Motorcyclist in leather jacket sitting across from insurance adjuster at office desk with accident documents and medical bills spread out

How to Negotiate a Motorcycle Accident Settlement Without a Lawyer

Content

Every year, lawyers pocket roughly one-third to two-fifths of what accident victims receive—money that could stay in your pocket if you knew how to negotiate effectively. For the right type of claim, representing yourself makes financial sense. Here's the catch: insurance adjusters negotiate settlements every single day while you're probably doing this for the first time in your life.

Should you go it alone? Maybe. The answer hinges on your specific situation. Got minor injuries with obvious fault? You'll probably do fine. Suffered a traumatic brain injury with disputed liability? You need professional representation yesterday. Between those extremes lies a gray area where the right knowledge and preparation determine whether self-representation succeeds or backfires.

This guide covers everything from photographing your wrecked bike to signing the final paperwork. You'll learn what evidence matters, how to calculate fair compensation, and which insurance company tricks to watch for. Most importantly, you'll recognize the warning signs that scream "hire a lawyer now" before you damage your case.

When Self-Representation Makes Sense for Motorcycle Accident Claims

Handling your own claim isn't always foolish. Sometimes it's the smartest financial move. The key is knowing which situations allow for successful self-representation and which ones will eat you alive.

Claim Scenarios Suitable for DIY Settlement

Picture this: someone blew through a stop sign and T-boned you at an intersection. Three witnesses saw it happen. The driver apologized profusely. Their insurance adjuster called you the next day accepting full responsibility. Your injuries involved an ER visit, four physical therapy appointments, and you're back at work feeling normal. This scenario practically begs for self-settlement.

Property damage claims work especially well without legal help. Your Harley needs $4,000 in repairs. The body shop wrote up a detailed estimate. The adjuster agrees with the numbers. No legal degree required—just documentation and follow-through.

Think about the math on smaller claims. Legal representation costs you anywhere from one-third to two-fifths of your final settlement check. On a $7,500 recovery, that's roughly $2,500 to $3,000 walking out the door. If you can negotiate that amount yourself through a few phone calls and letters, why give away thousands?

Soft tissue injuries that clear up within three to six months generally fall into DIY territory. You dealt with road rash, bruising, and muscle strains. Conservative treatment got you back to normal. Your medical expenses hit $3,200, you missed ten days of work, and now you're completely healed without lingering problems.

| Claim Characteristic | Self-Settle | Hire Attorney |

| Injury severity | Minor injuries with complete recovery inside six months | Serious injuries involving surgery or permanent disability |

| Liability clarity | Obvious fault backed by strong evidence | Conflicting stories about who caused the crash |

| Claim value | Total damages under $10,000 | Damages exceeding $25,000 or requiring future treatment |

| Time investment | You have 10-20 hours available for paperwork and calls | Complicated case demanding extensive legal work |

| Medical bills | Treatment costs under $5,000 with straightforward care | Expensive medical treatment or ongoing care needs |

| Insurance cooperation | Adjuster responds quickly and negotiates fairly | Bad faith delays, claim denials, or unreasonable offers |

Red Flags That Require Attorney Involvement

Severe injuries flip the script completely. Broken bones requiring surgical intervention, traumatic brain injuries, spinal cord damage, or injuries preventing your return to work—all these demand immediate attorney consultation. These cases involve complicated medical testimony, expert witnesses, and future damages that adjusters will fight tooth and nail to minimize.

Disputed liability means trouble. The other driver insists you were speeding or weaving between lanes. The police report says "fault undetermined." Witnesses contradict each other or don't exist. Insurance companies exploit any liability gray area to slash their payout. Fighting these battles solo rarely ends well.

Multiple responsible parties create nightmare scenarios. Three vehicles caused your crash. You got hit by a commercial truck with multiple overlapping policies. Figuring out which insurance company pays what percentage requires understanding coordination of benefits rules that most attorneys don't even master until they've handled dozens of cases.

Watch for claim denials or insulting lowball offers despite obvious liability and documented injuries. This signals the insurance company is playing hardball. They're betting you'll accept whatever they throw at you rather than hire representation. This bet pays off for them more often than you'd think.

Author: Hannah Pierce;

Source: spy-delhi.com

Permanent disability or disfigurement changes everything about valuing your claim. Visible scarring, chronic pain conditions, or permanent mobility restrictions carry long-term financial and emotional impacts extending far beyond your immediate medical costs. Lawyers use established precedents and sophisticated valuation methods to properly calculate these damages.

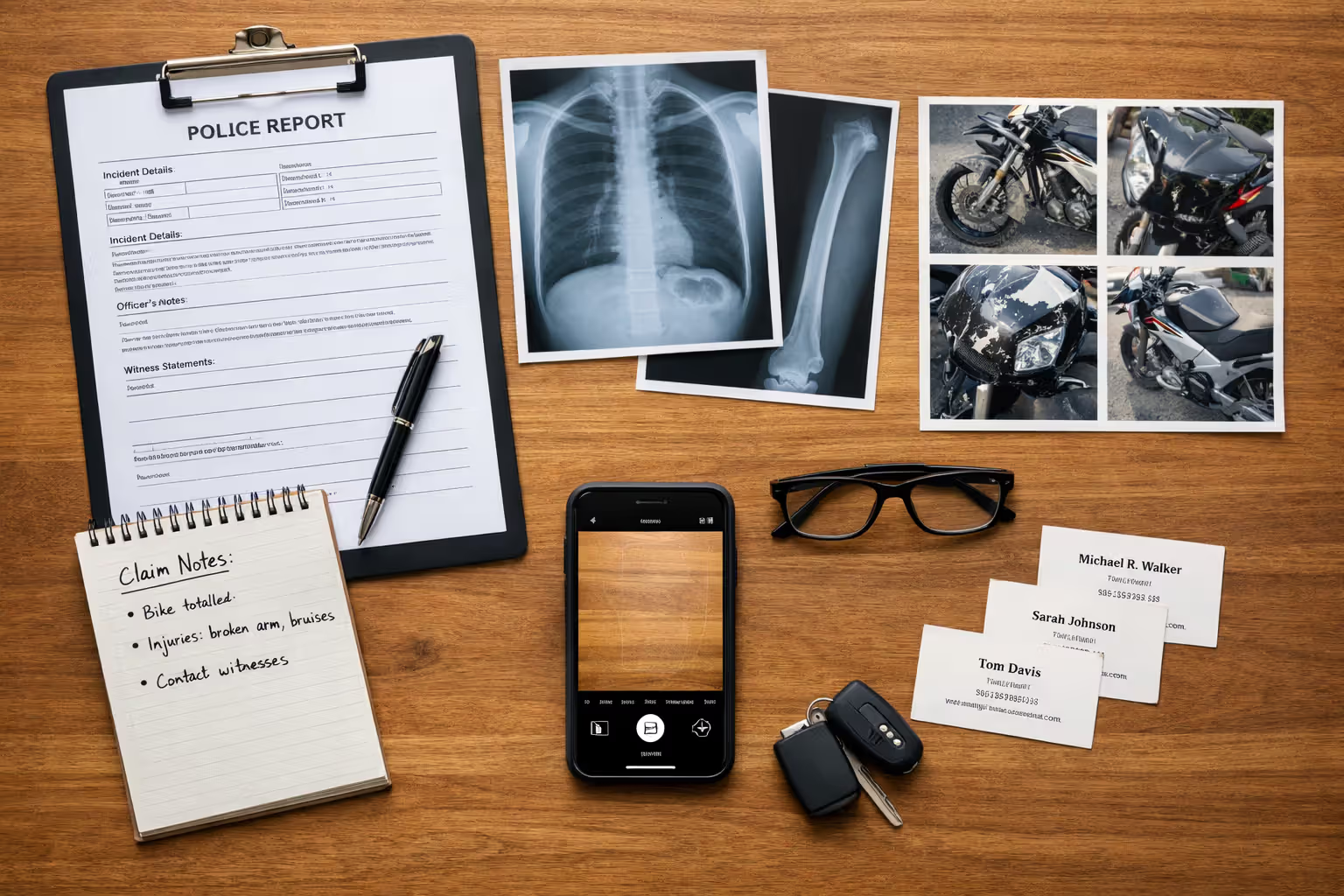

Gathering Evidence and Documentation After Your Motorcycle Crash

Your settlement value lives or dies based on evidence quality. Insurance adjusters trust documentation, not your word. Memories fade fast, scenes change, and without proof, you're fighting an uphill battle from day one.

Critical Photos and Physical Evidence to Collect

Before anyone touches those vehicles, photograph everything from multiple angles. Document skid marks and debris spread patterns. Shoot traffic control devices, intersection layouts, and road surface conditions. Get wide establishing shots showing spatial relationships, then zoom in for detailed damage close-ups. If weather played a role—rain, fog, glaring sun—capture that too.

Your motorcycle's damage needs exhaustive photographic documentation. Every scratch matters. Every dent counts. Every broken component tells part of your story. Shoot from different angles and lighting conditions. Include your protective gear in these photos—helmet damage, torn jacket, scraped gloves, damaged boots. Gear damage proves impact forces and supports injury severity claims.

Visible injuries demand immediate documentation. Photograph road rash, bruising, swelling, and lacerations right away. Continue photo documentation every two to three days tracking how injuries evolve. This visual timeline counters adjusters who later minimize injury severity by claiming damages weren't significant.

Keep physical evidence intact. That cracked helmet, those shredded jeans, that mangled saddlebag—store them safely. Don't repair your bike until the insurance company completes their inspection or you've finalized your settlement. These damaged items prove collision forces in ways that words never will.

Medical Records and Treatment Documentation

Get medical attention within 24 hours even if you feel okay. Adrenaline flooding your system masks pain temporarily. Some injuries—internal bleeding, concussions, soft tissue damage—don't announce themselves immediately. The longer you wait, the more ammunition adjusters have to argue your injuries came from somewhere else.

Collect every scrap of medical documentation. Emergency room reports, X-ray and MRI results, doctor's notes, physical therapy records, prescription receipts, and yes, even mileage logs for medical trips. Build a spreadsheet tracking dates, providers, services rendered, and costs incurred. Organization matters during negotiations.

Treatment compliance is non-negotiable. Skipping appointments or stopping therapy halfway through tells adjusters you weren't really injured. Disagree with your doctor's treatment plan? Discuss it with them and document that conversation. Don't just ghost your appointments.

Track daily life impacts in writing. Note your pain levels throughout the day. List activities you can no longer perform or that cause significant discomfort. Document sleep disruption and emotional effects. These contemporaneous notes become powerful evidence supporting non-economic damages that adjusters love to dismiss.

Police Reports and Witness Statements

Request the official police report within one week. Some jurisdictions offer online ordering; others require in-person visits to the station. This report contains the responding officer's fault assessment, any citations issued, and witness contact details. It carries significant weight even though it's not always admissible in court.

If bystanders saw your crash, grab their contact details on the spot. Names, phone numbers, email addresses—whatever they're willing to provide. Better yet, ask them to write brief statements describing what they witnessed while the memory remains fresh. Independent eyewitness testimony is gold during negotiations.

Some minor accidents don't trigger police response. In these cases, file your driver's report with your state DMV within the deadline (typically 10 days). This creates official documentation that the collision occurred.

Security cameras and traffic surveillance systems present time-sensitive opportunities. Nearby businesses often delete footage after 30-90 days. Visit immediately. Explain what happened, request they preserve relevant video, and follow up in writing. This footage can make or break disputed liability claims.

Author: Hannah Pierce;

Source: spy-delhi.com

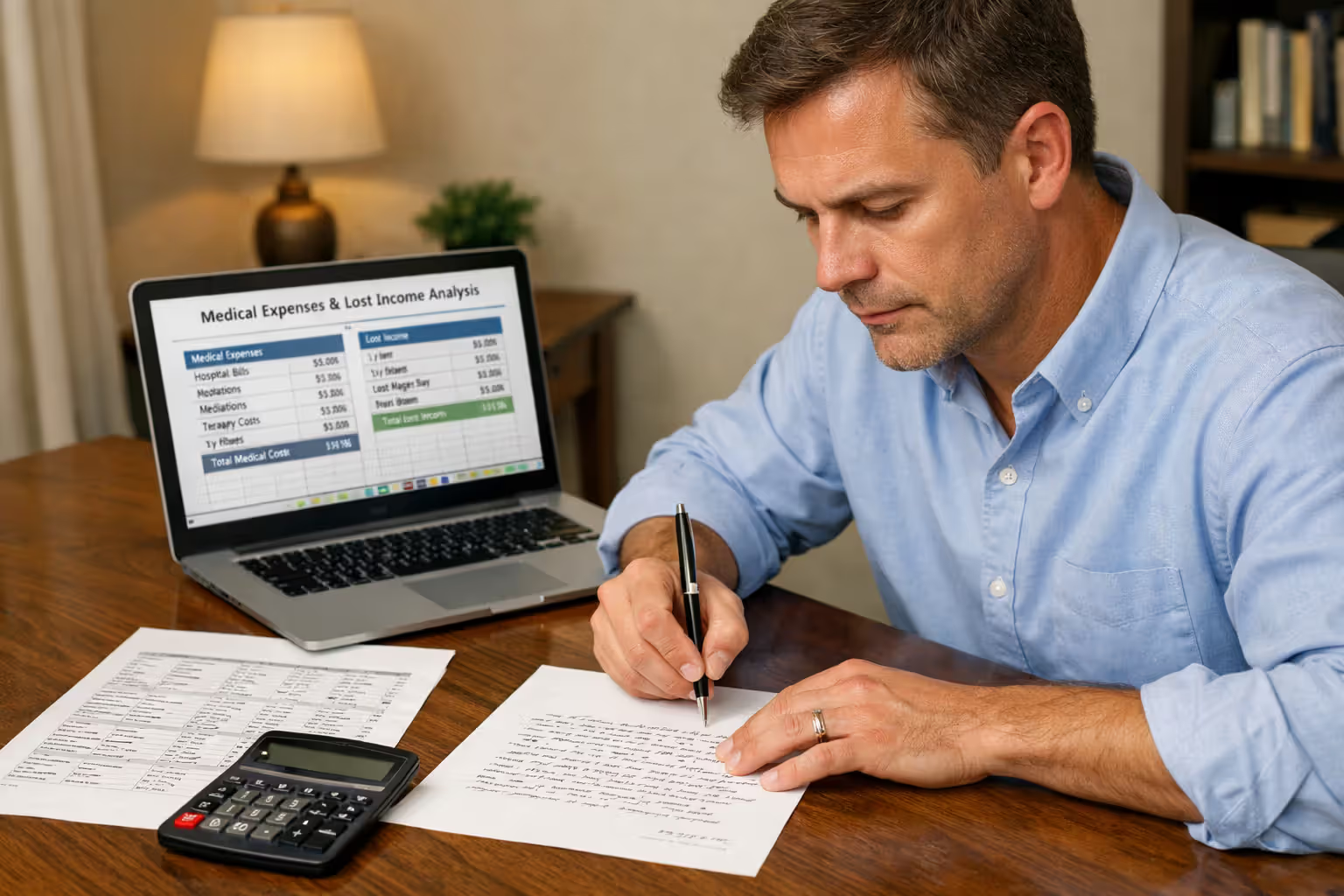

Calculating Your Motorcycle Accident Claim Value

Knowing your claim's genuine worth prevents premature settlement at inadequate amounts. Adjusters won't volunteer that they're authorized to pay three times what they initially offer. You must calculate reasonable ranges yourself.

Economic Damages: Medical Bills and Lost Wages

Economic damages involve actual dollar amounts you can prove with documentation. Total every medical expense: ambulance transport, emergency room treatment, hospital stays, physician consultations, diagnostic imaging, prescriptions, medical equipment, and continuing treatment costs.

Don't overlook future medical needs. Your doctor recommended six more physical therapy sessions or potential follow-up surgery. Include these projected costs using written estimates from medical providers.

Calculate lost wages using gross pay, not take-home amounts. Self-employed? Use tax returns, invoices, and bank deposits to prove lost income. Include vacation days or sick time you burned during recovery.

Lost earning capacity applies when injuries prevent returning to your previous occupation. A motorcycle courier who can no longer ride bikes has lost their career, not just temporary income. These claims typically need expert testimony—territory where self-representation gets dicey fast.

Property damage means motorcycle repair costs or fair market value if totaled. Add damaged riding gear, clothing, phone, and personal items destroyed in the crash. Obtain multiple repair estimates if the insurer's numbers seem low.

Non-Economic Damages: Pain and Suffering Multipliers

Pain and suffering lacks neat formulas, but adjusters use multiplier approaches. They take your medical expenses and multiply by some factor between 1.5 and 5 based on injury seriousness.

Minor soft tissue injuries typically receive 1.5 to 2 multipliers. Medical bills totaling $3,000 generate pain and suffering offers around $4,500 to $6,000. More serious injuries with objective proof like fractures or surgical intervention receive higher 3 to 5 multipliers.

Several factors push multipliers higher: permanent visible scarring, extended recovery periods, multiple surgical procedures, and injuries requiring long-term treatment. Factors dropping multipliers include pre-existing medical conditions, treatment gaps, and minimal objective findings on diagnostic tests.

The per diem approach assigns daily dollar values to your suffering and multiplies by recovery days. Argue your pain was worth $100 daily across 90 days of recovery? That's $9,000 in pain and suffering compensation.

Property Damage to Your Motorcycle

Insurance companies often handle property damage separately from bodily injury claims. This separation helps in straightforward cases but creates headaches when your bike's value gets disputed.

Actual cash value settlements compensate for pre-accident motorcycle value, not purchase price or outstanding loan balance. If you owe more than the bike's worth, you'll still carry debt after settlement. Gap insurance covers this shortfall—if you bought it.

Diminished value claims seek compensation for reduced resale value post-repair. Motorcycles with accident histories sell for thousands less than clean-title bikes. Many states don't recognize these claims and insurers fight them aggressively.

Total loss battles emerge when perspectives diverge on repair versus replacement decisions. Obtain independent valuations from motorcycle dealers or certified appraisers to support your position when disagreements arise.

Step-by-Step Negotiation Process With Insurance Adjusters

Negotiating with adjusters demands patience, documentation, and strategic thinking. Adjusters juggle 50-100 active claims simultaneously and want yours closed quickly and cheaply.

Writing Your Initial Demand Letter

Don't send demand letters until finishing treatment or reaching maximum medical improvement. Premature settlement means you can't claim future expenses or complications developing later.

Structure your demand letter professionally with detailed organization. Open with a concise accident narrative: date, location, how it unfolded, and why the other driver bears responsibility. Reference police reports and witness statements supporting your account.

Present your injuries thoroughly using medical documentation. List every healthcare provider, diagnoses received, treatments undergone, and current medical condition. Attach itemized billing showing total medical costs.

Describe injury impacts on daily living. Explain which activities became impossible, work you missed, pain you endured, and emotional toll extracted. Specific concrete examples beat vague suffering statements every time.

Calculate total damages with clarity. Separate economic damages (medical costs, lost income, property damage) from non-economic damages (pain and suffering). Demand a specific dollar amount running 20-30% above your actual target, creating negotiation room.

Include reasonable response deadlines—30 days works well. This creates urgency without seeming aggressive or unrealistic.

Responding to Lowball Settlement Offers

First offers will disappoint you. Count on it. Adjusters open negotiations with minimal figures hoping you'll accept from financial pressure or ignorance. View it as business strategy, not personal insult.

Reject first offers unless they meet or exceed your calculated value—which almost never happens. Respond in writing explaining offer inadequacy. Reference specific evidence the adjuster ignored, undervalued, or mischaracterized.

Counter-offer with a reduced demand, but don't plummet dramatically. They offered $8,000 against your $25,000 demand? Counter at $22,000. Demonstrate negotiation willingness without signaling desperation.

Request detailed explanation of their valuation methodology. Ask them to itemize calculations for each damage component. This forces justification of their numbers and frequently reveals valuation weaknesses.

Expect multiple back-and-forth rounds. Legitimate claims rarely settle after single counter-offers. Each exchange should progressively narrow the gap between positions.

Author: Hannah Pierce;

Source: spy-delhi.com

Common Insurance Company Tactics to Avoid

Recorded statement requests are traps disguised as routine procedures. Adjusters frame this as "just for our records" while hoping you'll contradict written statements or inadvertently admit partial responsibility. Politely refuse or keep responses extremely brief and consistent with your demand letter.

Delay tactics wear down claimants until they accept inadequate offers. Your adjuster doesn't return messages, repeatedly requests unnecessary documentation, or claims everything needs supervisor approval for weeks. Combat this by documenting every contact attempt and following up via email creating paper trails.

People representing themselves accept the insurer's medical bill assessment without pushback. Adjusters constantly argue certain treatments weren't medically necessary or were excessive, but they rarely have any medical training whatsoever. Always demand written explanations for any reduced medical expenses, and push back hard using your doctor's treatment notes justifying the care

— James Martinez

Comparative negligence arguments chip away at your settlement by assigning you partial blame. The adjuster suggests you were traveling too fast, not wearing appropriate gear, or violated traffic regulations. Counter with evidence proving you followed all applicable laws and safety practices.

Medical authorization forms seem harmless but grant adjusters access to your complete medical history going back years. They'll hunt for pre-existing conditions to argue your injuries weren't accident-caused. Provide only records directly related to accident injuries.

Quick settlement pressure involves offering immediate payment for fast claim closure. Adjusters know you're drowning in medical bills and lost paychecks. Don't let financial strain force acceptance of inadequate compensation.

Mistakes That Destroy Your Settlement Leverage

Minor errors during claims processing can cost thousands or completely tank your recovery. Insurance adjusters exploit these mistakes to deny claims outright or slash payouts dramatically.

Recording statements unprepared invites disaster. You might accidentally contradict earlier statements, downplay injury severity, or accept partial blame. If you absolutely must provide recorded statements, write key facts down first and stick to them religiously. Answer the specific question asked without volunteering additional information.

Quick settlement acceptance before understanding full damages is tempting when bills pile up fast. Many injuries worsen over time or demand additional treatment you didn't initially anticipate. Once you sign that release, your claim closes permanently regardless of complications developing later.

Statute of limitations deadlines kill claims forever. Each state imposes filing deadlines, typically two to four years for personal injury lawsuits. Even during active insurance negotiations, missing this deadline eliminates your leverage completely because you can no longer threaten litigation.

Social media posts create evidence ammunition against you. That photo of you standing at your nephew's wedding becomes "Look who's faking injuries!" in the adjuster's file. Adjusters and investigators routinely monitor claimant social media accounts. Lock everything down to private and post absolutely nothing about your accident, injuries, or activities until final settlement.

Fault admissions in any form inflict irreparable damage. Apologizing at the scene, texting the other driver you "didn't see them coming," or telling an adjuster you "should have braked sooner" all constitute admissions. Describe events factually without assigning yourself blame.

Injury exaggeration destroys credibility completely. Surveillance catching you performing activities you claimed were impossible makes adjusters assume everything was fabricated. Stay honest about actual limitations and genuine capabilities.

Delayed medical treatment creates causation arguments. Waiting three weeks for your first doctor visit lets adjusters argue injuries resulted from something else entirely. Seek treatment within 24-72 hours of your crash.

Combined property and injury settlements can limit options unnecessarily. Need immediate motorcycle repairs? Settle property damage separately while explicitly reserving injury claims. Once you sign a comprehensive release covering all damages, you can't later claim additional injuries.

Author: Hannah Pierce;

Source: spy-delhi.com

Legal Documents You'll Need to Finalize Your Settlement

Settlement agreements use specific legal language primarily protecting insurance companies. Understanding these documents before signing prevents nasty surprises later.

The settlement agreement or release form represents the core document. It specifies payment amounts, identifies which claims you're releasing, and confirms this resolves all accident-related issues. Read every single word carefully. Most releases are "general releases" meaning you waive all claims—known and unknown—against the at-fault party.

Pay close attention to release scope. Some releases cover only the at-fault driver while others include their employer, vehicle owner, insurance carrier, and anyone remotely connected. Understand exactly who you're releasing from future liability.

The consideration clause states what you receive for releasing claims. Verify this amount matches your negotiated settlement exactly. Also check whether stated amounts are before or after medical liens and subrogation claims get paid.

Medical lien resolution language addresses responsibility for paying outstanding medical bills or health insurance subrogation demands. If the release makes you responsible for liens, ensure your settlement amount adequately covers them.

Confidentiality clauses prevent discussing settlement terms publicly. These appear commonly in larger settlements. Decide whether you're comfortable with this speech restriction before signing anything.

Indemnification provisions sometimes require reimbursing the insurance company if additional accident-related claims surface later. This becomes problematic if another injured party later sues the at-fault driver and they attempt recovering from you.

Before signing anything, consider paying an attorney to review documents. Many lawyers will review settlement agreements for flat fees of $200-$500—worthwhile investment for larger settlements. This limited scope representation doesn't require hiring them for your entire case.

Never sign under time pressure. Adjusters demanding immediate signatures wave giant red flags. Take documents home, review carefully, and ask questions about anything unclear or concerning.

Verbal agreements mean nothing legally. Don't accept promises that something will be "handled later" or "isn't really a problem." If it's not written in the agreement, it doesn't exist.

After signing, keep complete copies of all settlement documents permanently. You'll need them for tax purposes and to prove claim resolution if questions arise years later.

FAQ: Motorcycle Accident Self-Settlement Questions

Handling motorcycle accident settlements without lawyers works for straightforward claims: minor injuries, obvious liability, and cooperative insurers. Success demands thorough documentation, realistic valuation, patient negotiation, and avoiding mistakes that destroy leverage.

Start by collecting comprehensive evidence immediately post-accident—photographs, medical records, witness information, and police reports. Calculate damages accurately by totaling economic losses and applying reasonable multipliers for pain and suffering. Approach negotiations strategically using well-crafted demand letters and willingness to counter inadequate offers with documented justifications.

Recognize when self-representation hits its limits. Serious injuries, disputed liability, bad faith insurance tactics, or claim values exceeding $25,000 typically demand professional legal representation. Money saved on lawyer fees won't compensate for settlements tens of thousands below true value.

Throughout the process, protect yourself by avoiding recorded statements, social media posts, and quick settlement pressure. Read every document thoroughly before signing, and don't hesitate investing a few hundred dollars for attorney document review before finalizing anything.

Your leverage comes from documentation quality, patience, and willingness to reject inadequate offers. Insurance adjusters close hundreds of claims annually—this is your one chance recovering fair compensation for injuries and losses. Invest the time to do it properly.