First-person view from a motorcycle at a busy urban intersection with cars and traffic lights ahead

How to Use a Motorcycle Accident Settlement Calculator to Estimate Your Claim

Picture this: you've just been discharged after three days in the hospital. The car that T-boned you at the intersection left you with a shattered femur, road rash covering half your back, and medical bills already hitting $47,000. Your employer wants to know your return-to-work date. You don't have one yet.

So you do what most people do—grab your phone and search "how much is my motorcycle accident worth?"

Within seconds, you're staring at settlement calculators that promise precise dollar figures. Just plug in some numbers, they say. Get your answer in minutes.

But here's the truth those websites won't admit upfront: these automated tools run kindergarten-level math on graduate-level problems. They're built on formulas that can't possibly factor in whether the driver who hit you was texting, whether your state caps pain and suffering at $350,000, or whether your permanent limp will cost you the construction job you've held for fifteen years.

Settlement calculators give you something—just not accuracy. They're closer to weather predictions three weeks out than actual forecasts of what you'll receive.

Real compensation gets determined through negotiation between people who understand strategy, leverage, and the specific details that make your case different from the ten thousand other motorcycle accidents this year.

What Factors Determine Your Motorcycle Accident Settlement Amount?

Two categories of damages drive your potential recovery: economic losses you can document with paperwork, and non-economic harm that exists regardless of whether a receipt captures it.

Economic damages represent every dollar that left your pocket or never made it there because of this crash. Your medical expenses come first—the ambulance bill ($1,800), emergency room evaluation ($3,200), imaging studies ($2,400), orthopedic surgeon's fee ($8,500), anesthesiologist ($1,900), hospital stay ($18,000 for three nights), prescription medications ($850), physical therapy ($145 per session for twenty-four sessions). Let's say you also need another surgery in eighteen months when the hardware in your femur starts causing problems. That future procedure adds another $15,000 to $22,000.

Property damage counts too. Your 2019 Harley Street Glide worth $16,500? Totaled. The $780 helmet that cracked open protecting your skull needs replacing. Your $450 leather jacket has torn completely through in three places. Boots, gloves, saddlebag, the GPS mount—everything that got destroyed or damaged goes into this calculation.

Lost wages extend beyond the obvious paychecks you missed during recovery. Maybe you earned $68,000 annually as an electrician before the crash. The injury forced you into a dispatcher role at $42,000 because you can't climb ladders anymore. That $26,000 annual gap, projected across your remaining twenty-three working years, represents $598,000 in lost earning capacity. Most riders completely forget to claim this.

Author: Ryan Whitlock;

Source: spy-delhi.com

Non-economic damages cover everything that hurts but doesn't come with an invoice. The physical pain you felt when the car's bumper struck your leg. The three months of agony during recovery. The nightmares where you relive the moment of impact. The embarrassment you feel about the visible scars on your arms. The frustration when chronic pain stops you from picking up your daughter.

Insurance companies value these damages using a calculation approach: economic losses get multiplied by a factor reflecting injury severity. Minor injuries—say, a broken collarbone that heals completely in ten weeks—might justify multiplying your economic damages by 1.5 or 2. More serious trauma like spinal injuries or traumatic brain damage can push that multiplier to 4 or even 5. The insurance company takes your $55,000 in medical bills and lost wages, multiplies by 3 for moderate injuries, and arrives at $165,000 for pain and suffering.

But who decides which multiplier to use? That's where calculators fall apart—choosing between 2x and 4x involves subjective judgment about dozens of case-specific factors.

Liability percentage can obliterate your settlement before you even start negotiating. Under comparative fault rules used by most states, whatever percentage of blame gets assigned to you reduces your recovery proportionally. The insurance company claims you were speeding 15 mph over the limit when their driver turned left across your path? They might argue you're 40% responsible. Your $180,000 claim drops to $108,000. A few states won't pay you anything if you're found 50% or 51% at fault—you cross that threshold and recovery goes to zero.

Injury severity gets measured on a spectrum from minor to catastrophic. Whiplash and contusions resolve in a few weeks. Fractures requiring surgery need three to six months of recovery. Permanent disabilities—amputations, spinal cord damage, chronic pain syndrome, traumatic brain injury—alter the entire trajectory of your life. Each step up this severity ladder adds substantial value.

Insurance adjusters scrutinize your medical records hunting for objective evidence. Fractures show up on X-rays. Ligament tears appear on MRI scans. Nerve damage gets confirmed through EMG testing. But soft tissue injuries that rely primarily on your own descriptions of pain? Adjusters challenge those aggressively because they're harder to definitively prove and easier for insurance companies to minimize as exaggerated.

Pain and suffering multipliers climb when you've got longer hospitalizations, multiple surgeries, permanent impairment ratings from treating physicians, visible scarring, or ongoing treatment requirements. A six-day hospital stay supports a higher multiplier than outpatient care. Three surgeries beat one. Permanent partial disability beats temporary limitations.

How Motorcycle Settlement Calculators Actually Work

These online tools execute basic math to produce estimates. Understanding the formulas reveals exactly why different calculators generate numbers all over the map.

The Multiplier Method Explained

This represents the most popular calculation approach. The formula looks like this:

Settlement Estimate = (Medical Bills + Lost Wages + Property Damage) × Severity Factor + The Original Economic Damages

Consider a rider with $42,000 in hospital bills, $13,500 in missed paychecks, and $8,200 in motorcycle damage. That's $63,700 in documented losses. The calculator applies a 3x multiplier for moderate injuries, creating $191,100 for pain and suffering. Add back that original $63,700, and you land at $254,800 total.

Which multiplier makes sense, though? Minor injuries—sprains, bruising, recovery inside a month—fall around 1.5 to 2. Moderate trauma involving fractures or surgical repairs but with complete eventual recovery lands between 2 and 3.5. Severe cases featuring permanent disability, chronic pain conditions, or major scarring justify 4 to 5 or higher. Catastrophic injuries like paralysis can push beyond 5.

Most calculators just ask you to categorize your own injury as "minor," "moderate," or "severe." You're making an educated guess. You're probably underestimating or overestimating based on zero legal experience evaluating thousands of injury claims.

Author: Ryan Whitlock;

Source: spy-delhi.com

Per Diem Calculation Approach

Alternative settlement tools employ a different formula. They assign a dollar value to each day you're experiencing injury-related pain and suffering, beginning with the crash date and running until you reach maximum medical improvement.

A common approach sets your daily rate at your normal daily earnings. Earning $85,000 yearly? That's roughly $233 per day. Recovery period lasting 180 days? That's $41,940 for pain and suffering, added to your economic losses.

This method works reasonably well for injuries with clear endpoints—you heal up, and life returns to normal. But what about permanent conditions requiring lifetime management? Some calculators attempt projecting pain decades into the future. That gets absurdly speculative fast.

Algorithm limitations undermine both approaches. No calculator can evaluate whether your case will resonate emotionally with twelve jurors. They don't recognize that the drunk driver who hit you had four prior DUIs, creating strong punitive damages potential. They can't incorporate that you've got preexisting degenerative disc disease in the same vertebrae you injured, which defense lawyers will exploit to argue reduced value. They miss subtleties about how your county's jury pool typically views motorcyclists.

| Method Type | How It Works | Best Used For | Typical Range | Limitations |

| Multiplier Method | Multiplies documented economic losses by severity factor (1.5-5) based on injury seriousness | Most injury scenarios; considered industry standard approach | $40K-$600K+ | Selecting appropriate multiplier requires experience and judgment; ignores case-specific negotiation dynamics |

| Per Diem Method | Calculates daily pain rate × total recovery days | Injuries with definite healing timelines and clear recovery endpoints | $15K-$120K | Daily rate assignment is arbitrary; struggles with permanent injuries requiring ongoing treatment |

| Economic Damages Only | Simply totals bills and lost paychecks without adding pain/suffering | Very minor injuries with obvious liability and quick recovery | $3K-$40K | Completely omits non-economic damages; produces massive undervaluation in most cases |

| Computer Algorithm Estimate | Processes multiple variables through proprietary calculations | Quick ballpark estimates for initial research | Highly variable | Black-box methodology; no transparency about underlying assumptions; frequently produces inaccurate results |

Step-by-Step: Using a Motorcycle Injury Settlement Calculator

Don't open a calculator and start guessing numbers. You need actual documentation assembled first—estimates based on guesses produce worthless results.

Collect every medical bill and treatment record covering your entire care: ambulance transport, emergency department evaluation, hospital admission, surgical procedures, orthopedic specialist visits, physical therapy sessions, pain management treatments, pharmacy receipts. Include medical equipment—whether crutches, knee braces, back supports, or TENS units your doctor prescribed. Still receiving treatment? Ask your physician what additional care you'll require and get cost estimates for those future procedures.

Calculate your lost income with precision. Gather recent pay stubs covering the period you couldn't work. Salaried employee? Take annual compensation, divide by 52, then multiply by weeks missed. Hourly worker? Multiply your hourly rate by the hours you would've worked. Self-employed riders should pull tax returns and bank statements demonstrating normal income flow before the crash. Lost a promotion opportunity or had to accept a lower-paying position because of permanent limitations? Document that income difference carefully.

Document all property damage with repair estimates or replacement valuations for your motorcycle, helmet, riding jacket, pants, boots, gloves, and any other equipment destroyed in the crash. Photographs showing your mangled bike establish the extent of damage clearly.

Assess your injury severity honestly. Most calculators provide categories to choose from. Minor typically means complete recovery within a few weeks without surgical intervention. Moderate encompasses fractures or surgical repairs but with anticipated full healing. Severe involves permanent functional impairment, ongoing pain requiring management, or substantial visible scarring. Catastrophic includes paralysis, brain damage with cognitive deficits, or amputation.

Input fault percentage if it's been established. Police reports, witness statements, and traffic citations help determine who caused the collision. The other driver ran a red light while you proceeded legally through a green? You're probably zero percent at fault. You were lane-splitting at 90 mph in moderate traffic? You might shoulder partial responsibility.

Treat the output with healthy skepticism. A calculator might display $185,000. Run identical information through three other tools and you'll see $138,000, $227,000, and $103,000. These wild variations expose the tools' fundamental unreliability rather than providing a useful valuation range.

Recognize what the calculator can't evaluate. Was the other driver impaired by alcohol or drugs? Did the crash occur in a construction zone with inadequate safety barriers? Do you have prominent facial scarring that affects your daily social interactions? Are you a particularly sympathetic plaintiff—maybe a single parent who volunteers with kids? These elements increase settlement value substantially but don't fit into calculator input fields.

Why Online Calculator Estimates Differ from Actual Settlements

Insurance adjusters aren't running the same free calculators you discovered through Google. They've got proprietary evaluation software like Colossus that analyzes dozens of variables—your treatment frequency patterns, the specific diagnostic codes your providers documented, regional settlement history data, and significantly more.

Insurance company strategies systematically minimize claim values. Adjusters receive training to identify reduction opportunities at every stage. You delayed seeking treatment for eight days after the crash? They'll argue the injuries couldn't have been genuinely serious. You attended physical therapy 28 sessions? They'll insist 12 sessions should've resolved your complaints. You've got soft tissue injuries without accompanying fractures? They'll minimize these because X-rays don't capture them, making them easier to dispute.

Initial settlement offers typically land somewhere between 25-55% of reasonable value. Adjusters fully expect counteroffers and rejection. Your calculator estimates $135,000. Their opening proposal? $52,000. Many unrepresented riders accept these lowball offers without realizing they're leaving substantial money unclaimed.

Author: Ryan Whitlock;

Source: spy-delhi.com

Negotiation variables create outcome unpredictability. Your patience matters significantly—insurers gradually increase offers for claimants who'll reject multiple proposals and wait months for fair value. Your demonstrated willingness to actually file a lawsuit changes everything. Once you retain counsel and formally sue, settlement offers often jump 40-80% because insurers now face litigation costs, expert witness fees, and jury verdict risk.

The at-fault driver's policy limits can impose a hard ceiling. They carry just $25,000 in bodily injury coverage (surprisingly common in many states), but your damages total $195,000? That calculator estimate becomes largely irrelevant unless you've got underinsured motorist coverage through your own policy or can identify additional liable parties.

State laws introduce variables calculators rarely touch. Several jurisdictions cap non-economic damages in injury cases—sometimes at $250,000, $350,000, or $500,000 depending on the state. Others follow pure comparative negligence (you can recover even at 99% fault, just reduced proportionally), while some use modified comparative fault rules with 50% or 51% cutoff thresholds that completely bar recovery if you exceed them. Statutes of limitations range from one year to six years for filing suit, depending on jurisdiction.

Even within a single state, venue dramatically impacts results. Juries in urban plaintiff-friendly counties consistently award higher verdicts than those in conservative rural areas. Insurers adjust settlement offers based on where you'd actually file your lawsuit and which jury pool would hear your case.

Case-specific circumstances that no algorithm can process include:

- Whether the at-fault driver appears credible or evasive when testifying

- If crash reconstruction experts support your version of how the collision occurred

- How sympathetic and believable you come across to potential jurors

- The persuasiveness of your treating physicians' medical opinions

- Whether you missed scheduled appointments or ignored treatment recommendations

- Prior injuries to the same body regions (insurers aggressively argue preexisting conditions)

- Your age and occupation (younger workers have more earning years ahead; physical jobs suffer more from mobility restrictions)

The value of a case is not determined by a formula. It is determined by the facts, the law, the venue, and the people involved

— Gerry Spence

Common Mistakes That Reduce Your Motorcycle Accident Payout

Accepting the insurer's first offer costs injured riders more compensation than any other single mistake. Insurance companies count on your financial pressure or assumption that their number represents fair value. That $48,000 initial proposal might become $122,000 after persistent back-and-forth negotiation over several months. Once you sign that release document, though, the claim closes forever—even if you later discover you accepted $70,000 less than reasonable value.

Failing to account for future medical costs leaves you responsible for expenses that should've been covered in your settlement. Orthopedic injuries commonly require additional surgical procedures years later—hardware removal, revision surgeries, or joint replacements. Brain injuries can demand ongoing cognitive therapy for decades. Significant scarring might need multiple revision procedures for functional or cosmetic improvement. Get your treating physician to outline anticipated future treatment requirements and associated costs before you even consider settling.

Ignoring non-economic damages entirely happens when injured riders focus exclusively on bills and lost paychecks. In serious injury scenarios, pain and suffering compensation frequently exceeds your economic damages substantially. You broke five ribs, fractured your collarbone, and suffered extensive road rash across your torso and arms? The physical agony during the three-month healing process, the psychological trauma from the crash itself, the anxiety about riding again, and the permanent scarring across visible skin all warrant significant additional compensation beyond what your medical bills total.

Neglecting property damage items reduces your total recovery unnecessarily. Beyond the motorcycle itself, your helmet must be replaced after any impact (they provide one-crash protection only). Your riding jacket, gloves, boots, and pants have genuine replacement value. Phone or GPS unit in your saddlebag destroyed? Include it. Aftermarket modifications and customization on your bike should be valued at actual replacement cost, not just the stock model's baseline price. Custom exhaust, upgraded suspension, performance tune—everything adds value.

Settling before reaching maximum medical improvement happens when you feel mostly recovered and accept compensation before your condition stabilizes. You feel 80% better at five months and take the money. Then eight months later you're still experiencing chronic pain requiring injection therapy and ongoing treatment. Too late—you already settled. The insurer owes zero additional dollars for future treatment. Always wait until your physician confirms you've improved as much as medical intervention can achieve.

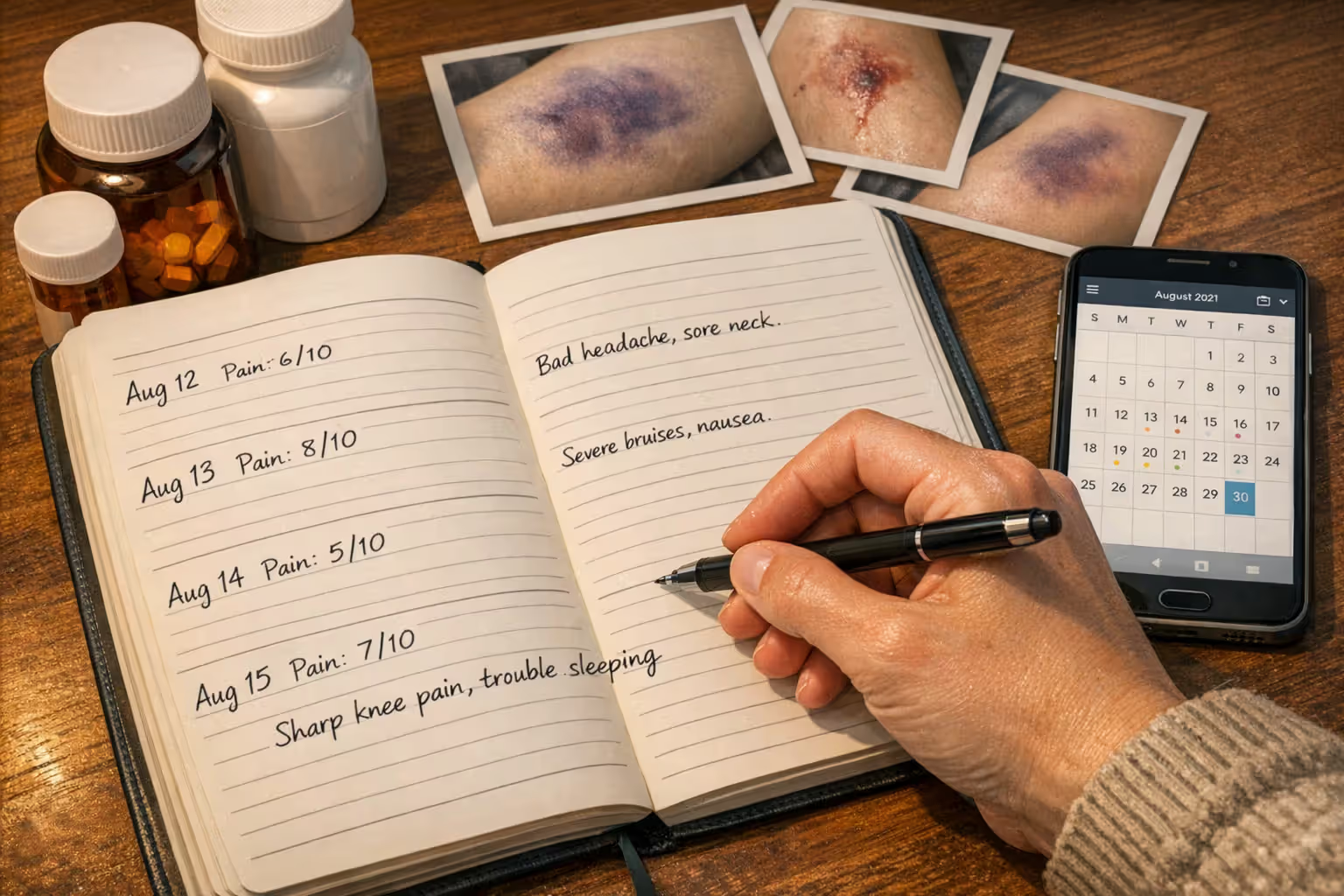

Not documenting pain and suffering adequately makes these damages harder to justify during negotiation. Maintain a daily journal recording pain levels on a 1-10 scale, activities you can no longer perform, sleep disruption, mood changes, and emotional struggles. Take photographs documenting bruising progression, swelling evolution, and scars as they develop and fade. These contemporaneous records help attorneys argue convincingly for higher pain and suffering multipliers.

Author: Ryan Whitlock;

Source: spy-delhi.com

Misunderstanding settlement tax treatment can create unpleasant surprises. Compensation for physical injuries generally isn't subject to federal income tax. However, punitive damages are fully taxable. Interest on your settlement is taxable. If your settlement includes a component representing wage loss, that portion might constitute taxable income. Consult a CPA before spending your settlement money to understand your specific tax obligations.

When to Use a Calculator vs. Consulting a Personal Injury Attorney

Settlement calculators serve a purpose for initial research, but specific situations absolutely demand professional legal guidance.

Damage amount thresholds offer practical guidance: once your losses approach or surpass $25,000, attorney representation typically increases your net recovery even after their contingency fee gets deducted. Multiple studies consistently demonstrate that represented claimants receive settlement offers averaging 3.5 times higher than those negotiating alone. An attorney taking 33% of a $120,000 settlement leaves you with $80,400—substantially better than the $37,000 you might have accepted handling negotiations yourself without legal expertise.

Minor injuries with under $5,000 in medical expenses, complete recovery within a month, and undisputed liability? You can probably manage direct negotiation with the insurance adjuster. Anything exceeding that complexity typically benefits from legal representation.

Complex medical cases need attorneys. Brain injuries involve sophisticated medical evidence about cognitive impairments, memory deficits, and personality changes. Spinal injuries require expert medical testimony about permanency ratings and functional limitations. Scarring and disfigurement claims benefit from lawyers who've handled hundreds of similar cases and understand how to maximize non-economic damages for visible injuries affecting social interactions and self-esteem. Calculators can't replicate the presentation strategies and negotiation tactics that substantially increase value in these scenarios.

Disputed liability situations where the insurance company claims you caused or substantially contributed to the crash demand thorough legal analysis. Attorneys investigate by obtaining official police reports, locating and interviewing witnesses, hiring accident reconstruction specialists, and subpoenaing traffic camera footage or dashcam video. If the insurer alleges you're 70% responsible but you believe you're blameless, that liability dispute affects hundreds of thousands of dollars in potential compensation. Getting this right requires investigation resources and expertise.

Insurance bad faith circumstances occur when insurers engage in unfair claim practices—denying legitimate claims without conducting reasonable investigation, refusing to make fair settlement proposals when liability is clear, or unreasonably delaying claim resolution hoping you'll give up. Attorneys can pursue separate bad faith claims that add punitive damages and attorney fees to your compensation. Calculators don't account for these additional damage categories that can double or triple your total recovery.

Multiple potentially liable defendants complicate everything substantially. A car pulled out in front of you, but the road construction contractor created visibility problems by placing equipment that blocked sight lines. You might have claims against both the negligent driver and the construction company. Coordinating claims against multiple defendants while maximizing total recovery requires legal strategy and extensive experience.

Permanent life-altering consequences like permanent disability ratings, chronic pain syndrome requiring ongoing pain management, or complete inability to ever return to your previous career field justify getting legal counsel involved immediately. These cases frequently involve six-figure or seven-figure settlements where accurate valuation requires understanding life care plans prepared by medical experts, vocational rehabilitation assessments, and economist testimony about lifetime lost earning capacity.

You can certainly use a calculator initially to generate ballpark figures, then consult attorneys for case-specific professional evaluation. Most personal injury lawyers offer free initial consultations and work on contingency fee arrangements—you don't pay anything upfront, and they don't collect fees unless they successfully recover compensation for you.

Frequently Asked Questions About Motorcycle Settlement Calculators

Understanding Your Path to Fair Compensation

Settlement calculators offer a reasonable research starting point for understanding potential claim values, but they absolutely cannot replace thorough case evaluation by experienced legal professionals who actually know what they're doing.

The formulas powering these automated tools—whether multiplier approaches or per diem calculations—produce mathematical estimates that completely ignore the human elements, negotiation dynamics, and legal complexities ultimately determining what compensation you actually collect.

Your real settlement depends on factors no algorithm captures: your negotiator's skill and decades of experience, the quality and completeness of your documentation and evidence, jurisdiction-specific jury verdict tendencies, the insurance company's internal assessment of their litigation risk if you proceed to trial, and dozens of case-specific circumstances unique to your situation. A calculator might project $125,000 while your case is genuinely worth $210,000 with proper legal strategy and compelling presentation—or perhaps just $72,000 because of comparative negligence issues the calculator weighted incorrectly or missed completely.

Use these tools to educate yourself about damage categories, basic valuation methodologies, and what factors generally matter. Recognize that economic damages create your foundation—every dollar of medical costs and lost wages requires solid documentation and convincing justification. Understand that non-economic damages for pain, suffering, and lost quality of life frequently equal or exceed economic losses when injuries are serious and permanent.

Then look past the calculator's projection. Assemble comprehensive documentation covering every aspect of your losses, avoid the common costly pitfalls like accepting initial lowball offers or settling before you finish treating, and honestly evaluate whether your case complexity justifies professional legal representation. For significant injuries, disputed liability, or potential settlement values exceeding $25,000, attorney involvement typically substantially boosts your net recovery despite contingency fees taking a percentage of the total.

That number glowing on your computer screen represents a mathematical exercise based on limited information, nothing more. Your actual settlement reflects the complete reality of your injuries, losses, evidence strength, and the strategic decisions you make throughout the entire claims process from start to finish. Treat calculators as educational tools for learning rather than crystal balls predicting your future, and you'll position yourself substantially better to secure compensation truly reflecting your damages and losses.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer insights and guidance on motorcycle accident insurance claims, settlement processes, liability issues, coverage limits, medical compensation, and related insurance matters, and should not be considered legal or financial advice.

All information, articles, and materials presented on this website are for general informational purposes only. Insurance policies, liability standards, settlement practices, and state regulations may vary by jurisdiction and insurer. The outcome of a motorcycle accident claim depends on the specific facts of the accident, available evidence, policy language, and applicable law.

This website is not responsible for any errors or omissions in the content, or for actions taken based on the information provided. Users are strongly encouraged to consult with a qualified attorney or licensed insurance professional regarding their specific motorcycle accident claim before making decisions about settlements, negotiations, or coverage disputes.