Motorcycle parked at a city intersection with legal settlement documents and a pen on a nearby surface, warm evening light, urban background

How to Choose Your Motorcycle Accident Settlement Payout Method

Your attorney just called with news you've been waiting months to hear. The insurance company finally agreed to settle. Your motorcycle accident case—the one that's consumed your life since that driver turned left across your lane last year—is wrapping up at $500,000. You're relieved. You're excited. Then your lawyer asks a question that catches you completely off guard: "Do you want the full amount wired to your account next month, or would you rather set up monthly payments that continue for the next two decades?"

Most riders I talk to haven't thought past getting the settlement approved. The delivery method? That wasn't even on their radar. But here's the reality—this decision impacts everything. Your tax situation. Whether creditors can grab your money. If you'll have funds remaining in 2035 or if you'll blow through it all by 2027. The wrong choice here can wreck the financial security you just fought so hard to obtain.

I'm breaking down both major approaches with actual dollar amounts, real-world consequences, and straight talk about which path makes sense when. This settlement payment motorcycle accident guide gives you the information you need before signing anything.

How Motorcycle Accident Settlements Are Typically Paid Out

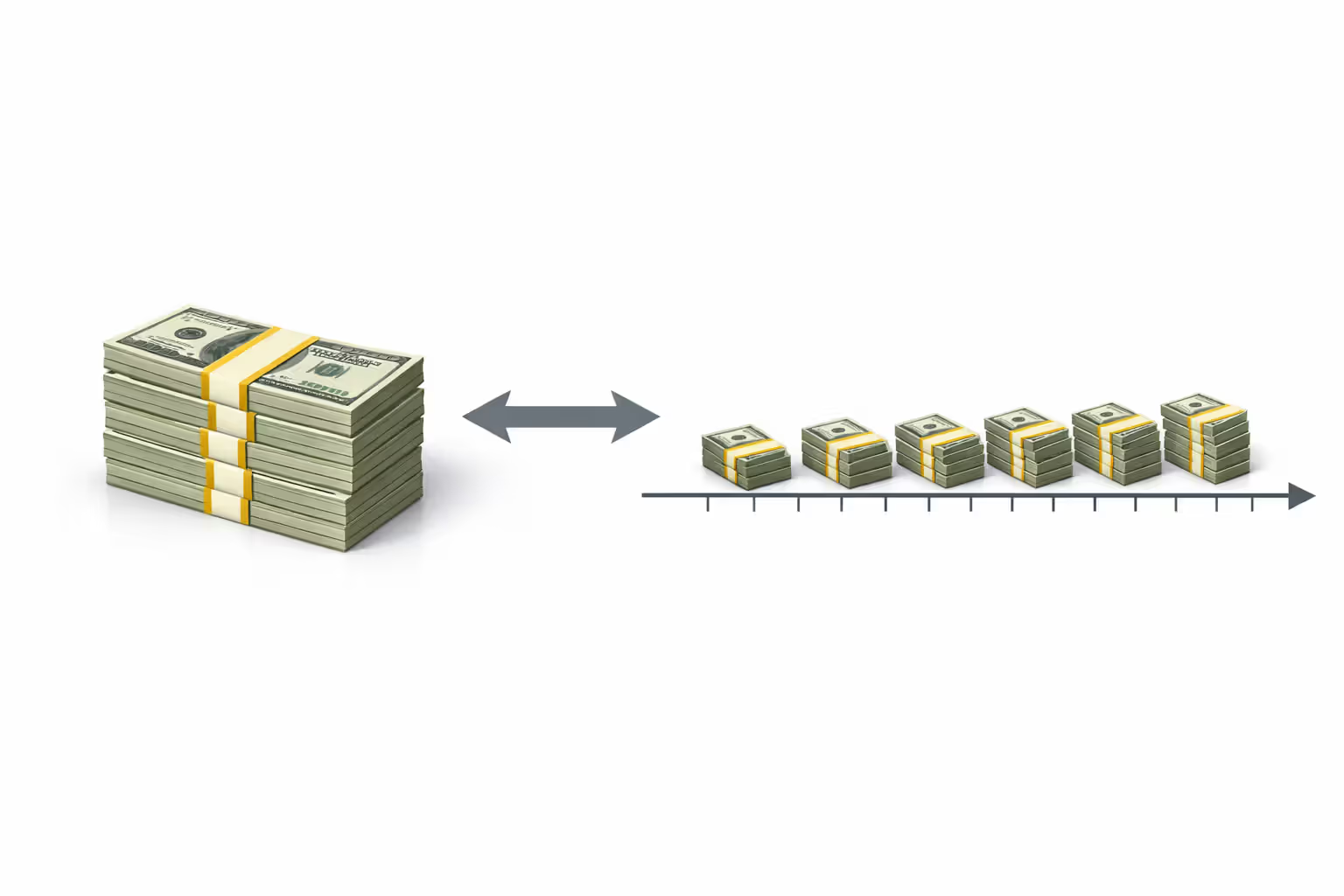

Two main settlement payout motorcycle accident options exist: getting everything at once versus getting it over time. The difference isn't subtle. Option one means signing the release paperwork today and seeing your complete settlement hit your bank account within 6-8 weeks. Option two means establishing a payment plan where money shows up monthly, quarterly, or annually for however many years you negotiate—sometimes for the rest of your life.

Who decides which route you take? That depends on leverage and settlement size. Small cases—anything under $50,000—rarely offer payment options. Insurance companies won't bother with the paperwork hassle and ongoing administrative costs when they can just cut one check and close your file forever. But once you're discussing six-figure agreements, both doors typically open. You can negotiate your preferred delivery method as part of the overall settlement terms.

Here's what surprises most people: insurance companies actually prefer spreading out payments on bigger cases. Sounds backwards, doesn't it? They're not doing you favors. When they set up your payment plan, they purchase what's called an annuity from a separate life insurance company. That annuity might cost them $420,000 today but pays you $500,000 over twenty years. They save cash immediately, remove your case from their liability ledgers right away, and transfer all future payment obligations to the annuity provider.

Author: Ryan Whitlock;

Source: spy-delhi.com

Your lawyer's compensation structure matters more than you'd think in this decision. Most personal injury attorneys work on contingency—that standard 33-40% fee. Some collect their entire cut upfront whether you choose one payment or many. Others agree to receive their fee on the same schedule as your payments if you go that direction. See why this creates potential conflicts? If your attorney has office rent due, three paralegals on payroll, and litigation expenses piling up, they might steer you toward the lump sum even when installments would better protect your interests. Before making your call, ask directly: "How does my choice affect when you get paid?"

State laws rarely force one method over another in typical adult motorcycle injury settlements. You'll find exceptions—workers' compensation cases sometimes require structured payments by statute, and settlements involving injured kids often need court-supervised payment plans. But for standard adult motorcycle crash cases? You're generally free to choose, assuming you can negotiate it with the other side.

Lump Sum Settlements: Receiving Your Full Payment at Once

The lump sum motorcycle settlement guide starts with its most obvious selling point: complete, immediate control over every dollar you negotiated. Sign the release, wait for the check to clear, and suddenly your entire settlement sits available for whatever you need.

Advantages of Taking a Lump Sum Payment

Immediate financial relief solves problems that can't wait. You're staring at $85,000 in medical bills currently in collections. Your mortgage lender sent a foreclosure notice last month. Credit card companies call daily. The bike was totaled, and you've been borrowing transportation from family members who are getting tired of helping. A lump sum lets you eliminate all these crises today instead of trying to manage them while waiting years for monthly checks to accumulate enough to matter.

Investment flexibility becomes significant if you actually understand financial markets or work with a competent advisor who isn't just selling products. Let's say $400,000 lands in your account tomorrow. You could spread it across index funds tracking the S&P 500, municipal bonds throwing off tax-free income, real estate investment trusts, or dividend-paying stocks. Historical stock market returns average around 10% annually (with massive ups and downs along the way). If you actually achieve 7% average growth after inflation, your money compounds substantially across decades—potentially delivering more than rigid payment schedules would provide.

Complete flexibility handles life's curveballs that nobody sees coming. Maybe your son gets accepted to Stanford but you need $40,000 for his freshman year. Perhaps you need a $55,000 wheelchair-accessible van to accommodate your injuries. Or maybe your best friend's profitable restaurant needs a $75,000 capital infusion and you'd become a partner with real equity. With cash sitting in your account, you control exactly when and how those dollars get deployed. Structured plans lock you into inflexible schedules that are nearly impossible to modify once established.

Administrative simplicity appeals to people who hate ongoing paperwork and monitoring requirements. One payment arrives. You deal with one tax situation. Done. You won't spend the next two decades tracking whether payments arrived on schedule, monitoring whether your annuity company remains financially stable, or filing address changes every time you move.

Drawbacks and Risks of Lump Sum Payouts

Research studying lottery winners tells a harsh story that applies directly to settlement recipients: roughly 70% of people receiving sudden large windfalls lose everything within just a few years. Motorcycle crash victims face identical risks. That $300,000 feels massive when it first arrives. Then you help your sister with her business ($40,000 seemed reasonable), eliminate all debts ($75,000), purchase a truck ($45,000), take your family on a much-deserved vacation to Hawaii ($12,000), invest in your cousin's "can't-miss" cryptocurrency opportunity ($50,000), and make several other well-intentioned decisions. Twenty-four months pass and you're back in financial stress—except now the settlement that was supposed to last twenty years is gone.

Creditor exposure creates real legal problems once lump sums hit your bank account. Those medical providers who waited patiently during litigation? They can potentially garnish accounts or file judgments accessing those funds (your state's exemption laws determine specifics). Credit card companies, collection agencies, and other creditors suddenly become aggressive once they discover you've received money. Structured payment plans often receive stronger legal protection from creditor claims in many states because technically the money hasn't been paid to you yet.

Investment risk cuts both directions. Sure, you might grow your settlement to $800,000 through smart decisions. You might also watch $150,000 evaporate if you invest right before a market crash. Unlike structured settlements guaranteeing every payment regardless of market conditions, your lump sum investment carries complete exposure to volatility, inflation, and your own mistakes.

Temptation affects even financially responsible people. When you're suddenly holding hundreds of thousands of dollars, family members need "temporary loans," investment "opportunities" appear from everywhere, and lifestyle inflation creeps into spending patterns. That new pontoon boat seems perfectly reasonable when you've got $400,000 available. Three years later, you've spent $250,000 and have nothing tangible to show for it.

Author: Ryan Whitlock;

Source: spy-delhi.com

Structured Settlement Payments: Understanding Installment Options

An installment settlement motorcycle accident guide requires understanding that structured settlements aren't one-size-fits-all arrangements. You can customize payment timing extensively, creating financial plans matching your specific medical needs, family situation, and security goals.

How Structured Settlements Work for Motorcycle Injury Claims

When you accept installment payments, the defendant's insurance carrier purchases an annuity contract from a top-rated life insurance company. This annuity becomes the funding mechanism for your future payments. Important distinction worth understanding: you don't actually own the annuity itself—you own rights to receive payments from it. This legal detail matters, especially regarding taxes and creditor protection.

Payment timing can be designed in countless configurations matching what you actually need:

- Level payment arrangements: Identical amounts arrive monthly, quarterly, or annually for a set number of years

- Increasing payment designs: Payments grow by a fixed percentage each year to combat inflation

- Hybrid arrangements: Immediate cash for urgent needs, followed by ongoing periodic payments covering living expenses

- Deferred payment plans: Payments don't start until years in the future (useful if you're still earning income but want guaranteed retirement funding later)

- Lifetime payment designs: Guaranteed income continuing as long as you're alive, with various minimum payment guarantees available

A realistic structure for a $500,000 motorcycle accident settlement might look like this: $100,000 delivered immediately, $2,500 arriving monthly for life, plus $25,000 annual payments for ten years. This combination provides immediate cash for pressing medical bills and debts, ongoing monthly income covering daily living expenses, and annual lump sums handling larger expenses like vehicle modifications or medical equipment.

Annuity company selection matters enormously—we're literally talking about the difference between financial security and catastrophe. You need companies carrying the highest financial strength ratings: A++ or A+ from A.M. Best, or AAA from Standard & Poor's. If your annuity company goes belly-up financially, your payments stop. Period. Unlike bank deposits with FDIC insurance, annuities lack federal protection. Most settlement agreements specify only top-rated companies, but verify this detail meticulously before signing anything.

Author: Ryan Whitlock;

Source: spy-delhi.com

Benefits of Choosing Installment Payments

Guaranteed income eliminates market anxiety and personal mistakes from the equation. Stock market crashes? Doesn't touch you. Economic recession? Your payments still arrive on schedule. You make terrible investment choices? Doesn't matter—your structured settlement keeps paying regardless. This reliability makes budgeting straightforward and removes long-term financial uncertainty.

Protection from financial mismanagement sounds insulting to say out loud, but it's honest. If you've never successfully managed money, struggle with impulse purchases, or have family members constantly needing financial "help," structured payments remove the risk of depleting everything prematurely. Money arrives gradually in manageable chunks, preventing catastrophic all-at-once mistakes.

Creditor protection varies significantly by state but generally offers stronger security than lump sums sitting in accessible bank accounts. In many jurisdictions, future structured settlement payments receive exemption from creditor claims. That medical provider trying to collect $50,000? They usually can't garnish payments you haven't received yet (though they might attempt garnishing individual payments as they arrive, depending on your state's laws).

Tax advantages for qualifying payment types can save tens of thousands of dollars. We'll cover taxes comprehensively in the next section, but structured settlements compensating physical injury claims receive favorable tax treatment—payments arrive completely tax-free, and growth occurring within the annuity never gets taxed.

Family security through guaranteed payments ensures loved ones receive financial support even if you mismanage money. Some structures include death benefits, continuing payments to designated beneficiaries if you die before receiving all scheduled amounts.

Limitations of Structured Settlement Agreements

Inflexibility stands as structured settlements' biggest drawback. Once you've signed the settlement release and the annuity company has purchased your contract, you generally cannot modify the payment schedule. At all. If you suddenly need a large sum for emergency surgery, a home down payment, or a business investment, you're stuck waiting for scheduled payments.

The secondary market offers an escape—companies will buy your structured settlement payment rights for immediate cash—but you'll pay brutally. These factoring companies typically offer 50-70 cents per dollar, meaning you forfeit 30-50% of your settlement value accessing your own money. State laws regulate these transactions and require court approval, but they're legal in most states. If you suspect you might need to sell payments later, just take everything upfront initially and avoid losing a third of your settlement to factoring companies.

Inflation quietly destroys purchasing power over time. That $3,000 monthly payment covers expenses comfortably in 2025. Fast forward to 2045: inflation has gutted its real value by 40-50%. You can structure increasing payments that rise annually, but this means accepting lower initial payments—a trade-off that doesn't work when you need money immediately.

No investment upside means you completely miss potential market gains. If stocks deliver 8% annual returns over the next twenty years, you've sacrificed substantial growth by accepting fixed payments instead of investing a lump sum. Of course, you've also dodged potential losses.

Death before receiving everything creates problems depending on your structure design. Some annuities are "life only," meaning payments stop immediately when you die regardless of how much you've collected. If you die after receiving $100,000 from a structure designed to pay $500,000 over your lifetime, the remaining $400,000 vanishes—the annuity company keeps it. Other structures guarantee minimum payment periods or include death benefits for beneficiaries. The structure design you select dramatically affects what happens to remaining funds if you die early.

Factors That Should Influence Your Payout Decision

Your payout choice motorcycle accident settlement guide starts with your medical reality. Do your injuries require ongoing treatment for years ahead? Spinal cord injuries, traumatic brain injuries, complex regional pain syndrome, and severe orthopedic damage often demand lifetime medical care. If you anticipate needing Medicare or Medicaid eventually, structured payments can help preserve eligibility—large lump sums count as assets that may disqualify you from benefits. If your injuries have substantially healed and you're returning to normal work, immediate payment offers greater flexibility.

Age and life expectancy create dramatically different scenarios. A 25-year-old with a $500,000 settlement has completely different needs than a 65-year-old with identical settlement amounts. Younger recipients benefit from decades of potential growth when investing lump sums wisely. Older recipients might prioritize security of guaranteed lifetime income over growth potential. If you have health conditions reducing life expectancy, lump sums generally make more financial sense than lifetime payment structures.

Financial discipline requires brutal honesty with yourself. Have you successfully managed money historically? Look at your actual track record, not your good intentions. Have you maintained emergency funds? Avoided credit card debt spirals? Invested consistently for retirement? Or do you have a history of impulsive purchases, gambling losses, or constantly bailing out family members? Have you filed bankruptcy? If your financial track record is weak, structured payments protect you from yourself. If you've demonstrated consistent financial responsibility, you can probably handle immediate payment.

Investment knowledge separates confident investors from those who'll make expensive mistakes. Do you understand asset allocation, diversification, risk tolerance, tax-efficient investing, and rebalancing strategies? If these concepts seem foreign or confusing, you'll either need to hire a financial advisor (reducing your returns through advisory fees) or accept that you lack expertise to manage a large lump sum successfully.

Debt obligations require immediate attention in certain situations. Facing foreclosure? Vehicle repossession? Aggressive creditor lawsuits? You need money now—structured payments won't stop a foreclosure proceeding already in progress. However, if your debts are manageable and you're negotiating payment plans, structured settlements might offer better long-term creditor protection.

The biggest mistake I see is people choosing their payout method based on what sounds appealing rather than what actually matches their circumstances.A client with $200,000 in medical debt and a foreclosure notice needs immediate payment regardless of long-term benefits of structured payments. But someone with no debt, secure housing, and poor money management skills should seriously consider structured payments despite the flexibility appeal of lump sums

— Jennifer Martinez

Family support needs influence the decision significantly. Supporting children through college? Caring for elderly parents? Supporting a disabled spouse? Guaranteed monthly income provides security for dependents. If you're single with no dependents, you have more freedom to take investment risks with immediate payment.

Employment status and income matter considerably. If you're returning to work earning solid income, you might not need immediate settlement money for living expenses—making structured payments or deferred payments attractive. If your injuries prevent you from ever working again, you need income replacement now, though structured payments can provide that ongoing income stream.

Tax Implications of Different Settlement Payout Methods

Tax treatment of motorcycle accident settlements depends primarily on what the settlement compensates, not on your delivery method. The IRS provides clear guidance: compensation for physical injuries and physical sickness is not taxable income, whether you receive immediate payment or structured payments.

This means if your $400,000 settlement compensates for medical expenses, pain and suffering, lost wages due to physical injury, and permanent disability, the entire amount arrives tax-free. Receive it all at once? Tax-free. Receive it as structured payments over twenty years? Each payment is tax-free.

However, several settlement components can trigger tax obligations:

Punitive damages are always taxable, even in physical injury cases. If your settlement includes $50,000 in punitive damages (uncommon in motorcycle accident cases but possible in egregious situations), that portion becomes taxable income regardless of payout structure.

Interest on delayed payments is taxable. If your settlement agreement includes interest for late payment, that interest portion gets taxed as income.

Lost wages allocated separately can create tax complications. The IRS position maintains that lost wage compensation for physical injuries is tax-free, but some settlement agreements specifically allocate portions to lost wages, potentially triggering tax obligations. Your settlement agreement language matters significantly.

Emotional distress without physical injury is taxable. If you weren't physically injured but received a settlement for emotional trauma, that's taxable income. This scenario rarely occurs in motorcycle accident cases since nearly all involve physical injury.

The payout structure affects tax treatment in one significant way: investment earnings. With immediate payment, any investment returns—interest, dividends, capital gains—face normal taxation. If you receive $300,000 tax-free and invest it, your investment earnings get taxed. With structured payments, the annuity grows tax-deferred, and you never pay taxes on that growth—it's all included in your tax-free payments.

Here's a concrete example: You receive a $500,000 lump sum tax-free and invest it, earning 7% annually. Your investment grows to $967,000 over ten years. You'll pay capital gains taxes on the $467,000 gain when you sell investments. Alternatively, you accept structured payments paying $60,000 annually for ten years ($600,000 total). All $600,000 arrives tax-free—you pay zero taxes on the growth built into the annuity.

Medicare and Medicaid considerations add complexity many people overlook. Large lump sum settlements can disqualify you from these programs because they count as available assets. Structured payments offer more protection—future payments often aren't counted as current assets in many states, helping preserve benefit eligibility. If you anticipate needing government benefits, consult an elder law attorney or benefits specialist before choosing your payout structure.

Attorney fee implications vary by arrangement. Your lawyer's contingency fee (typically 33-40%) gets deducted from the gross settlement. Whether you receive immediate payment or structured payments, the attorney fee calculation remains the same. However, some attorneys take their entire fee upfront even if you choose structured payments, while others structure their fee alongside your payments. This doesn't affect your taxes but significantly impacts your lawyer's preferences and advice.

Author: Ryan Whitlock;

Source: spy-delhi.com

Common Mistakes Motorcycle Accident Victims Make When Choosing a Payout Option

1. Choosing based on what friends or family did. Your brother-in-law's decision to take everything upfront for his car accident settlement has zero relevance to your motorcycle injury case. Settlement amounts differ. Injury severity differs. Ages differ. Financial situations differ. Personal circumstances differ dramatically. What worked perfectly for someone else could wreck your financial future.

2. Failing to calculate actual payment amounts carefully. Many people hear "$500,000 structured settlement" and assume they're receiving exactly $500,000. Then they discover the structure actually delivers $2,000 monthly for 20 years—totaling $480,000, not $500,000. Always demand exact payment schedules showing every payment amount and specific date before making your decision.

3. Ignoring annuity company financial strength ratings. Not all insurance companies are equally stable or reliable. Accepting structured payments from a B-rated company to get slightly higher payments is foolish. If that company fails financially in fifteen years, your payments stop permanently. Only accept annuities from A++ or AAA-rated companies with proven financial stability.

4. Underestimating how quickly lump sums disappear. That $250,000 seems enormous until you pay off $80,000 in medical bills, eliminate $40,000 in credit card debt, buy a $35,000 vehicle, give $20,000 to family members who need help, take a $15,000 vacation (you deserve it after what you've been through), and make a few investments that don't work out. Suddenly you're at $60,000 with no ongoing income. This exact scenario plays out constantly.

5. Accepting structured payments without inflation protection. Fixed payments steadily lose buying power as years pass. $3,000 monthly today equals roughly $1,800 monthly in twenty years (assuming 2.5% annual inflation). If you choose structured payments, negotiate increasing payment amounts—even 2-3% annual increases make enormous differences over decades.

6. Not consulting a financial advisor before deciding. Your personal injury attorney is a legal expert, not a financial planner. Before choosing your payout structure, invest $500-1,000 for a consultation with a fee-only Certified Financial Planner who can analyze your specific situation without conflicts of interest. Avoid advisors who earn commissions on products they sell you.

7. Letting immediate needs override long-term planning entirely. Yes, you need money now for bills and expenses. But accepting immediate full payment when a hybrid structure (partial lump sum plus ongoing payments) would serve you better is shortsighted. Many settlements can be structured with immediate payment for urgent needs plus monthly payments for long-term security—giving you both.

Comparing Your Options: Lump Sum vs. Structured Settlement

| Feature | Lump Sum Payment | Structured Settlement |

| Payment timing | One payment arriving 30-60 days after signing release | Scheduled payments arriving over months, years, or your lifetime |

| Investment control | Complete control to invest however you choose | Annuity company manages funds; you have zero control |

| Tax treatment | Settlement itself arrives tax-free; investment earnings are taxable | Every payment arrives tax-free including built-in growth |

| Creditor vulnerability | Exposed once deposited in your account (exemptions vary by state) | Stronger legal protection; future payments often exempt from creditors |

| Flexibility | Immediate access to every dollar | Severely limited; you cannot accelerate payments without selling them at massive discounts |

| Risk of mismanagement | High risk; entire amount can disappear through poor decisions | Low risk; payments arrive on schedule regardless of your spending habits |

| Best candidates | Financially disciplined people with investment knowledge, immediate large expenses, younger recipients who can invest long-term | People with ongoing medical needs, limited financial experience, older recipients seeking guaranteed income |

| Minimum settlement amount | No minimum; available for settlements of any size | Usually requires $50,000+ due to administrative costs |

Frequently Asked Questions About Motorcycle Accident Settlement Payouts

Choosing between immediate full payment and structured settlement payments ranks among the most consequential financial decisions you'll face after a motorcycle accident. The right choice depends on your medical needs, financial discipline, age, debt obligations, and long-term goals—not on what sounds appealing or what others recommend.

Take time analyzing your situation honestly. Consult with a financial advisor who has no stake in your decision. Run the actual numbers for both scenarios. Consider hybrid structures that provide immediate funds for urgent needs while securing long-term income. And remember: this decision is permanent, so choose based on your actual circumstances and honest self-assessment, not wishful thinking about your financial discipline or investment skills.

Your settlement represents compensation for serious injuries and losses. Whether you receive it all at once or over time, protect this money by making an informed, deliberate choice about the payout structure that truly serves your needs.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to offer insights and guidance on motorcycle accident insurance claims, settlement processes, liability issues, coverage limits, medical compensation, and related insurance matters, and should not be considered legal or financial advice.

All information, articles, and materials presented on this website are for general informational purposes only. Insurance policies, liability standards, settlement practices, and state regulations may vary by jurisdiction and insurer. The outcome of a motorcycle accident claim depends on the specific facts of the accident, available evidence, policy language, and applicable law.

This website is not responsible for any errors or omissions in the content, or for actions taken based on the information provided. Users are strongly encouraged to consult with a qualified attorney or licensed insurance professional regarding their specific motorcycle accident claim before making decisions about settlements, negotiations, or coverage disputes.