If you need immediate funds, consider personal loans or payment plans with medical providers rather than settling prematurely.

Poor communication with adjusters creates unnecessary problems. Failing to return calls, providing inconsistent information, or becoming hostile makes adjusters less inclined to work with you. You can be firm and persistent without being combative. Document all communications but maintain a professional tone even when frustrated.

Posting on social media about your accident or injuries hands insurers evidence to use against you. Photos of you engaging in physical activities contradict claims of serious injury. Posts describing the accident differently than your official statement suggest inconsistency. Insurers routinely monitor claimants' social media. Make all accounts private and post nothing about your accident, injuries, or claim until everything is resolved.

Failing to mitigate damages by not following medical advice gives insurers arguments that you worsened your own injuries. If doctors recommend physical therapy and you don't go, insurers argue your prolonged recovery is your fault, not theirs. Follow all treatment recommendations and document reasons if you can't comply with any.

Comparison of Common Motorcycle Claim Denial Reasons vs. Successful Appeal Strategies

| Denial Reason | Why Insurers Use It | How to Counter It |

| Late reporting violation | Creates technical grounds for denial even when claim is otherwise valid; suggests claimant has something to hide | Provide evidence you reported within policy timeframe when properly calculated; show documented reasons for any delay (hospitalization, unavailable communication); cite state laws requiring reasonable reporting periods |

| Policy exclusion for modifications | Allows denial based on undisclosed changes to motorcycle that may or may not have contributed to accident | Obtain mechanic statement that modifications didn't cause or contribute to accident; show modifications were disclosed during policy application; argue exclusion doesn't apply to the specific type of accident that occurred |

| Disputed fault determination | Shifts liability to you based on insurer's investigation rather than objective evidence | Present police report assigning fault to other party; provide witness statements contradicting insurer's version; hire accident reconstruction expert to challenge insurer's technical conclusions |

| Pre-existing injury claims | Reduces or eliminates medical payment obligations by attributing injuries to conditions existing before accident | Obtain medical records showing no treatment for similar injuries before accident; get doctor's letter explaining how accident caused new injury or aggravated prior condition; show gap in treatment for prior condition proves it had resolved |

| Lack of supporting documentation | Claims insufficient evidence to verify accident occurred as described or that damages are accident-related | Return to accident scene for additional photos; obtain business security footage; track down witnesses you didn't interview initially; get repair estimates from multiple shops showing damage consistent with your accident description |

Frequently Asked Questions

Moving Forward After a Denial

A motorcycle accident claim denial doesn't end your options—it starts a new phase where preparation and persistence determine the outcome. Insurers count on claimants giving up after the initial denial, accepting that the company's decision is final. Understanding that denials are often negotiating positions rather than immovable conclusions changes how you approach the situation.

Focus your energy on building an evidence file that directly contradicts the specific reason stated in your denial letter. Generic appeals that simply argue "you're wrong" fail. Targeted appeals that address each element of the insurer's reasoning with concrete evidence succeed far more often.

Track your deadlines religiously and consider whether attorney involvement makes financial sense for your particular claim value and complexity. Some situations clearly benefit from legal representation, while others are straightforward enough to handle yourself.

The process takes time—often months from denial through successful appeal or settlement. Budget for this timeline both financially and emotionally. Understand that insurance companies move slowly and use delay as a strategy to pressure you into accepting less than you deserve.

Your denied claim isn't necessarily a lost cause. With the right evidence, proper procedure, and persistent follow-through, many denied motorcycle claims eventually result in payment—either through internal appeals, DOI intervention, or legal action. The key is refusing to accept the initial denial as the final word and methodically building the case that proves you're entitled to coverage.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer insights and guidance on motorcycle accident insurance claims, settlement processes, liability issues, coverage limits, medical compensation, and related insurance matters, and should not be considered legal or financial advice.

All information, articles, and materials presented on this website are for general informational purposes only. Insurance policies, liability standards, settlement practices, and state regulations may vary by jurisdiction and insurer. The outcome of a motorcycle accident claim depends on the specific facts of the accident, available evidence, policy language, and applicable law.

This website is not responsible for any errors or omissions in the content, or for actions taken based on the information provided. Users are strongly encouraged to consult with a qualified attorney or licensed insurance professional regarding their specific motorcycle accident claim before making decisions about settlements, negotiations, or coverage disputes.